Question: pls answer this and i will give a like asap Hedge with HSI Index You are a Hong-Kong-based manager of an equity portfolio valued at

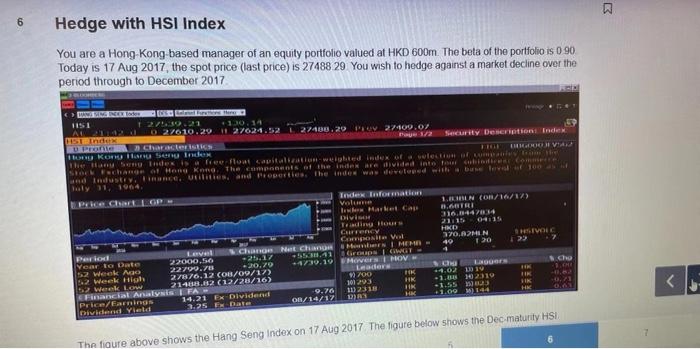

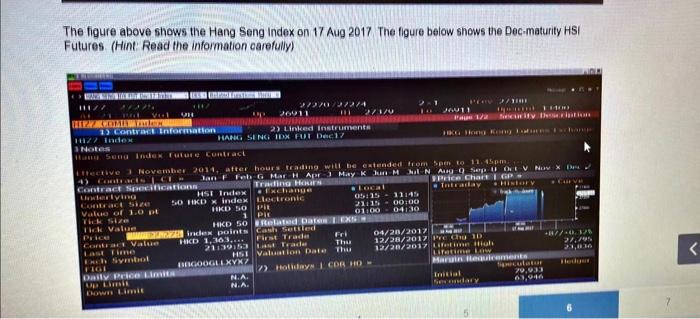

Hedge with HSI Index You are a Hong-Kong-based manager of an equity portfolio valued at HKD600m. The beta of the portfolio is 090 Today is 17 Aug 2017, the spot price (last price) is 2748829 You wish to hedge against a market decine over the parind throuih th hacamher 2017 The figure above shows the Hang Seng indox on 17 Aug 2017 . The figure below shows be Dec-maturity HSI Futures. (Hint: Read the information carefuly) 1. To fully hedge the portlolio, you need to (long or short) HSI future contracts The number of contracts needed are (round to the nearest integer) 2. If the Hang Seng index is 27,100 in Dec 2017, calculate the followings: - The value of the share portfolio is In HKD (round to the nearest infeger) - The gain (loss) on futures is in HKD (add negative sign for loss)1rounglto the nearest integer) - The net position of your porttolio after hedging is in HKD (roesnd to the nearest integer) 1. To fully hedge the portfolio, you need The number of contracts needed are (long or short) HSI future contract (round to the nearest integer) 2. If the Hang Seng index is 27,100 in Dec 2017, calculate the followings: - The value of the share portfolio is in HKD (round to the nearest integer) - The gain (loss) on futures is in HKD (add negative "-" sign for loss)(rounfito the nearest integer) - The net position of your portfolio after hedging is in HKD (round to the nearest integer)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts