Question: PLZ HELP onsider a speculator seeking to trade volatility using American put options written against a dividend aying stock. To do so she seeks an

PLZ HELP

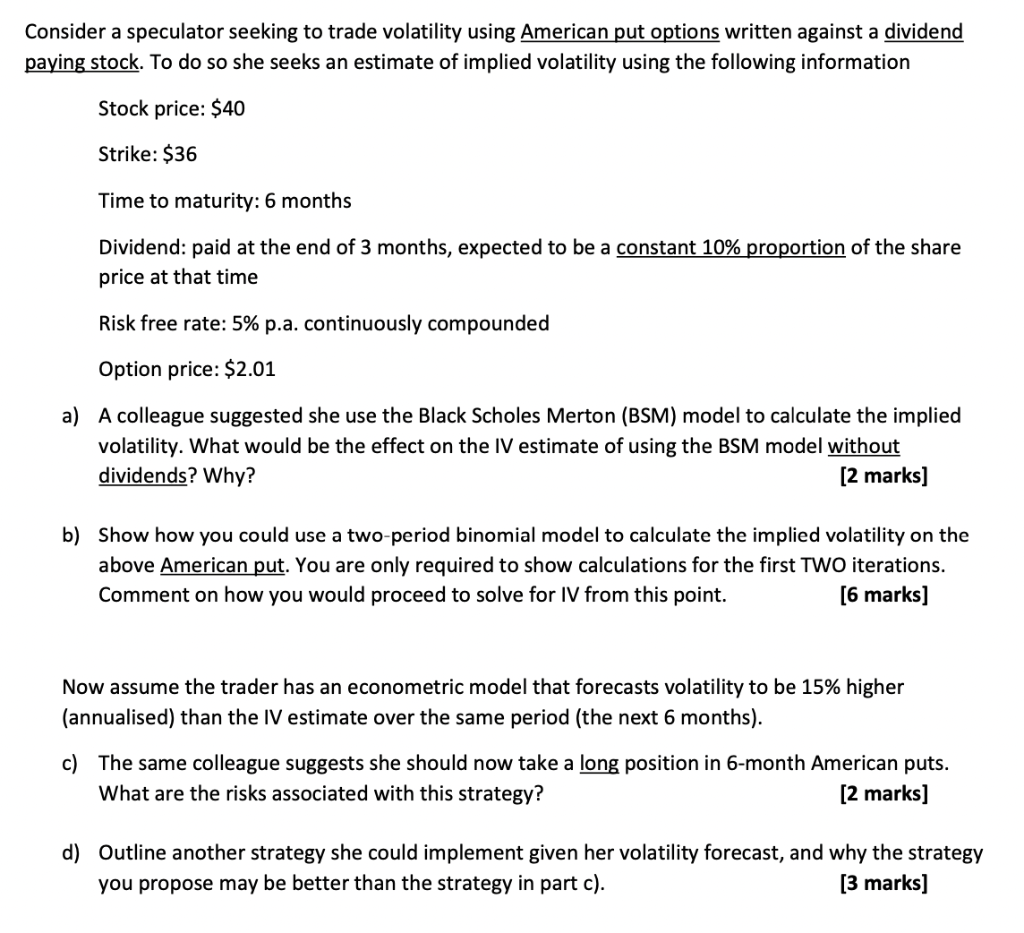

onsider a speculator seeking to trade volatility using American put options written against a dividend aying stock. To do so she seeks an estimate of implied volatility using the following information Stock price: $40 Strike: \$36 Time to maturity: 6 months Dividend: paid at the end of 3 months, expected to be a constant 10% proportion of the share price at that time Risk free rate: 5% p.a. continuously compounded Option price: \$2.01 a) A colleague suggested she use the Black Scholes Merton (BSM) model to calculate the implied volatility. What would be the effect on the IV estimate of using the BSM model without dividends? Why? [2 marks] b) Show how you could use a two-period binomial model to calculate the implied volatility on the above American put. You are only required to show calculations for the first TWO iterations. Comment on how you would proceed to solve for IV from this point. [6 marks] Now assume the trader has an econometric model that forecasts volatility to be 15% higher (annualised) than the IV estimate over the same period (the next 6 months). c) The same colleague suggests she should now take a long position in 6-month American puts. What are the risks associated with this strategy? [2 marks] d) Outline another strategy she could implement given her volatility forecast, and why the strategy you propose may be better than the strategy in part c). [3 marks] onsider a speculator seeking to trade volatility using American put options written against a dividend aying stock. To do so she seeks an estimate of implied volatility using the following information Stock price: $40 Strike: \$36 Time to maturity: 6 months Dividend: paid at the end of 3 months, expected to be a constant 10% proportion of the share price at that time Risk free rate: 5% p.a. continuously compounded Option price: \$2.01 a) A colleague suggested she use the Black Scholes Merton (BSM) model to calculate the implied volatility. What would be the effect on the IV estimate of using the BSM model without dividends? Why? [2 marks] b) Show how you could use a two-period binomial model to calculate the implied volatility on the above American put. You are only required to show calculations for the first TWO iterations. Comment on how you would proceed to solve for IV from this point. [6 marks] Now assume the trader has an econometric model that forecasts volatility to be 15% higher (annualised) than the IV estimate over the same period (the next 6 months). c) The same colleague suggests she should now take a long position in 6-month American puts. What are the risks associated with this strategy? [2 marks] d) Outline another strategy she could implement given her volatility forecast, and why the strategy you propose may be better than the strategy in part c). [3 marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts