Question: pls show work Estimating Inventory Loss Using Gross Profit Method The accounting records of Butler Company reveal the following information. Inventory, January 1 $44,000 Purchases

pls show work

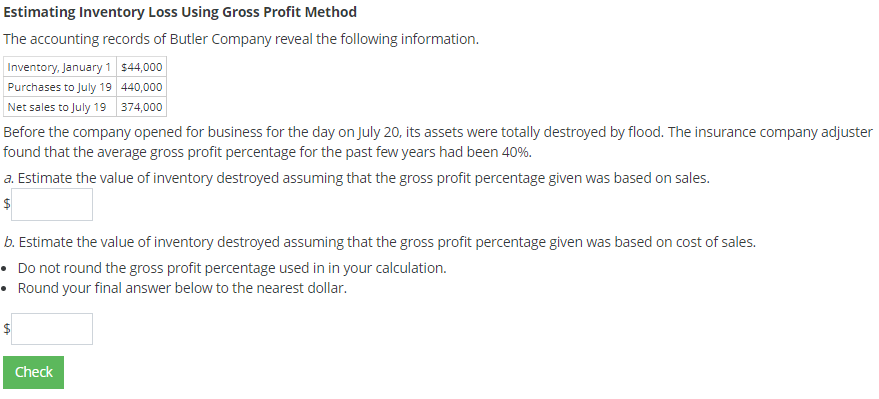

Estimating Inventory Loss Using Gross Profit Method The accounting records of Butler Company reveal the following information. Inventory, January 1 $44,000 Purchases to July 19 440,000 Net sales to July 19 374,000 Before the company opened for business for the day on July 20, its assets were totally destroyed by flood. The insurance company adjuster found that the average gross profit percentage for the past few years had been 40%. a. Estimate the value of inventory destroyed assuming that the gross profit percentage given was based on sales. $ b. Estimate the value of inventory destroyed assuming that the gross profit percentage given was based on cost of sales. Do not round the gross profit percentage used in in your calculation. Round your final answer below to the nearest dollar. $ Check

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts