Question: please solve this in excel with formulas given 1) An investor buys a three-year bond with a 6% coupon rate paid annually. The bond is

please solve this in excel with formulas given

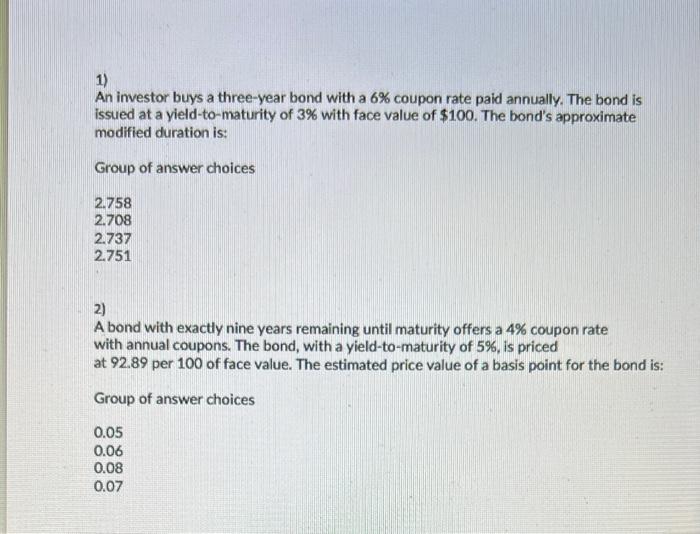

1) An investor buys a three-year bond with a 6% coupon rate paid annually. The bond is issued at a yield-to-maturity of 3% with face value of $100. The bond's approximate modified duration is: Group of answer choices 2.758 2.708 2.737 2.751 2) A bond with exactly nine years remaining until maturity offers a 4% coupon rate with annual coupons. The bond, with a yield-to-maturity of 5%, is priced at 92.89 per 100 of face value. The estimated price value of a basis point for the bond is: Group of answer choices 0.05 0.06 0.08 0.07

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock