Question: Pls help Exercise 2.47. Consider the one-step binomial model with stock prices hav- ing d=1/u. We can price ATM calls by T (US K) =

Pls help

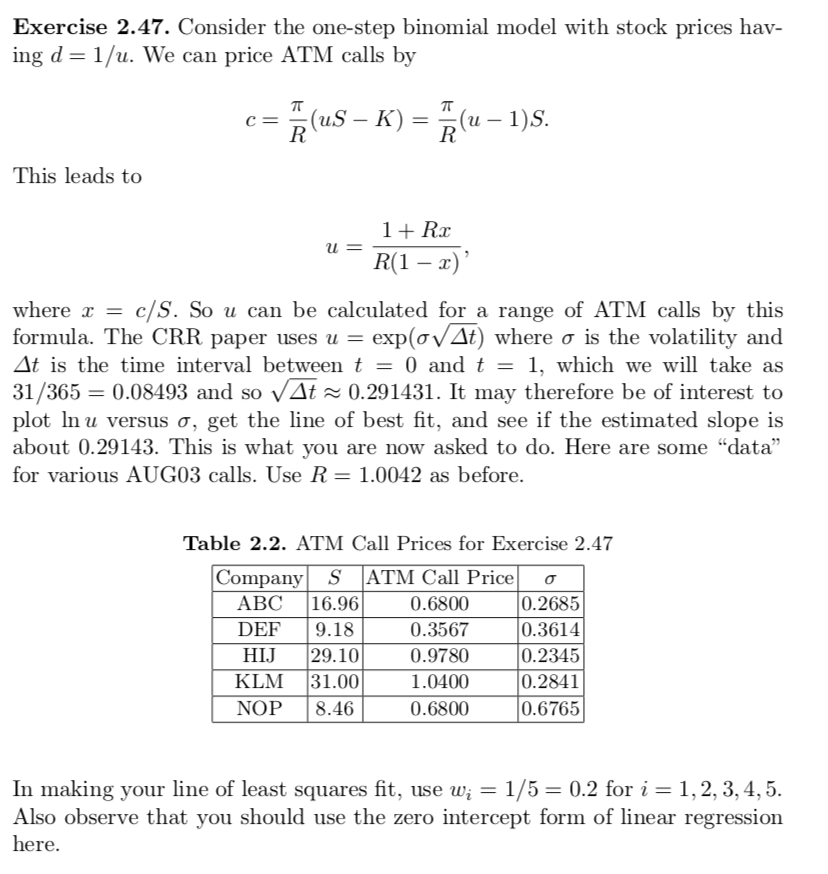

Exercise 2.47. Consider the one-step binomial model with stock prices hav- ing d=1/u. We can price ATM calls by T (US K) = (u 1).. This leads to = 1+ Rx u R(1 x)' where x c/S. So u can be calculated for a range of ATM calls by this formula. The CRR paper uses u = explov At) where o is the volatility and At is the time interval between t = 0 and t = 1, which we will take as 31/365 = 0.08493 and so At = 0.291431. It may therefore be of interest to plot In u versus o, get the line of best fit, and see if the estimated slope is about 0.29143. This is what you are now asked to do. Here are some "data" for various AUG03 calls. Use R=1.0042 as before. Table 2.2. ATM Call Prices for Exercise 2.47 Company S ATM Call Price o ABC 16.96 0.6800 0.2685 DEF 9.18 0.3567 0.3614 HIJ 29.10 0.9780 0.2345 KLM 31.00 1.0400 0.2841 NOP 8.46 0.6800 0.6765 In making your line of least squares fit, use w; = 1/5 = 0.2 for i = 1,2,3,4,5. Also observe that you should use the zero intercept form of linear regression here. Exercise 2.47. Consider the one-step binomial model with stock prices hav- ing d=1/u. We can price ATM calls by T (US K) = (u 1).. This leads to = 1+ Rx u R(1 x)' where x c/S. So u can be calculated for a range of ATM calls by this formula. The CRR paper uses u = explov At) where o is the volatility and At is the time interval between t = 0 and t = 1, which we will take as 31/365 = 0.08493 and so At = 0.291431. It may therefore be of interest to plot In u versus o, get the line of best fit, and see if the estimated slope is about 0.29143. This is what you are now asked to do. Here are some "data" for various AUG03 calls. Use R=1.0042 as before. Table 2.2. ATM Call Prices for Exercise 2.47 Company S ATM Call Price o ABC 16.96 0.6800 0.2685 DEF 9.18 0.3567 0.3614 HIJ 29.10 0.9780 0.2345 KLM 31.00 1.0400 0.2841 NOP 8.46 0.6800 0.6765 In making your line of least squares fit, use w; = 1/5 = 0.2 for i = 1,2,3,4,5. Also observe that you should use the zero intercept form of linear regression here

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts