Question: Please write the solution out with explanation. Thank you! Using Exhibit 5.7, calculate the one-, three-, and six-month forward premium or discount for the U.S.

Please write the solution out with explanation. Thank you!

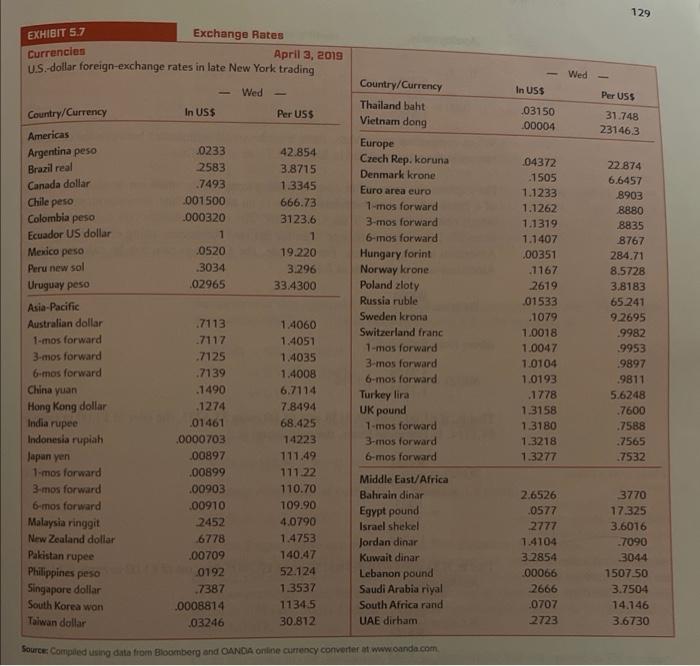

Using Exhibit 5.7, calculate the one-, three-, and six-month forward premium or discount for the U.S. dollar versus the British pound using European term quotations. For simplicity, assume each month has 30 days. What is the interpretation of your results? 129 EXHIBIT 5.7 Exchange Rates Currencien April 3, 2019 US. dollar foreign-exchange rates in late New York trading Source: Compied using data fiom Bloonberg and OANGA onine aunency converter mt www andacom

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock