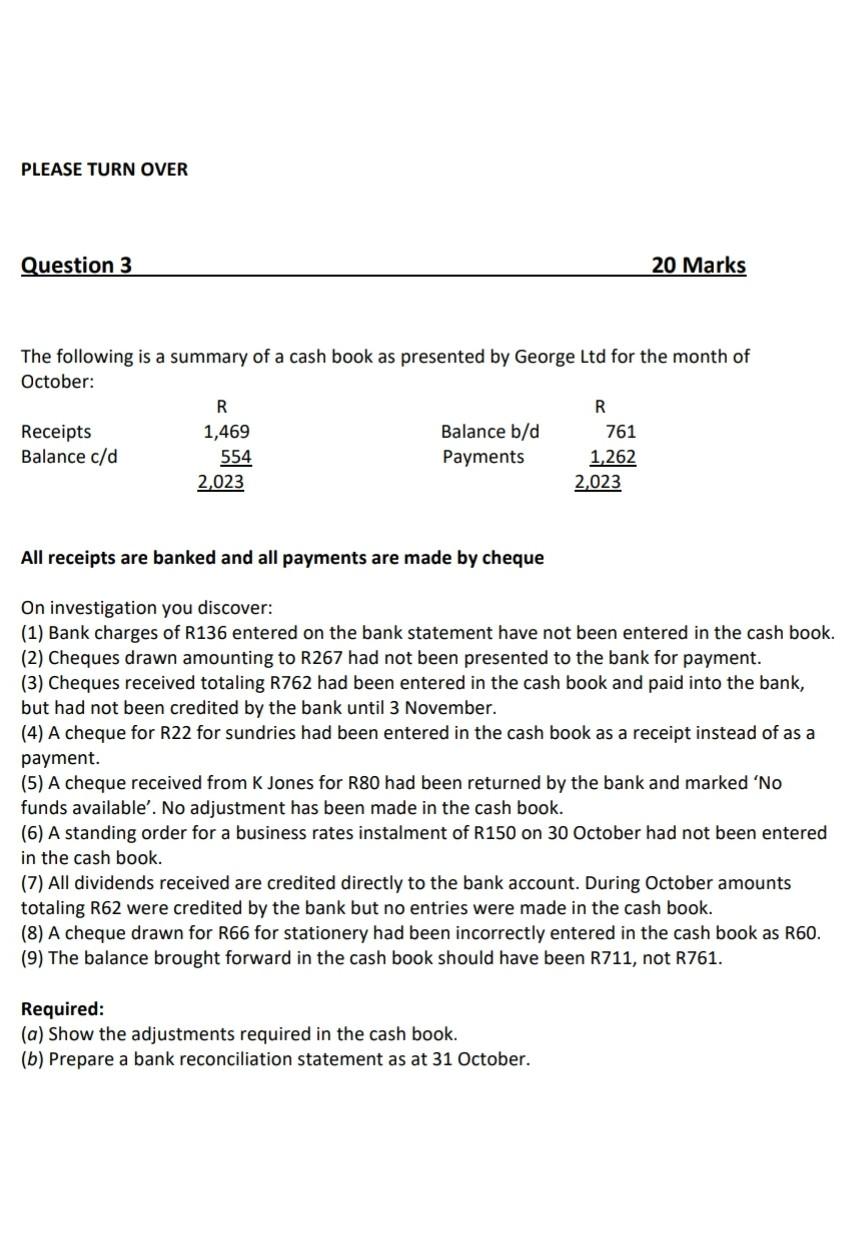

Question: PLEASE TURN OVER Question 3 20 Marks The following is a summary of a cash book as presented by George Ltd for the month of

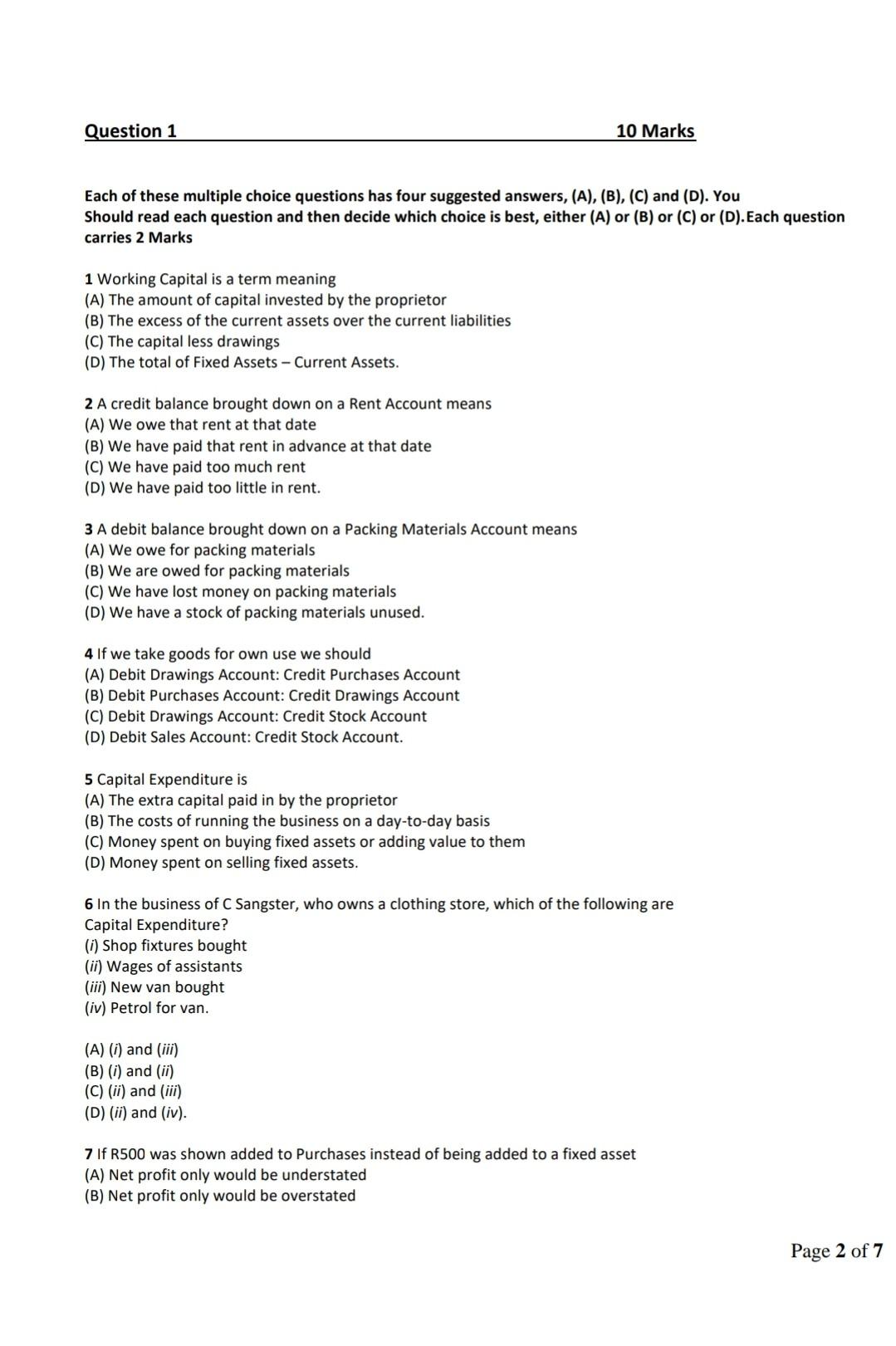

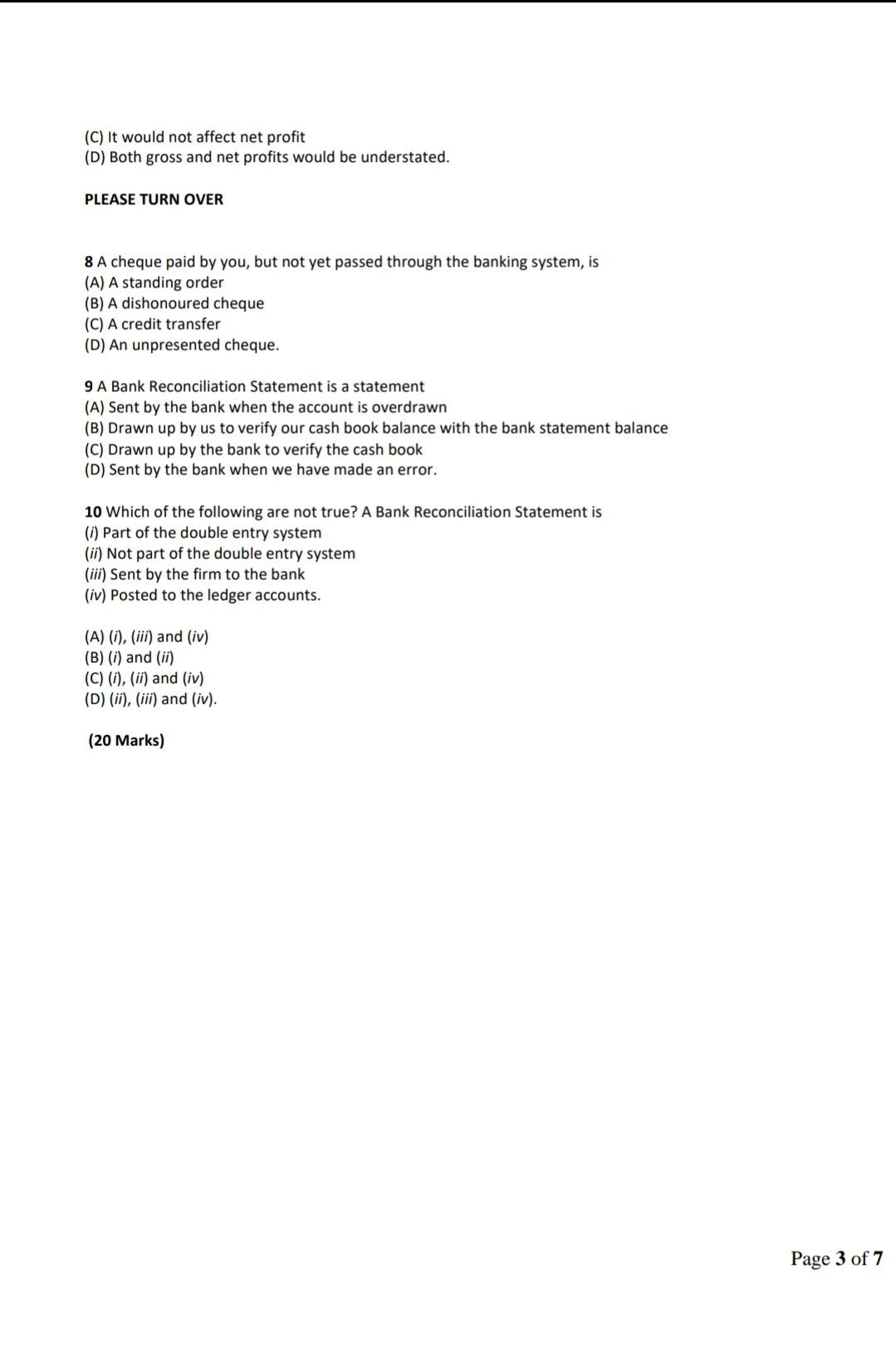

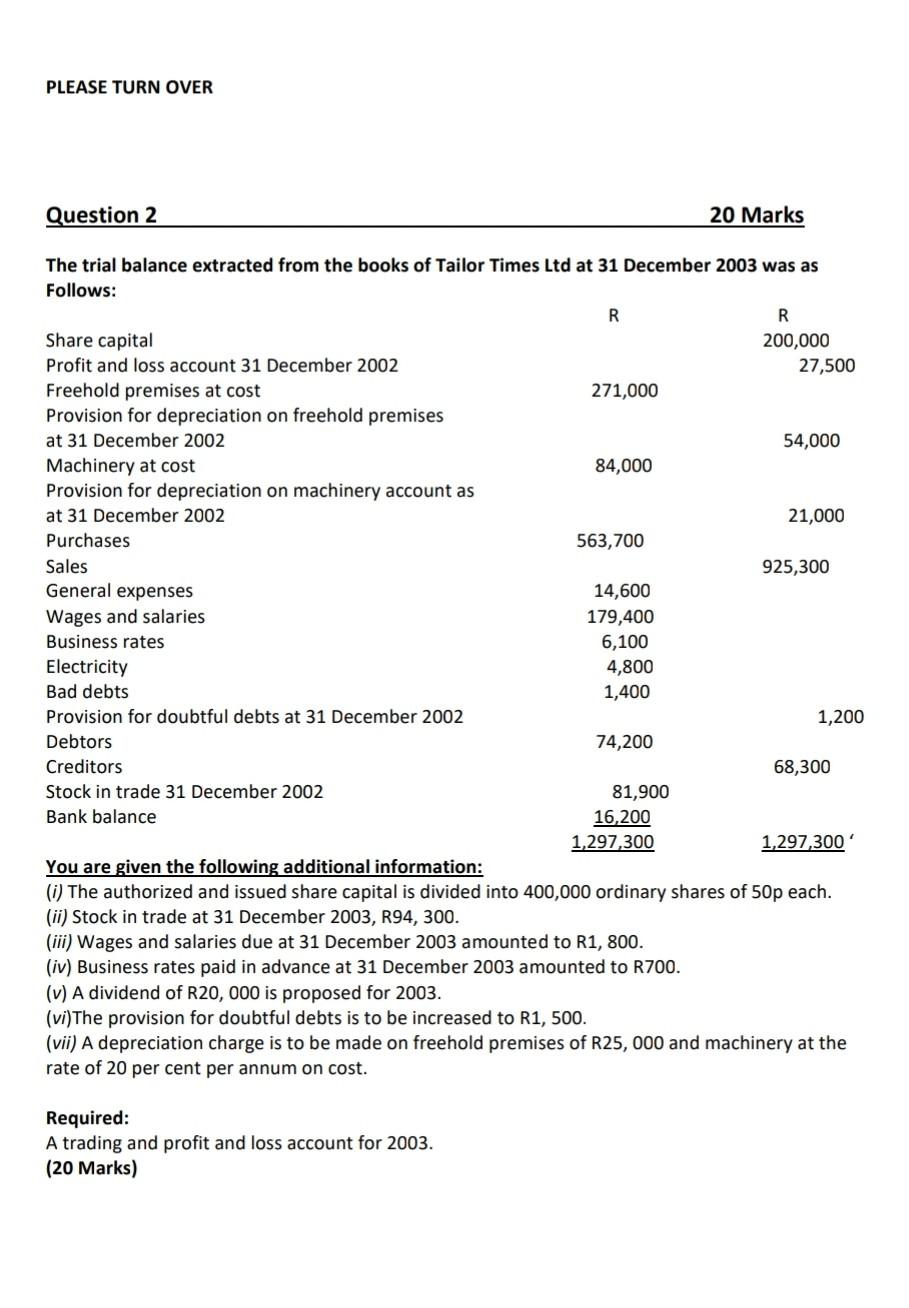

PLEASE TURN OVER Question 3 20 Marks The following is a summary of a cash book as presented by George Ltd for the month of October: R R Receipts 1,469 Balance b/d 761 Balance c/d 554 Payments 1,262 2,023 2,023 All receipts are banked and all payments are made by cheque On investigation you discover: (1) Bank charges of R136 entered on the bank statement have not been entered in the cash book. (2) Cheques drawn amounting to R267 had not been presented to the bank for payment. (3) Cheques received totaling R762 had been entered in the cash book and paid into the bank, but had not been credited by the bank until 3 November. (4) A cheque for R22 for sundries had been entered in the cash book as a receipt instead of as a payment. (5) A cheque received from K Jones for R80 had been returned by the bank and marked 'No funds available'. No adjustment has been made in the cash book. (6) A standing order for a business rates instalment of R150 on 30 October had not been entered in the cash book. (7) All dividends received are credited directly to the bank account. During October amounts totaling R62 were credited by the bank but no entries were made in the cash book. (8) A cheque drawn for R66 for stationery had been incorrectly entered in the cash book as R60. (9) The balance brought forward in the cash book should have been R711, not R761. Required: (a) Show the adjustments required in the cash book. (b) Prepare a bank reconciliation statement as at 31 October. Question 1 10 Marks Each of these multiple choice questions has four suggested answers, (A), (B), (C) and (D). You Should read each question and then decide which choice is best, either (A) or (B) or (C) or (D). Each question carries 2 Marks 1 Working Capital is a term meaning (A) The amount of capital invested by the proprietor (B) The excess of the current assets over the current liabilities (C) The capital less drawings (D) The total of Fixed Assets - Current Assets. 2 A credit balance brought down on a Rent Account means (A) We owe that rent at that date (B) We have paid that rent in advance at that date (C) We have paid too much rent (D) We have paid too little in rent. 3 A debit balance brought down on a Packing Materials Account means (A) We owe for packing materials (B) We are owed for packing materials (C) We have lost money on packing materials (D) We have a stock of packing materials unused. 4 If we take goods for own use we should (A) Debit Drawings Account: Credit Purchases Account (B) Debit Purchases Account: Credit Drawings Account (C) Debit Drawings Account: Credit Stock Account (D) Debit Sales Account: Credit Stock Account. 5 Capital Expenditure is (A) The extra capital paid in by the proprietor (B) The costs of running the business on a day-to-day basis (C) Money spent on buying fixed assets or adding value to them (D) Money spent on selling fixed assets. 6 In the business of C Sangster, who owns a clothing store, which of the following are Capital Expenditure? (i) Shop fixtures bought (ii) Wages of assistants (iii) New van bought (iv) Petrol for van. (A) (i) and (iii) (B) (i) and (ii) (C) (ii) and (iii) (D) (ii) and (iv). 7 If R500 was shown added to purchases instead of being added to a fixed asset (A) Net profit only would be understated (B) Net profit only would be overstated Page 2 of 7 (C) It would not affect net profit (D) Both gross and net profits would be understated. PLEASE TURN OVER 8 A cheque paid by you, but not yet passed through the banking system, is (A) A standing order (B) A dishonoured cheque (C) A credit transfer (D) An unpresented cheque. 9 A Bank Reconciliation Statement is a statement (A) Sent by the bank when the account is overdrawn (B) Drawn up by us to verify our cash book balance with the bank statement balance (C) Drawn up by the bank to verify the cash book (D) Sent by the bank when we have made an error. 10 Which of the following are not true? A Bank Reconciliation Statement is (i) Part of the double entry system (ii) Not part of the double entry system (iii) Sent by the firm to the bank (iv) Posted to the ledger accounts. (A) (i), (iii) and (iv) (B) (i) and (ii) (C) (i), (ii) and (iv) (D) (ii), (iii) and (iv). (20 Marks) Page 3 of 7 PLEASE TURN OVER Question 2 20 Marks The trial balance extracted from the books of Tailor Times Ltd at 31 December 2003 was as Follows: R R Share capital 200,000 Profit and loss account 31 December 2002 27,500 Freehold premises at cost 271,000 Provision for depreciation on freehold premises at 31 December 2002 54,000 Machinery at cost 84,000 Provision for depreciation on machinery account as at 31 December 2002 21,000 Purchases 563,700 Sales 925,300 General expenses 14,600 Wages and salaries 179,400 Business rates 6,100 Electricity 4,800 Bad debts 1,400 Provision for doubtful debts at 31 December 2002 1,200 Debtors 74,200 Creditors 68,300 Stock in trade 31 December 2002 81,900 Bank balance 16,200 1,297,300 1,297,300 You are given the following additional information: (i) The authorized and issued share capital is divided into 400,000 ordinary shares of 50p each. (ii) Stock in trade at 31 December 2003, R94, 300. (iii) Wages and salaries due at 31 December 2003 amounted to R1, 800. (iv) Business rates paid in advance at 31 December 2003 amounted to R700. (v) A dividend of R20,000 is proposed for 2003. (vi) The provision for doubtful debts is to be increased to R1, 500. (vii) A depreciation charge is to be made on freehold premises of R25,000 and machinery at the rate of 20 per cent per annum on cost. Required: A trading and profit and loss account for 2003. (20 Marks) PLEASE TURN OVER Question 4 20 Marks The financial year of The Better Trading Company ended on 30 November 2007. You have been asked to prepare a Total Debtors Account and a Total Creditors Account in order to produce End-of-year figures for Debtors and Creditors for the draft final accounts. You are able to obtain the following information for the financial year from the books of original entry: Sales - cash - credit Purchases - cash - credit Total receipts from customers Total payments to suppliers Discounts allowed (all to credit customers) Discounts received (all from credit suppliers) Refunds given to cash customers Balance in the sales ledger set off against balance in the purchases ledger Bad debts written off Increase in the provision for bad debts Credit notes issued to credit customers Credit notes received from credit suppliers R 344,890 268,187 14,440 496,600 600,570 503,970 5,520 3,510 5,070 70 780 90 4,140 1,480 According to the audited financial statements for the previous year debtors and creditors as at 1 December 2006 were R26,555 and R43, 450 respectively. Required: Draw up the relevant Total Accounts entering end-of-year totals for debtors and creditors. (20 Marks) Pag PLEASE TURN OVER Question 5 Total Marks 20 J Massa is setting up a new business. Before actually selling anything, he bought a van for R4, 500, a market stall for R2,000 and a stock of goods for R1, 500. He did not pay in full for his stock of goods and still owes R1,000 in respect of them. He borrowed R5,000 from C Fox. After the events just described, and before trading starts, he has R400 cash in hand and R1, 100 cash at bank. Calculate the amount of his capital. (10 Marks) Draw up Emmanuel's balance sheet from the following information as at 31 December 2008: R Capital 7,200 Debtors 1,200 Van 3,800 Creditors 1,600 Fixtures 1,800 Stock of goods 4,200 Cash at bank 300 (10 Marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts