Question: Plz answer it as soooon as possible ,, need hand written 11. {a} An insurance company has a portfolio of independent policies with mate claims

Plz answer it as soooon as possible ,, need hand written

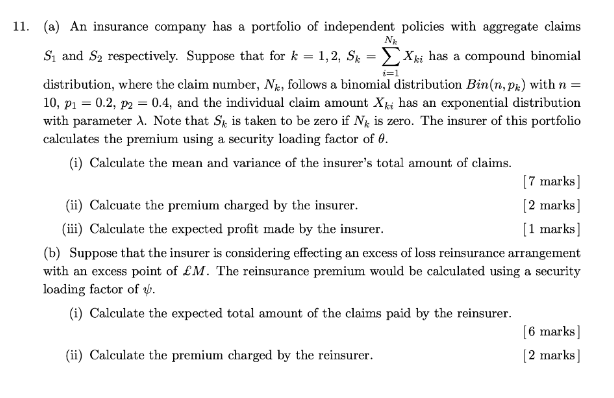

11. {a} An insurance company has a portfolio of independent policies with mate claims We 5'1 and 32 prospectively. Suppose that for Ir = 1,21 3!: = 23],; has a compound binomial i=1 distribution, where the claim number, Np\" follows a binomial distribution Births, pg} with r: = 1|]I p1 = n.2, p; = [1.4, and the individual claini amount EH has an exponential distribution with parameter 1. Note that 3;; is taken. to be zero if N3: is zero. The insurer of this portfolio calculates the premium using a security loading factor of d. {i} Calculate the mean and variance ofthe insurer's total amount. of claims. ['F marks] [ii] Caleuate the premium charged by the insurer, [2 marks] {iii} Calculate the elm-acted prot made by the insurer. [1 marks] {b} Bop-pose that the insurer is considering effecting an excess of loss reinsurance arrangement with so excess point of 1\". The reinsurance premium would be calculated using a security loading faetor of sir. (i) Calculate the expected total amount of the claims paid by the reinsurer. [ii marks] [ii] Calculate the premium charged by the reinsurer. [2 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts