Question: PlZ give brief introduction about each answer t 2-33. 70 LO 2-4 Chapter Two Wren, Inc., a nonpublic company. retaims Ying and Company CPA to

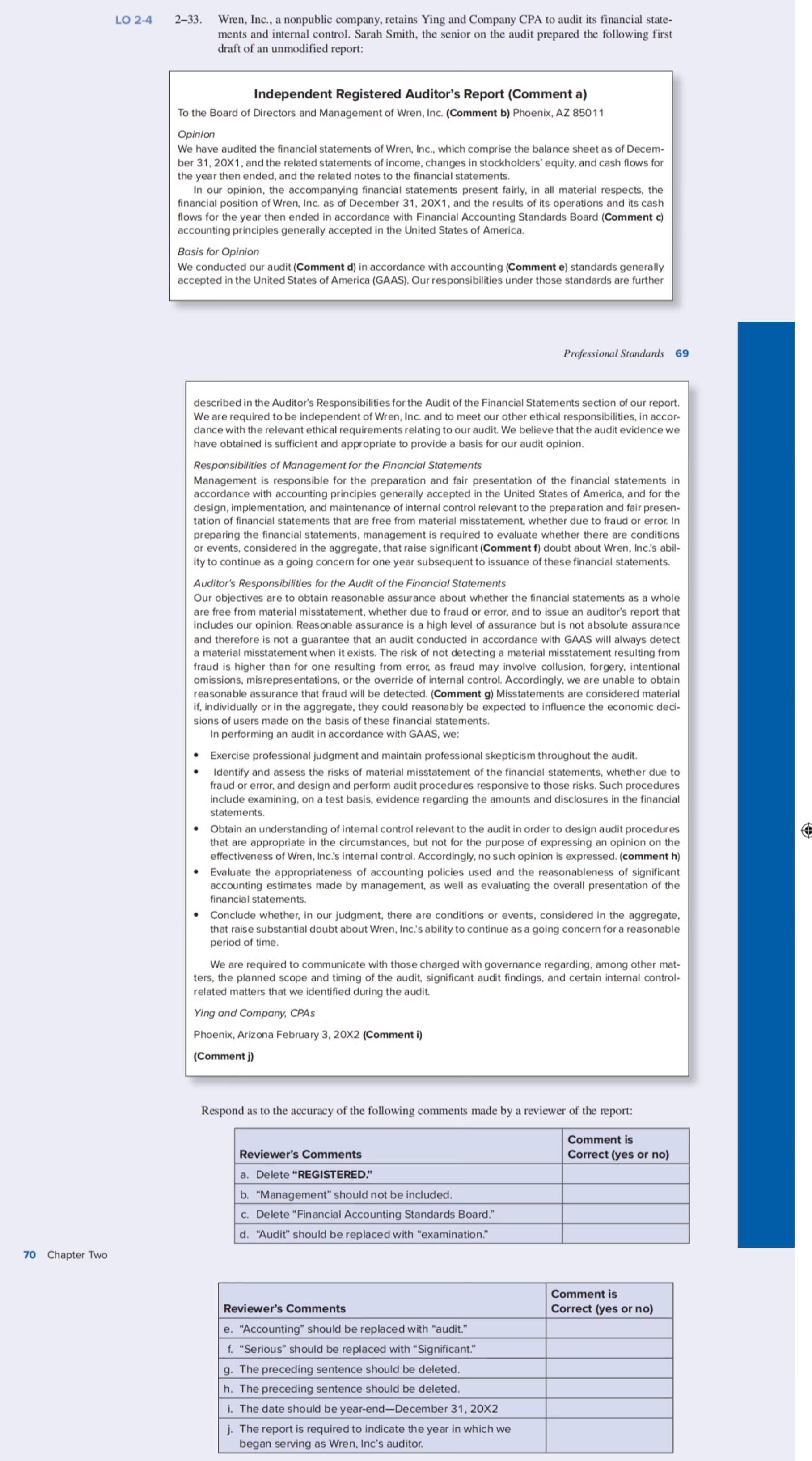

2-33. 70 LO 2-4 Chapter Two Wren, Inc., a nonpublic company. retaims Ying and Company CPA to audit its financial state- ments and internal control. Sarah Smith, the senior on the audit prepared tlr following first draft of an unmodified report: Independent Registered Auditor's Report (Comment a) To the Board of Directors and Management of Wren, Inc (Comment b) Phoenix, AZ 85011 We have audited the financial statements of Wren. Inc.. which comprise the balance sheet as of Decem- ber 31. 20XI , and the related statements of income, changes in stockholders' equity, and cash flovvs for the year then ended, and the related notes to the financial statements. In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of Wren, Inc. as of December 31. 20XI . and the results of its operations and its cash flows for the year then ended in accordance with Financial Accounting Standards Board (Comment c) accounting principles generally accepted in the United States of America. Basis for Opinion We conducted our audit (Comment d) in accordance with accounting (Comment e) standards generally accepted in the United States of America (GAAS). Our responsibilities under those standards are further Professional Standards 69 described in the Auditor's Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of Wren, Inc. and to meet our other ethical responsibilities. in accor- dance with the relevant ethical requirements relating to our audit. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Responsibilities of Management for the Financial Statements Management is responsible for the preparation and fair presentation of the financial statements in accordance with accounting principles generally accepted in the United States of America. and for the design. implementation. and maintenance of internal control relevant to the preparation and fair presen- tation of financial statements that are free from material misstatement. whether due to fraud or error. In preparing the financial statements, management is required to evaluate whether there are conditions or events. considered in the aggregate. that raise significant (Comment f) doubt about Wren. Inc.'s abil- ity to continue as a going concern for one year subsequent to issuance of these financial statements. Auditor's Responsibilities for the Audit of the Financial Statements Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement. whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance but is not absolute assurance and therefore is not a guarantee that an audit conducted in accordance with GAAS will always detect a material misstatement when it exists. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error. as fraud may involve collusion. forgery. intentional omissions. misrepresentations, or the override of internal control. Accordingly. we are unable to obtain reasonable assurance that fraud will be detected. (Comment g) Misstatements are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic deci- sions of users made on the basis of these financial statements. In performing an audit in accordance with GAAS. we: Exercise professional judgment and maintain professional skepticism throughout the audit. Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining. on a test basis, evidence regarding the amounts and disclosures in the financial statements. Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances. but not for the purpose of expressing an opinion on the effectiveness of Wren, Inc.'s internal control. Accordingly, no such opinion is expressed. (comment h) Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management. as well as evaluating the overall presentation of the financial statements. Conclude whether. in our judgment. there are conditions or events. considered in the aggregate. that raise substantial doubt about Wren. Inc.'s ability to continue as a going concern for a reasonable period of time. We are required to communicate with those charged with governance regarding, among other mat- ters, the planned scope and timing of the audit. significant audit findings, and certain internal control- related matters that we identified during the audit Ying and Compony, CPAs Phoenix. Arizona February 3.20X2 (Comment i) (Comment j) Respond as to the accuracy of the following comments made by a reviewer of the report: Reviewer's Comments a. Delete "REGISTERED." b. "Management" should not be included. c. Delete "Financial Accounting Standards Board." d. "Audit" should be replaced with "examination." Reviewer's Comments "Accounting" should be replaced with "audit." e. f. "Serious" should be replaced with "Significant." The preceding sentence should be deleted. g. The preceding sentence should be deleted. h. The date should be year-endDecember 31. 20X2 The report is required to indicate the year in which we j. began serving as Wren, Inc's auditor. Comment is Correct (yes or no) Comment is Correct (yes or no)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts