Question: Please would someone help? {yt} is assumed to be a series of quarterly unemployment rates. Assume we employ the following two AR(5) models to fit

Please would someone help?

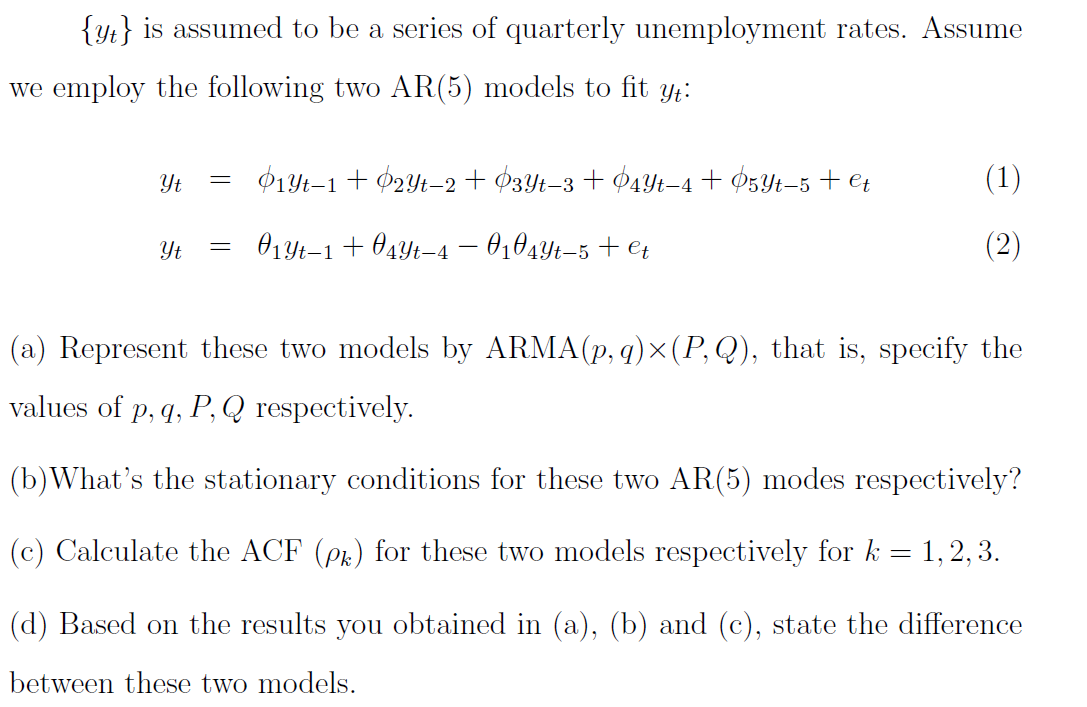

{yt} is assumed to be a series of quarterly unemployment rates. Assume we employ the following two AR(5) models to fit yt: yt = $19t-1 + (29t-2 + $34/t-3 + $4yt-4 + $54t-5 + et (1) yt = 019/t-1+ 049t-4 - 0104yt-5 + et (2) (a) Represent these two models by ARMA(p, q) x (P, Q), that is, specify the values of p, q, P, Q respectively. (b) What's the stationary conditions for these two AR(5) modes respectively? (c) Calculate the ACF (PR) for these two models respectively for k = 1, 2, 3. (d) Based on the results you obtained in (a), (b) and (c), state the difference between these two models

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock