Question: PLZ PLZ HELP The semi-annually compounded swap rates are as shown in Figure 1 below: Calculate the term structure of interest rates. An AA-rated firm

PLZ PLZ HELP

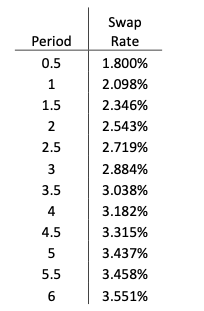

The semi-annually compounded swap rates are as shown in Figure 1 below:

-

Calculate the term structure of interest rates.

-

An AA-rated firm issues a 3.6% p.a. six-year semi-annual pay bond. Calculate the bonds

-

Price,

-

Yield,

-

Duration, and

-

Convexity.

-

-

If interest rates exhibit volatility of 12% p.a. across the yield curve, calculate the arbitrage-free interest rate grid using the Black-Derman-Toy (BDT) methodology.

Period 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 Swap Rate 1.800% 2.098% 2.346% 2.543% 2.719% 2.884% 3.038% 3.182% 3.315% 3.437% 3.458% 3.551% Period 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 Swap Rate 1.800% 2.098% 2.346% 2.543% 2.719% 2.884% 3.038% 3.182% 3.315% 3.437% 3.458% 3.551%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts