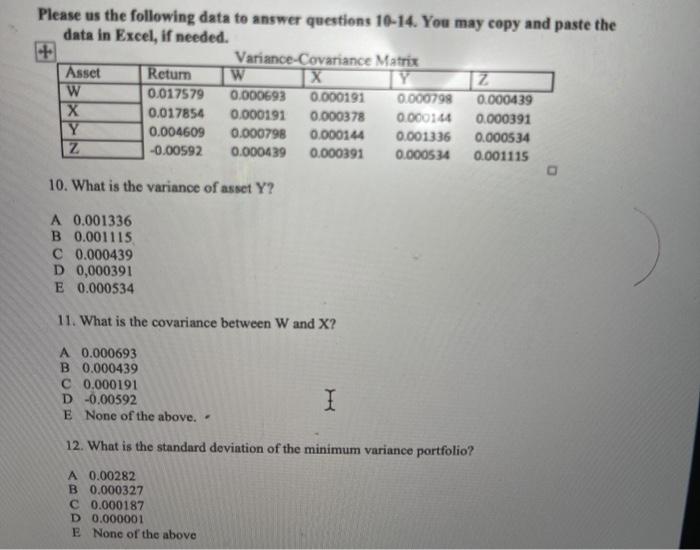

Question: Please us the following data to answer questions 10-14. You may copy and paste the data in Excel, if needed. Variance-Covariance Matrix Asset Return W

Please us the following data to answer questions 10-14. You may copy and paste the data in Excel, if needed. Variance-Covariance Matrix Asset Return W Z W 0.017579 0.000693 0.000191 0.000799 0.000439 X 0.017854 0.000191 0.000378 0.000144 0.000391 Y 0.004609 0.000798 0.000144 0.001336 0.000534 Z -0.00592 0.000439 0.000391 0.000534 0.001115 10. What is the variance of asset Y? A 0.001336 B 0.001115 C 0.000439 D 0,000391 E 0.000534 11. What is the covariance between Wand X? A 0.000693 B 0.000439 C 0.000191 D -0.00592 E None of the above.. I 12. What is the standard deviation of the minimum variance portfolio? A 0.00282 B 0.000327 0.000187 D 0.000001 E None of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts