Question: Please write a C++ code for the cumulative normal distribution using the given code. Please read the whole question and then answer. This is the

Please write a C++ code for the cumulative normal distribution using the given code. Please read the whole question and then answer. This is the 5th time I'm posting this same question.

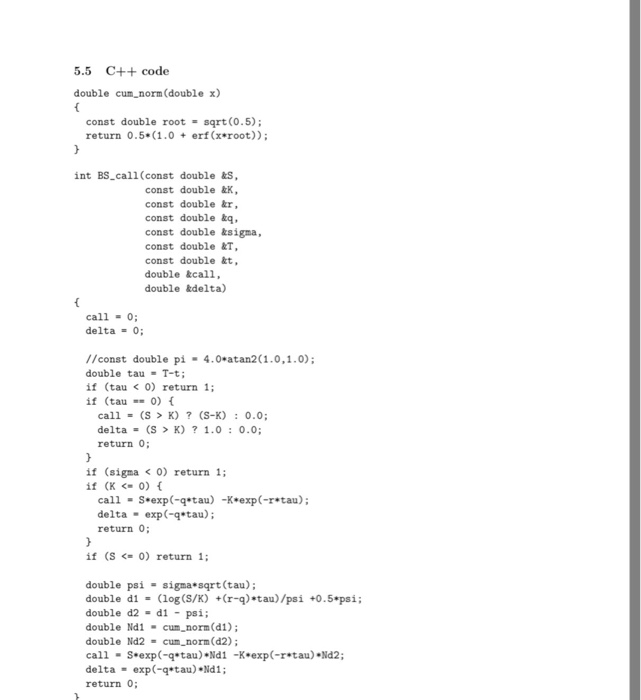

Please write a C++ code for the cumulative normal distribution using the given code. Please read the whole question and then answer. This is the 5th time I'm posting this same question. 5 Question 5 5.1 (information): Black-Scholes formula Consider a European call and put on a stock, with strike K and expiration time T, where Tt .Suppose the stock price is S at the current time t. The stock pays a continuous dividends with a yield q. The risk free interest rate is r. The volatility of the stock is .We require the cumulative Normal distribution N(), which is given by N(z)- 212 du 1. The function N(x) is monotonically increasing, with N(-x) = 0, N(x) = 1 and 0

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock