Question: please use data above and help to solve questions for the last backgraund case requirement questions China and Japan in Iron Ore Negotiation 1. Introduction

please use data above and help to solve questions for the last backgraund case requirement questions

please use data above and help to solve questions for the last backgraund case requirement questions

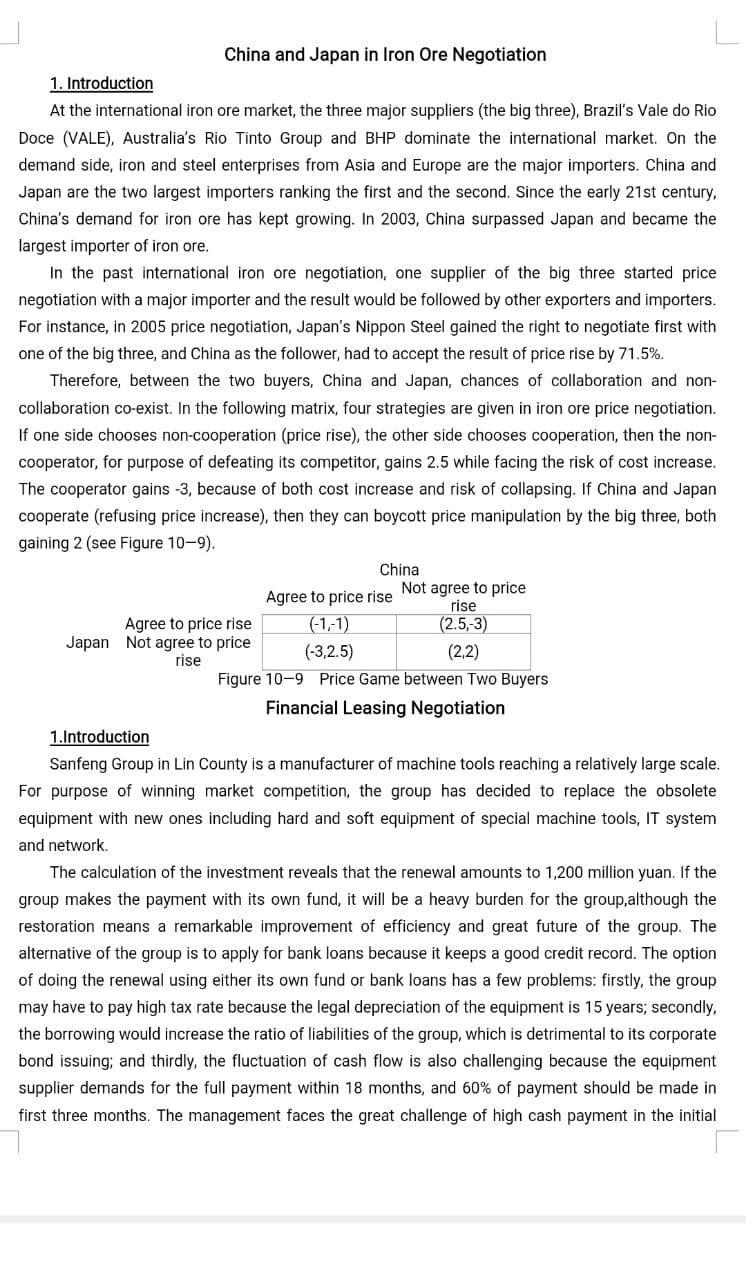

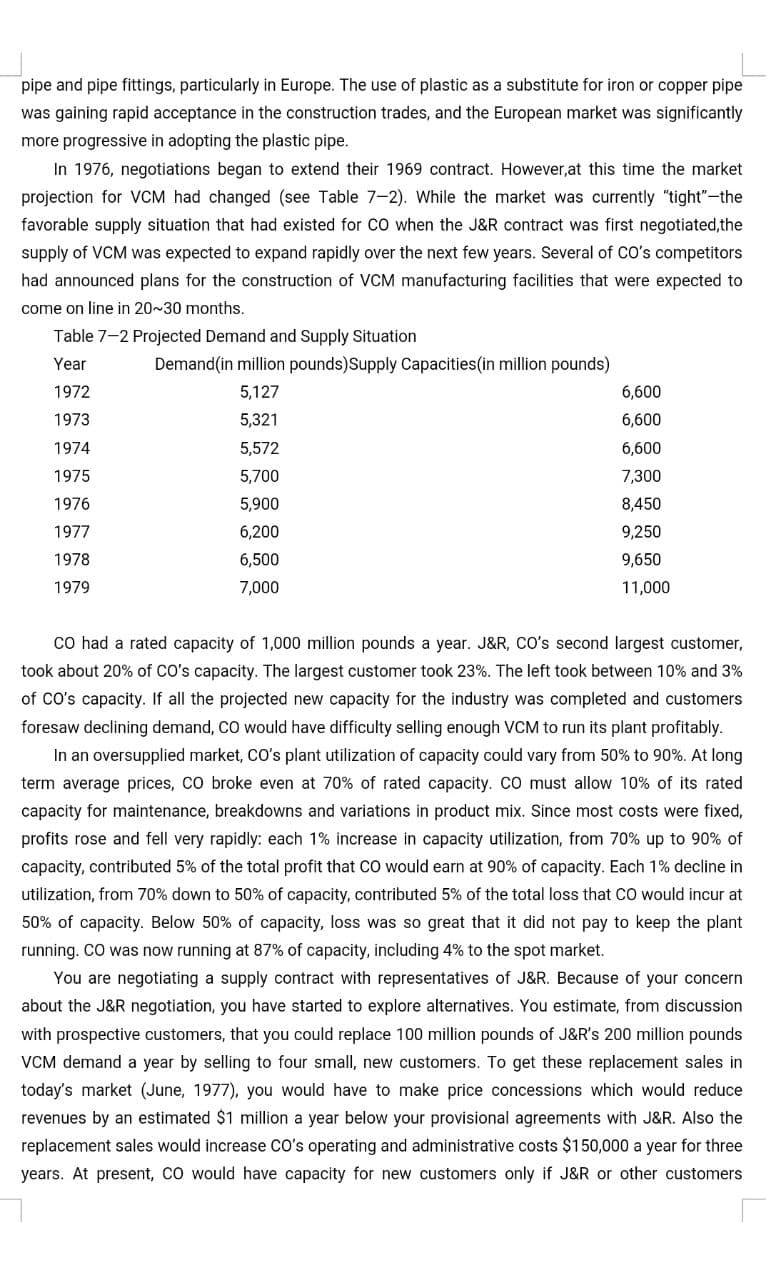

China and Japan in Iron Ore Negotiation 1. Introduction At the international iron ore market, the three major suppliers (the big three), Brazil's Vale do Rio Doce (VALE), Australia's Rio Tinto Group and BHP dominate the international market. On the demand side, iron and steel enterprises from Asia and Europe are the major importers. China and Japan are the two largest importers ranking the first and the second. Since the early 21st century. China's demand for iron ore has kept growing. In 2003, China surpassed Japan and became the largest importer of iron ore. In the past international iron ore negotiation, one supplier of the big three started price negotiation with a major importer and the result would be followed by other exporters and importers. For instance, in 2005 price negotiation, Japan's Nippon Steel gained the right to negotiate first with one of the big three, and China as the follower, had to accept the result of price rise by 71.5%. Therefore, between the two buyers, China and Japan, chances of collaboration and non- collaboration co-exist. In the following matrix, four strategies are given in iron ore price negotiation. If one side chooses non-cooperation (price rise), the other side chooses cooperation, then the non- cooperator, for purpose of defeating its competitor, gains 2.5 while facing the risk of cost increas The cooperator gains-3, because of both cost increase and risk of collapsing. If China and Japan cooperate (refusing price increase), then they can boycott price manipulation by the big three, both gaining 2 (see Figure 10-9). China Not agree to price Agree to price rise rise Agree to price rise (2.5-3) Japan Not agree to price rise (-3,2.5) (22) Figure 10-9 Price Game between Two Buyers Financial Leasing Negotiation 1.Introduction Sanfeng Group in Lin County is a manufacturer of machine tools reaching a relatively large scale. For purpose of winning market competition, the group has decided to replace the obsolete equipment with new ones including hard and soft equipment of special machine tools, IT system and network The calculation of the investment reveals that the renewal amounts to 1,200 million yuan. If the group makes the payment with its own fund, it will be a heavy burden for the group, although the restoration means a remarkable improvement of efficiency and great future of the group. The alternative of the group is to apply for bank loans because it keeps a good credit record. The option of doing the renewal using either its own fund or bank loans has a few problems: firstly, the group may have to pay high tax rate because the legal depreciation of the equipment is 15 years; secondly, the borrowing would increase the ratio of liabilities of the group, which is detrimental to its corporate bond issuing, and thirdly, the fluctuation of cash flow is also challenging because the equipment supplier demands for the full payment within 18 months, and 60% of payment should be made in first three months. The management faces the great challenge of high cash payment in the initial period and managing financial stability. The management of the group following a specialist's suggestion gets in touch with the Sunshine Financial Leasing Company (SFLC) and is informed that its investment problem can be addressed through financial leasing. Financial leasing is an alternative way of raising fund, in which a lesser, according to the requirement of a lessee, signs a purchasing contract with a supplier, as well as a leasing contract with the lessee. The lesser promises the lessee the right of using the equipment under the condition that the latter pays the rent. The lessee, upon making full payment of the rent on expiring date, gains the ownership of the equipment. Obviously, the payment structure of rent in international leasing business is important for the lesser and the lessee. There are different ways to calculate rent, and the most common one is called "equal sharing" approach. Generally speaking, the rent consists of original price of equipment, leasing interest rate, profit, service fee, estimated nominal price of the equipment, etc. The equation is shown as the following: each payments (originalprice+freight+insurance-remainingvalue)+interest+profit+servicefee totaltimesofpayment The length of leasing period depends on the life of equipment, for instance, equipment of low value is within 3 years; plants, machinery equipment, computers and the like are about 5 years; aircraft, ship and railway stocks are about 10 years. Normally, the length of leasing period is counted as 75% of equipment life. Negotiation on Oil Contract 1.Background Information The Central Oil Company (CO) was founded in 1942 as the Fortune Oil Company. It was also one of the largest and best known worldwide producers of industrial petrochemicals. Through growth and acquisition, the company expanded rapidly. It developed extensive oil holdings in North Africa and the Middle East, as well as significant coal beds in the western United States. Much of the company's oil production was sold under its own name as gasoline through service stations in US and Europe, but also it was distributed through several chains of independent gasoline stations. One of the company's major industrial chemical lines was the production of vinyl chloride monomer (VCM). The basic components of VCM are ethylene and chlorine. Ethylene is a colorless, flammable, gaseous hydrocarbon with a disagreeable odor, it is generally obtained from natural or coal gas, or by "cracking" petroleum into smaller molecular components. As a further step in the petroleum "cracking" process, ethylene is combined with chlorine to produce VCM, also a colorless gas. VCM was the primary component of a family of plastics known as the vinyl chlorides. Polyvinyl chloride can be converted to an enormous array of consumer and industrial applications: flooring, wire insulation, electrical transformers, home furnishings, piping, toys, bottles and containing, rainwear, light roofing and a variety of protective coatings. In 1969, CO established the first major contract with the J&R Corporation for the purchase of VCM. J&R was a major industrial manufacturer of wood and petrochemical products for the construction industry. J&R was expanding its manufacturing operations in the production of plastic pipe and pipe fittings, particularly in Europe. The use of plastic as a substitute for iron or copper pipe was gaining rapid acceptance in the construction trades, and the European market was significantly more progressive in adopting the plastic pipe. In 1976, negotiations began to extend their 1969 contract. However, at this time the market projection for VCM had changed (see Table 7-2). While the market was currently "tight"-the favorable supply situation that had existed for CO when the J&R contract was first negotiated, the supply of VCM was expected to expand rapidly over the next few years. Several of Co's competitors had announced plans for the construction of VCM manufacturing facilities that were expected to come on line in 20-30 months. Table 7-2 Projected Demand and Supply Situation Year Demand(in million pounds)Supply Capacities(in million pounds) 1972 5,127 6,600 1973 5,321 6,600 1974 5,572 6,600 1975 5,700 7,300 1976 5,900 8,450 1977 6,200 9,250 1978 6,500 9,650 1979 11,000 7,000 CO had a rated capacity of 1,000 million pounds a year. J&R, CO's second largest customer, took about 20% of CO's capacity. The largest customer took 23%. The left took between 10% and 3% of CO's capacity. If all the projected new capacity for the industry was completed and customers foresaw declining demand, CO would have difficulty selling enough VCM to run its plant profitably. In an oversupplied market, CO's plant utilization of capacity could vary from 50% to 90%. At long term average prices, CO broke even at 70% of rated capacity. Co must allow 10% of its rated capacity for maintenance, breakdowns and variations in product mix. Since most costs were fixed, profits rose and fell very rapidly: each 1% increase in capacity utilization, from 70% up to 90% of capacity, contributed 5% of the total profit that CO would earn at 90% of capacity. Each 1% decline in utilization, from 70% down to 50% of capacity, contributed 5% of the total loss that CO would incur at 50% of capacity. Below 50% of capacity, loss was so great that it did not pay to keep the plant running. CO was now running at 87% of capacity, including 4% to the spot market. You are negotiating a supply contract with representatives of J&R. Because of your concern about the J&R negotiation, you have started to explore alternatives. You estimate, from discussion with prospective customers, that you could replace 100 million pounds of J&R's 200 million pounds VCM demand a year by selling to four small, new customers. To get these replacement sales in today's market (June, 1977), you would have to make price concessions which would reduce revenues by an estimated $1 million a year below your provisional agreements with J&R. Also the replacement sales would increase Co's operating and administrative costs $150,000 a year for three years. At present, CO would have capacity for new customers only if J&R or other customers decreased their takes. Historically, during periods of industry over-capacity large buyers were tempted to split their purchases among suppliers and then played them off against each other to get lower prices. To control wide swings in plant utilization, producers generally would not sell quantities of 50 million pounds a year or more to one buyer without a long-term contract. CO could sell VCM in the spot market where prices and amounts available varied considerably from week to week. You prefer to sell on a contract basis to assure that your plant capacity is fully used. The spot market can be highly volatile. Spot prices can swing plus or minus 50% around the long-term trend. Although the trend of spot prices appears to be under downward pressure, 50% of the new VCM capacity projected for 1974-1977 nevertheless has come in place. Producers can postpone new plant constructions or shut down under-utilized capacity if they believe supply will be too far above long-term demand. Most producers, however, resist postponing new construction for fear of losing market share when demand increases. They resist shutdown when demand declines unless they foresee heavy, long-term losses, or imminent bankruptcy. The cost of your pipeline to J&R will be fully recovered by the end of the current contract. Sales to buyers without a pipeline are delivered by truck or railroad tank cars. Customers without a pipeline must allow an order lead time of one week to six months, depending upon Co's order backlog and the availability of trucks or tank cars. For annual volume of 50 million pounds the costs of a pipeline amortized over 8 years equal the costs of non-pipeline transportation. At higher volumes pipeline costs are recovered more rapidly. Pipeline maintenance and operation costs are less than 5% of non -pipeline transportation, CO's average contract price for large volume buyers like J&C was 15 cents/lb. in 1976, up from 10 cents/lb. in 1974. Actual contract prices are computed by a complex formula: Product price=B1(Feedstock)+B2 (Labour)+B3(Energy costs)+B4(Crude oil commodity costs). Each B is a negotiated coefficient. Prices have been rising primarily because of increases in crude oil commodity costs and feedstock prices. Predictions are that these costs will continue to rise because of OPEC. In the past 12 months spot prices of VCM have been as high as 24 cents/lb. and as low as 12 cents/lb. J&R buys a large quantity of VCM and CO is geared to supplying product to J&R's quality specifications. Interruptions in supply due to unacceptable quality or delayed shipments can force a customer like J&R to cut back production or shut down in two weeks. Although there are specific American Chemical Society product standards, the quality delivered can vary substantially across suppliers. When there are quality disputes, the parties may negotiate a settlement, agree to arbitration or, as a last resort, sue. Co has an excellent reputation as a reliable, high quality supplier. 2.Negotiation for the remaining issues Assume that you are in CO negotiating team, which consists of the V. P. Marketing-Europe, the VCM Marketing Manager-Europe, and the Assistant VCM Marketing Manager-Europe. You will be meeting with the J&R Corporation negotiating team, which consists of the J&R V. P. Europe, the Purchasing Manager, and the Assistant Purchasing Manager. Time has passed since your last meeting and it is now June 24, 1977. If neither party gives notice of termination(that is, by June 30, 1977)in 180 days, the "evergreen" clause takes effect. Evergreen means that after December 31, 1977, the contract will be renewed annually with its present terms unless either party gives notice of termination. Co had agreed to make changes on the original contract. Both sides had reached the provisional agreement on price, minimum quantities, and length of new contract (three years from date of signing) and metering. Three issues are still in dispute: (1) Most favored nation's clause(MFN):(2) Meet the competition(MTC):(3) Right to resell the product(RTR). Price: The formula price would be adjusted downward by approximately 0.85 cents per pound. Minimum quantities: J&R suggested minimum quantities of 205 million pounds in the first year of the contract and 210 million pounds in the second year and 220 million pounds in the third. CO considered the minimum quantities were ridiculously low, however, they agreed to the purchase schedule. Length of new contract: The two sides agreed to a three-year contract renewal instead of suggested five years by CO. Metering: J&R stated that the pipeline sending the product was leaking. If the new metering system could be installed they would feel infinitely more comfortable. Finally CO agreed to remeter the pipeline. The remaining issues: (1) Most favoured nation's clause. If CO negotiated with another purchaser a more favorable price for VCM than J&R was receiving now, CO would guarantee that J&R would receive that price as well. (2)Meet the competition. Co would willingly meet any lower price on VCM offered by a competitor, in order to maintain the J&R relationship. (3)Right to resell the product. J&R wanted the contractual right to resell the product if it could not use the minimum amount. Requirement for the Negotiation Organize your virtual/pretend negotiation teams according to the roles in the case. Work out your negotiation plan, including each other's interests, negotiating power, the most wanted interests and interests you can concession, other options and best alternatives. China and Japan in Iron Ore Negotiation 1. Introduction At the international iron ore market, the three major suppliers (the big three), Brazil's Vale do Rio Doce (VALE), Australia's Rio Tinto Group and BHP dominate the international market. On the demand side, iron and steel enterprises from Asia and Europe are the major importers. China and Japan are the two largest importers ranking the first and the second. Since the early 21st century. China's demand for iron ore has kept growing. In 2003, China surpassed Japan and became the largest importer of iron ore. In the past international iron ore negotiation, one supplier of the big three started price negotiation with a major importer and the result would be followed by other exporters and importers. For instance, in 2005 price negotiation, Japan's Nippon Steel gained the right to negotiate first with one of the big three, and China as the follower, had to accept the result of price rise by 71.5%. Therefore, between the two buyers, China and Japan, chances of collaboration and non- collaboration co-exist. In the following matrix, four strategies are given in iron ore price negotiation. If one side chooses non-cooperation (price rise), the other side chooses cooperation, then the non- cooperator, for purpose of defeating its competitor, gains 2.5 while facing the risk of cost increas The cooperator gains-3, because of both cost increase and risk of collapsing. If China and Japan cooperate (refusing price increase), then they can boycott price manipulation by the big three, both gaining 2 (see Figure 10-9). China Not agree to price Agree to price rise rise Agree to price rise (2.5-3) Japan Not agree to price rise (-3,2.5) (22) Figure 10-9 Price Game between Two Buyers Financial Leasing Negotiation 1.Introduction Sanfeng Group in Lin County is a manufacturer of machine tools reaching a relatively large scale. For purpose of winning market competition, the group has decided to replace the obsolete equipment with new ones including hard and soft equipment of special machine tools, IT system and network The calculation of the investment reveals that the renewal amounts to 1,200 million yuan. If the group makes the payment with its own fund, it will be a heavy burden for the group, although the restoration means a remarkable improvement of efficiency and great future of the group. The alternative of the group is to apply for bank loans because it keeps a good credit record. The option of doing the renewal using either its own fund or bank loans has a few problems: firstly, the group may have to pay high tax rate because the legal depreciation of the equipment is 15 years; secondly, the borrowing would increase the ratio of liabilities of the group, which is detrimental to its corporate bond issuing, and thirdly, the fluctuation of cash flow is also challenging because the equipment supplier demands for the full payment within 18 months, and 60% of payment should be made in first three months. The management faces the great challenge of high cash payment in the initial period and managing financial stability. The management of the group following a specialist's suggestion gets in touch with the Sunshine Financial Leasing Company (SFLC) and is informed that its investment problem can be addressed through financial leasing. Financial leasing is an alternative way of raising fund, in which a lesser, according to the requirement of a lessee, signs a purchasing contract with a supplier, as well as a leasing contract with the lessee. The lesser promises the lessee the right of using the equipment under the condition that the latter pays the rent. The lessee, upon making full payment of the rent on expiring date, gains the ownership of the equipment. Obviously, the payment structure of rent in international leasing business is important for the lesser and the lessee. There are different ways to calculate rent, and the most common one is called "equal sharing" approach. Generally speaking, the rent consists of original price of equipment, leasing interest rate, profit, service fee, estimated nominal price of the equipment, etc. The equation is shown as the following: each payments (originalprice+freight+insurance-remainingvalue)+interest+profit+servicefee totaltimesofpayment The length of leasing period depends on the life of equipment, for instance, equipment of low value is within 3 years; plants, machinery equipment, computers and the like are about 5 years; aircraft, ship and railway stocks are about 10 years. Normally, the length of leasing period is counted as 75% of equipment life. Negotiation on Oil Contract 1.Background Information The Central Oil Company (CO) was founded in 1942 as the Fortune Oil Company. It was also one of the largest and best known worldwide producers of industrial petrochemicals. Through growth and acquisition, the company expanded rapidly. It developed extensive oil holdings in North Africa and the Middle East, as well as significant coal beds in the western United States. Much of the company's oil production was sold under its own name as gasoline through service stations in US and Europe, but also it was distributed through several chains of independent gasoline stations. One of the company's major industrial chemical lines was the production of vinyl chloride monomer (VCM). The basic components of VCM are ethylene and chlorine. Ethylene is a colorless, flammable, gaseous hydrocarbon with a disagreeable odor, it is generally obtained from natural or coal gas, or by "cracking" petroleum into smaller molecular components. As a further step in the petroleum "cracking" process, ethylene is combined with chlorine to produce VCM, also a colorless gas. VCM was the primary component of a family of plastics known as the vinyl chlorides. Polyvinyl chloride can be converted to an enormous array of consumer and industrial applications: flooring, wire insulation, electrical transformers, home furnishings, piping, toys, bottles and containing, rainwear, light roofing and a variety of protective coatings. In 1969, CO established the first major contract with the J&R Corporation for the purchase of VCM. J&R was a major industrial manufacturer of wood and petrochemical products for the construction industry. J&R was expanding its manufacturing operations in the production of plastic pipe and pipe fittings, particularly in Europe. The use of plastic as a substitute for iron or copper pipe was gaining rapid acceptance in the construction trades, and the European market was significantly more progressive in adopting the plastic pipe. In 1976, negotiations began to extend their 1969 contract. However, at this time the market projection for VCM had changed (see Table 7-2). While the market was currently "tight"-the favorable supply situation that had existed for CO when the J&R contract was first negotiated, the supply of VCM was expected to expand rapidly over the next few years. Several of Co's competitors had announced plans for the construction of VCM manufacturing facilities that were expected to come on line in 20-30 months. Table 7-2 Projected Demand and Supply Situation Year Demand(in million pounds)Supply Capacities(in million pounds) 1972 5,127 6,600 1973 5,321 6,600 1974 5,572 6,600 1975 5,700 7,300 1976 5,900 8,450 1977 6,200 9,250 1978 6,500 9,650 1979 11,000 7,000 CO had a rated capacity of 1,000 million pounds a year. J&R, CO's second largest customer, took about 20% of CO's capacity. The largest customer took 23%. The left took between 10% and 3% of CO's capacity. If all the projected new capacity for the industry was completed and customers foresaw declining demand, CO would have difficulty selling enough VCM to run its plant profitably. In an oversupplied market, CO's plant utilization of capacity could vary from 50% to 90%. At long term average prices, CO broke even at 70% of rated capacity. Co must allow 10% of its rated capacity for maintenance, breakdowns and variations in product mix. Since most costs were fixed, profits rose and fell very rapidly: each 1% increase in capacity utilization, from 70% up to 90% of capacity, contributed 5% of the total profit that CO would earn at 90% of capacity. Each 1% decline in utilization, from 70% down to 50% of capacity, contributed 5% of the total loss that CO would incur at 50% of capacity. Below 50% of capacity, loss was so great that it did not pay to keep the plant running. CO was now running at 87% of capacity, including 4% to the spot market. You are negotiating a supply contract with representatives of J&R. Because of your concern about the J&R negotiation, you have started to explore alternatives. You estimate, from discussion with prospective customers, that you could replace 100 million pounds of J&R's 200 million pounds VCM demand a year by selling to four small, new customers. To get these replacement sales in today's market (June, 1977), you would have to make price concessions which would reduce revenues by an estimated $1 million a year below your provisional agreements with J&R. Also the replacement sales would increase Co's operating and administrative costs $150,000 a year for three years. At present, CO would have capacity for new customers only if J&R or other customers decreased their takes. Historically, during periods of industry over-capacity large buyers were tempted to split their purchases among suppliers and then played them off against each other to get lower prices. To control wide swings in plant utilization, producers generally would not sell quantities of 50 million pounds a year or more to one buyer without a long-term contract. CO could sell VCM in the spot market where prices and amounts available varied considerably from week to week. You prefer to sell on a contract basis to assure that your plant capacity is fully used. The spot market can be highly volatile. Spot prices can swing plus or minus 50% around the long-term trend. Although the trend of spot prices appears to be under downward pressure, 50% of the new VCM capacity projected for 1974-1977 nevertheless has come in place. Producers can postpone new plant constructions or shut down under-utilized capacity if they believe supply will be too far above long-term demand. Most producers, however, resist postponing new construction for fear of losing market share when demand increases. They resist shutdown when demand declines unless they foresee heavy, long-term losses, or imminent bankruptcy. The cost of your pipeline to J&R will be fully recovered by the end of the current contract. Sales to buyers without a pipeline are delivered by truck or railroad tank cars. Customers without a pipeline must allow an order lead time of one week to six months, depending upon Co's order backlog and the availability of trucks or tank cars. For annual volume of 50 million pounds the costs of a pipeline amortized over 8 years equal the costs of non-pipeline transportation. At higher volumes pipeline costs are recovered more rapidly. Pipeline maintenance and operation costs are less than 5% of non -pipeline transportation, CO's average contract price for large volume buyers like J&C was 15 cents/lb. in 1976, up from 10 cents/lb. in 1974. Actual contract prices are computed by a complex formula: Product price=B1(Feedstock)+B2 (Labour)+B3(Energy costs)+B4(Crude oil commodity costs). Each B is a negotiated coefficient. Prices have been rising primarily because of increases in crude oil commodity costs and feedstock prices. Predictions are that these costs will continue to rise because of OPEC. In the past 12 months spot prices of VCM have been as high as 24 cents/lb. and as low as 12 cents/lb. J&R buys a large quantity of VCM and CO is geared to supplying product to J&R's quality specifications. Interruptions in supply due to unacceptable quality or delayed shipments can force a customer like J&R to cut back production or shut down in two weeks. Although there are specific American Chemical Society product standards, the quality delivered can vary substantially across suppliers. When there are quality disputes, the parties may negotiate a settlement, agree to arbitration or, as a last resort, sue. Co has an excellent reputation as a reliable, high quality supplier. 2.Negotiation for the remaining issues Assume that you are in CO negotiating team, which consists of the V. P. Marketing-Europe, the VCM Marketing Manager-Europe, and the Assistant VCM Marketing Manager-Europe. You will be meeting with the J&R Corporation negotiating team, which consists of the J&R V. P. Europe, the Purchasing Manager, and the Assistant Purchasing Manager. Time has passed since your last meeting and it is now June 24, 1977. If neither party gives notice of termination(that is, by June 30, 1977)in 180 days, the "evergreen" clause takes effect. Evergreen means that after December 31, 1977, the contract will be renewed annually with its present terms unless either party gives notice of termination. Co had agreed to make changes on the original contract. Both sides had reached the provisional agreement on price, minimum quantities, and length of new contract (three years from date of signing) and metering. Three issues are still in dispute: (1) Most favored nation's clause(MFN):(2) Meet the competition(MTC):(3) Right to resell the product(RTR). Price: The formula price would be adjusted downward by approximately 0.85 cents per pound. Minimum quantities: J&R suggested minimum quantities of 205 million pounds in the first year of the contract and 210 million pounds in the second year and 220 million pounds in the third. CO considered the minimum quantities were ridiculously low, however, they agreed to the purchase schedule. Length of new contract: The two sides agreed to a three-year contract renewal instead of suggested five years by CO. Metering: J&R stated that the pipeline sending the product was leaking. If the new metering system could be installed they would feel infinitely more comfortable. Finally CO agreed to remeter the pipeline. The remaining issues: (1) Most favoured nation's clause. If CO negotiated with another purchaser a more favorable price for VCM than J&R was receiving now, CO would guarantee that J&R would receive that price as well. (2)Meet the competition. Co would willingly meet any lower price on VCM offered by a competitor, in order to maintain the J&R relationship. (3)Right to resell the product. J&R wanted the contractual right to resell the product if it could not use the minimum amount. Requirement for the Negotiation Organize your virtual/pretend negotiation teams according to the roles in the case. Work out your negotiation plan, including each other's interests, negotiating power, the most wanted interests and interests you can concession, other options and best alternatives

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock