Question: please urgent. tqvm PART B - PROBLEM QUESTIONS Answering time: 3.00 PM - 3.55 PM (55 minutes); Submission to be received by: 4.05 PM] QUESTION

![- 3.55 PM (55 minutes); Submission to be received by: 4.05 PM]](https://s3.amazonaws.com/si.experts.images/answers/2024/09/66df556b28dab_42666df556ab8c2b.jpg)

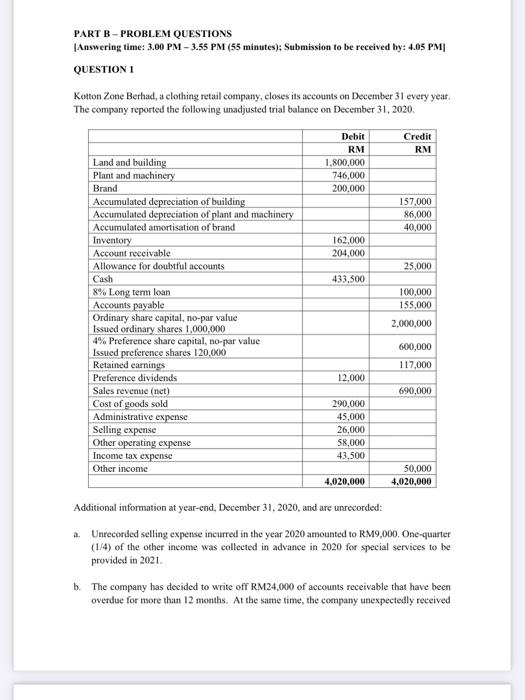

PART B - PROBLEM QUESTIONS Answering time: 3.00 PM - 3.55 PM (55 minutes); Submission to be received by: 4.05 PM] QUESTION 1 Kotton Zone Berhad, a clothing retail company, closes its accounts on December 31 every year. The company reported the following unadjusted trial balance on December 31, 2020. Debit Credit RM Land and building Plant and machinery RM 1.800,000 746,000 200.000 Brand 157,000 86,000 40,000 162,000 204,000 25,000 433,500 100,000 155,000 2,000,000 Accumulated depreciation of building Accumulated depreciation of plant and machinery Accumulated amortisation of brand Inventory Account receivable Allowance for doubtful accounts Cash 8% Long term loan Accounts payable Ordinary share capital, no-par value Issued ordinary shares 1,000,000 4% Preference share capital, no par value Issued preference shares 120,000 Retained earnings Preference dividends Sales revenue (net) Cost of goods sold Administrative expense Selling expense Other operating expense Income tax expense 600,000 117,000 12.000 690,000 290,000 45,000 26,000 58,000 43,500 Other income 50,000 4,020,000 4,020,000 Additional information at year-end, December 31, 2020, and are unrecorded: Unrecorded selling expense incurred in the year 2020 amounted to RM9,000. One-quarter (1/4) of the other income was collected in advance in 2020 for special services to be provided in 2021. b. The company has decided to write off RM24,000 of accounts receivable that have been overdue for more than 12 months. At the same time, the company unexpectedly received 2 of 3 a cheque of RM5,000 from a customer whose account had been written off in 2018. This transaction has not been recorded. c. Uncollectible accounts are estimated at 5% of accounts receivable. Bad debt expense is recorded as Selling expense. d Land, which has a cost of RM1,000,000, is not depreciated. The company's depreciation policy for other non-current assets is as follows: Building Straight-line method, 5% per annum Plant and machinery Diminishing-balance method, 10% per annum Depreciation is provided on a yearly basis on assets held at year-end, December 31, 2020. Depreciation expense of building, plant and machinery is recorded as administrative expense c. The brand provides a 20-year economic benefit to the company. Amortisation expense of brand is recorded as Selling expense. f. The 8% long-term loan was taken on October 1, 2020. Interest on the note is accrued at year-end, December 31, 2020. & The board of directors declared ordinary dividend of RM0.04 per share. The ordinary dividend will be distributed on January 5, 2021, together with the remaining preference dividend Required: 1. Journalize the above transactions, (a) to (g) (4 marks) 2. Prepare the following for Kotton Zone Berhad: Statement of profit or loss for the year ended December 31, 2020. (10 marks) Statement of changes in cquity for the year ended December 31, 2020 (3 marks) Statement of financial position as at, December 31, 2020. (9 marks) 3. The chief executive of Kotton Zone Berhad was informed that the financial statements in part (1) above would be available as soon as the adjusting entries are made." Does the need for adjusting entries at the end of the year imply that transactions are not being recorded properly? Use adjustment (a) above as an example. (4 marks) TOTAL: 30 MARKS PART B - PROBLEM QUESTIONS Answering time: 3.00 PM - 3.55 PM (55 minutes); Submission to be received by: 4.05 PM] QUESTION 1 Kotton Zone Berhad, a clothing retail company, closes its accounts on December 31 every year. The company reported the following unadjusted trial balance on December 31, 2020. Debit Credit RM Land and building Plant and machinery RM 1.800,000 746,000 200.000 Brand 157,000 86,000 40,000 162,000 204,000 25,000 433,500 100,000 155,000 2,000,000 Accumulated depreciation of building Accumulated depreciation of plant and machinery Accumulated amortisation of brand Inventory Account receivable Allowance for doubtful accounts Cash 8% Long term loan Accounts payable Ordinary share capital, no-par value Issued ordinary shares 1,000,000 4% Preference share capital, no par value Issued preference shares 120,000 Retained earnings Preference dividends Sales revenue (net) Cost of goods sold Administrative expense Selling expense Other operating expense Income tax expense 600,000 117,000 12.000 690,000 290,000 45,000 26,000 58,000 43,500 Other income 50,000 4,020,000 4,020,000 Additional information at year-end, December 31, 2020, and are unrecorded: Unrecorded selling expense incurred in the year 2020 amounted to RM9,000. One-quarter (1/4) of the other income was collected in advance in 2020 for special services to be provided in 2021. b. The company has decided to write off RM24,000 of accounts receivable that have been overdue for more than 12 months. At the same time, the company unexpectedly received 2 of 3 a cheque of RM5,000 from a customer whose account had been written off in 2018. This transaction has not been recorded. c. Uncollectible accounts are estimated at 5% of accounts receivable. Bad debt expense is recorded as Selling expense. d Land, which has a cost of RM1,000,000, is not depreciated. The company's depreciation policy for other non-current assets is as follows: Building Straight-line method, 5% per annum Plant and machinery Diminishing-balance method, 10% per annum Depreciation is provided on a yearly basis on assets held at year-end, December 31, 2020. Depreciation expense of building, plant and machinery is recorded as administrative expense c. The brand provides a 20-year economic benefit to the company. Amortisation expense of brand is recorded as Selling expense. f. The 8% long-term loan was taken on October 1, 2020. Interest on the note is accrued at year-end, December 31, 2020. & The board of directors declared ordinary dividend of RM0.04 per share. The ordinary dividend will be distributed on January 5, 2021, together with the remaining preference dividend Required: 1. Journalize the above transactions, (a) to (g) (4 marks) 2. Prepare the following for Kotton Zone Berhad: Statement of profit or loss for the year ended December 31, 2020. (10 marks) Statement of changes in cquity for the year ended December 31, 2020 (3 marks) Statement of financial position as at, December 31, 2020. (9 marks) 3. The chief executive of Kotton Zone Berhad was informed that the financial statements in part (1) above would be available as soon as the adjusting entries are made." Does the need for adjusting entries at the end of the year imply that transactions are not being recorded properly? Use adjustment (a) above as an example. (4 marks) TOTAL: 30 MARKS

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts