Question: please solve this question precisely Consider a market with A securities. Let x, denote the weight of security / in a portfolio, I', the variance

please solve this question precisely

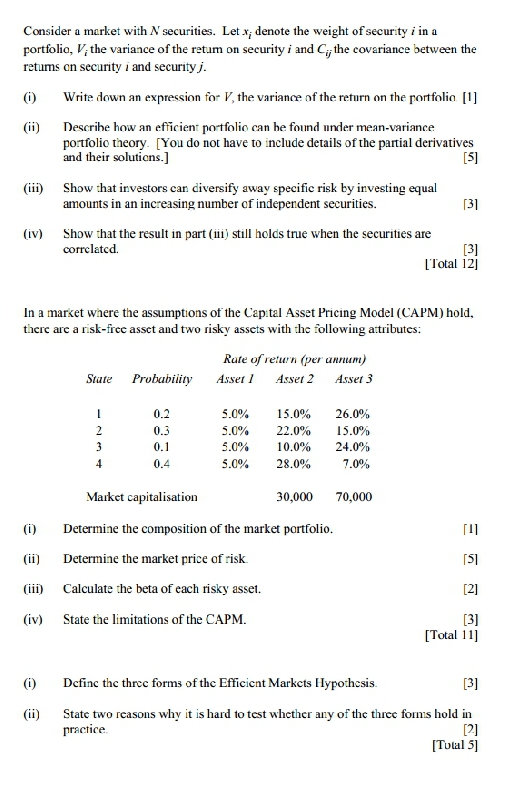

Consider a market with A securities. Let x, denote the weight of security / in a portfolio, I', the variance of the retum on security i and Cy the covariance between the returns on security i and security j. (i) Write down an expression for I', the variance of the return on the portfolio [1] (ii) Describe how an efficient portfolio can be found under mean-variance portfolio theory. [You do not have to include details of the partial derivatives and their solutions.] [5] (iii) Show that investors can diversify away specific risk by investing equal amounts in an increasing number of independent securities. 131 (iv) Show that the result in part (iii) still holds true when the securities are correlated. [3] ['Total 12] In a market where the assumptions of the Capital Asset Pricing Model (CAPM) hold, there are a risk-free asset and two risky assets with the following attributes: Rate of return (per unnum) State Probability Asser / Asset 2 Asset 3 0.2 5.0% 15.0% 26.0% 0.3 5.0% 22.0% 15.0% 0.1 5.0% 10.0% 24.0% 0.4 5.0% 28.0% 7.0% Market capitalisation 30,000 70,000 (i) Determine the composition of the market portfolio. (ii] Determine the market price of risk (iii) Calculate the beta of each risky asset. [2] (iv) State the limitations of the CAPM. [3] [Total 11] (i) Define the three forms of the Efficient Markets Hypothesis. [3] (ii) State two reasons why it is hard to test whether any of the three forms hold in practice. [2] [Total 5]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts