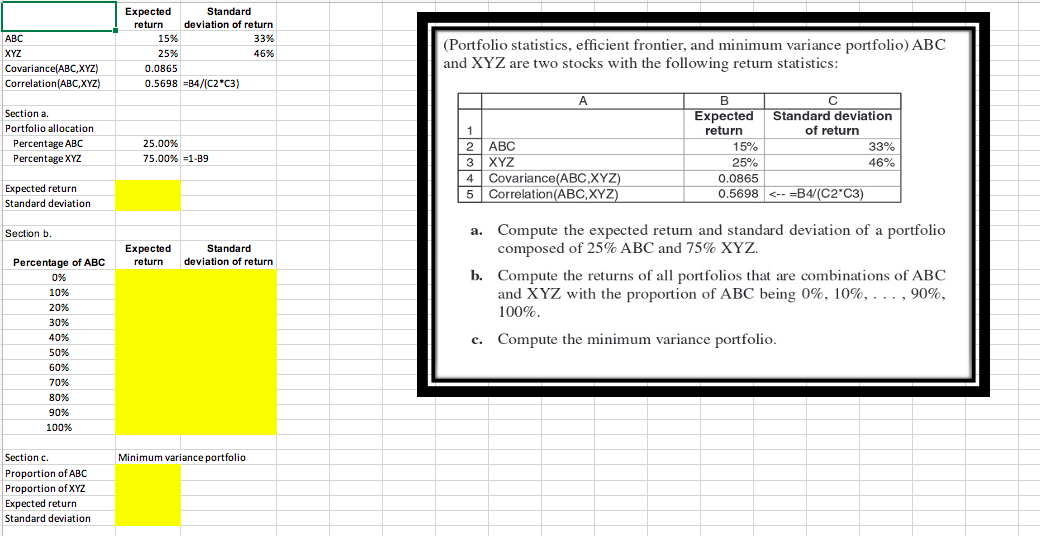

Question: (Portfolio statistics, efficient frontier, and minimum variance portfolio) ABC and XYZ are two stocks with the following return statistics: a. Compute the expected return and

(Portfolio statistics, efficient frontier, and minimum variance portfolio) ABC and XYZ are two stocks with the following return statistics: a. Compute the expected return and standard deviation of a portfolio composed of 25%ABC and 75%XYZ. b. Compute the returns of all portfolios that are combinations of ABC and XYZ with the proportion of ABC being 0%,10%,,90%, 100%. c. Compute the minimum variance portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock