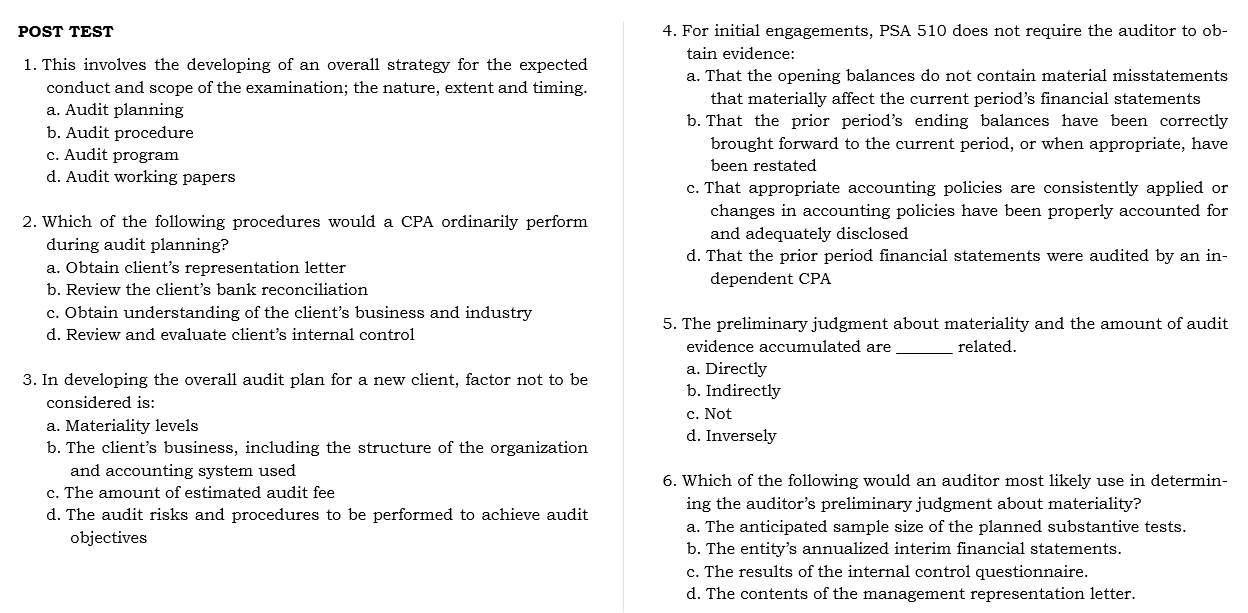

Question: POST TEST 1. This involves the developing of an overall strategy for the expected conduct and scope of the examination; the nature, extent and timing.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock