Question: plz answer as fast as possible 2. Consider the following simplified Arbitrage Pricing Theory APT model (16 Marks) Factor Market Interest Spread Yield spread Expected

plz answer as fast as possible

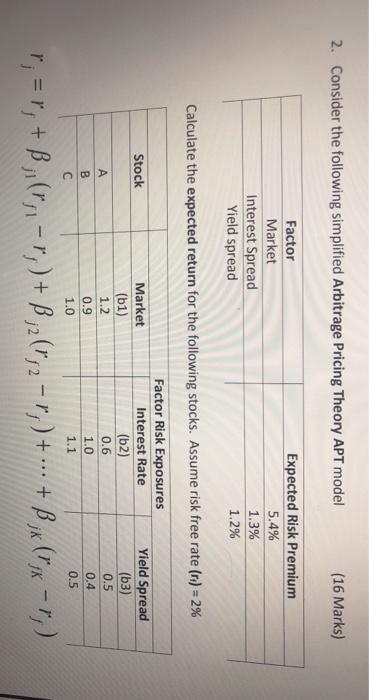

2. Consider the following simplified Arbitrage Pricing Theory APT model (16 Marks) Factor Market Interest Spread Yield spread Expected Risk Premium 5.4% 1.3% 1.2% Calculate the expected return for the following stocks. Assume risk free rate (n) = 2% Stock Factor Risk Exposures Interest Rate (62) 0.6 1.0 1.1 Market (61) 1.2 0.9 1.0 B Yield Spread (63) 0.5 0.4 0.5 r;=r; + B ;(", - r,)+B;2(";2 - r.) + ... + Bix ("/x-",)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock