Question: Please solve the following question without using Chatgpt and with FULL calculations. Please also recheck your answers once again so that the calculations make sense.

Please solve the following question without using Chatgpt and with FULL calculations. Please also recheck your answers once again so that the calculations make sense. Otherwise I would have to downvote.

One information I think would help you would be the following link, which solves question A, but only gives you brief directions on how to solve question B:

https://www.chegg.com/homework-help/questions-and-answers/hope-give-entire-answer-don-t-copy-chegg-answers--please-quickly-q115747586

ONLY IF the solving method for question A in the above link seems correct to you, please answer question B for me here. If not, please solve both question A and B for me here. Thank you, and please don't write illogical and careless answers I have received multiple times on this site.

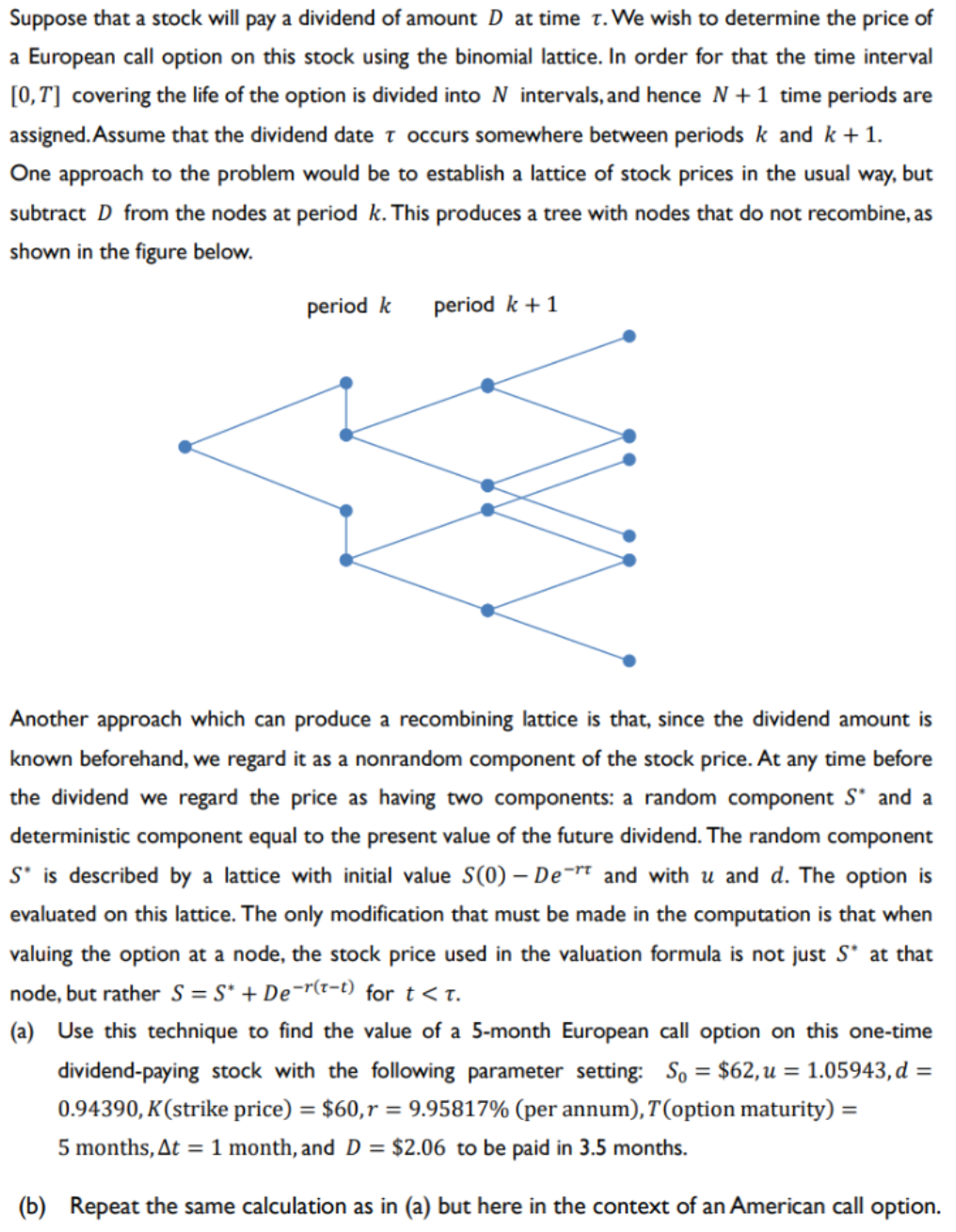

Suppose that a stock will pay a dividend of amount D at time . We wish to determine the price of a European call option on this stock using the binomial lattice. In order for that the time interval [0,T] covering the life of the option is divided into N intervals, and hence N+1 time periods are assigned.Assume that the dividend date occurs somewhere between periods k and k+1. One approach to the problem would be to establish a lattice of stock prices in the usual way, but subtract D from the nodes at period k. This produces a tree with nodes that do not recombine, as shown in the figure below. Another approach which can produce a recombining lattice is that, since the dividend amount is known beforehand, we regard it as a nonrandom component of the stock price. At any time before the dividend we regard the price as having two components: a random component S and a deterministic component equal to the present value of the future dividend. The random component S is described by a lattice with initial value S(0)Der and with u and d. The option is evaluated on this lattice. The only modification that must be made in the computation is that when valuing the option at a node, the stock price used in the valuation formula is not just S at that node, but rather S=S+Der(t) for t<. use this technique to find the value of a european call option on one-time dividend-paying stock with following parameter setting: s0="$62,u=1.05943,d=" price annum t maturity months month and d="$2.06" be paid in months. repeat same calculation as but here context an american option. suppose that will pay dividend amount at time . we wish determine using binomial lattice. order for interval covering life is divided into n intervals hence periods are assigned.assume date occurs somewhere between k one approach problem would establish lattice prices usual way subtract from nodes period k. produces tree do not recombine shown figure below. another which can produce recombining since known beforehand regard it nonrandom component price. any before having two components: random s deterministic equal present future dividend. described by initial u d. evaluated only modification must made computation when valuing node used valuation formula just rather>

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts