Question: Please tell me which function I should apply to get the answer to the following. The yellow cells are the figures I have to calculate

Please tell me which function I should apply to get the answer to the following. The yellow cells are the figures I have to calculate

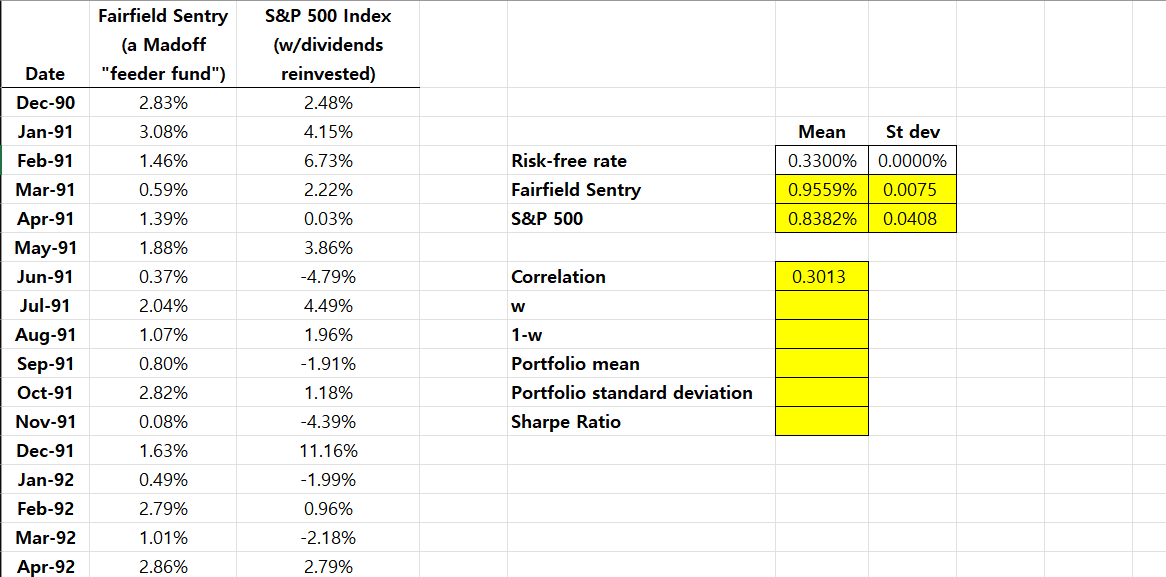

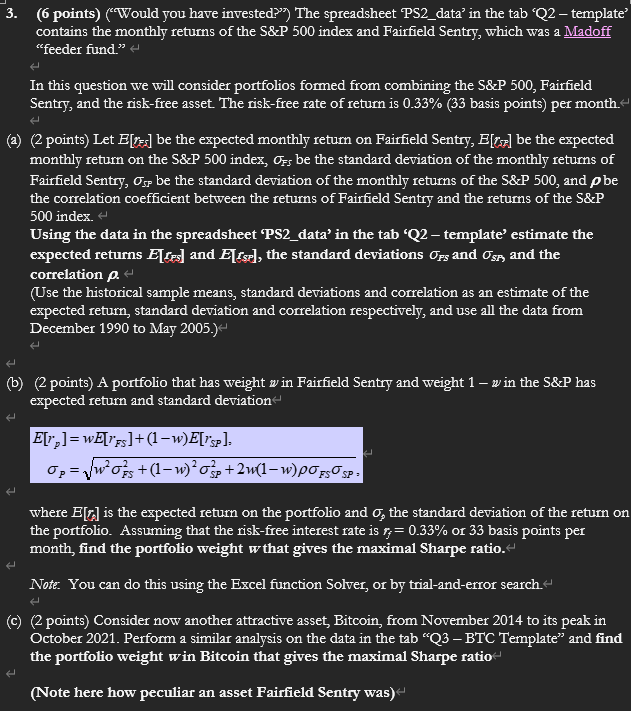

\f3. (6 points) ("Would you have invested?"?) The spreadsheet PS2_data' in the tab 'Q2- template contains the monthly returns of the S&P 500 index and Fairfield Sentry, which was a Madoff "feeder fund."~ In this question we will consider portfolios formed from combining the S&P 500, Fairfield Sentry, and the risk-free asset. The risk-free rate of return is 0.33% (33 basis points) per month. (a) (2 points) Let Elve] be the expected monthly return on Fairfield Sentry, E[ ] be the expected monthly return on the S&P 500 index, Or be the standard deviation of the monthly returns of Fairfield Sentry, Us be the standard deviation of the monthly returns of the S&P 500, and p be the correlation coefficient between the returns of Fairfield Sentry and the returns of the S&P 500 index. ~ Using the data in the spreadsheet 'PS2_data' in the tab 'Q2 - template' estimate the expected returns E[res] and Else], the standard deviations Ops and Use, and the correlation p. Use the historical sample means, standard deviations and correlation as an estimate of the expected return, standard deviation and correlation respectively, and use all the data from December 1990 to May 2005.)~ (b) (2 points) A portfolio that has weight : in Fairfield Sentry and weight 1 - w in the S&P has expected return and standard deviation E[ ]= WE[FS]+ (1-w) E[/SP ]. Op = 1Worst(1-w)'sp + 2w(1-w)popsSP = where B is the expected return on the portfolio and O, the standard deviation of the return on the portfolio. Assuming that the risk-free interest rate is = 0.33% or 33 basis points per month, find the portfolio weight w that gives the maximal Sharpe ratio. Note: You can do this using the Excel function Solver, or by trial-and-error search. (c) (2 points) Consider now another attractive asset, Bitcoin, from November 2014 to its peak in October 2021. Perform a similar analysis on the data in the tab "Q3 - BTC Template" and find the portfolio weight win Bitcoin that gives the maximal Sharpe ratio (Note here how peculiar an asset Fairfield Sentry was)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!