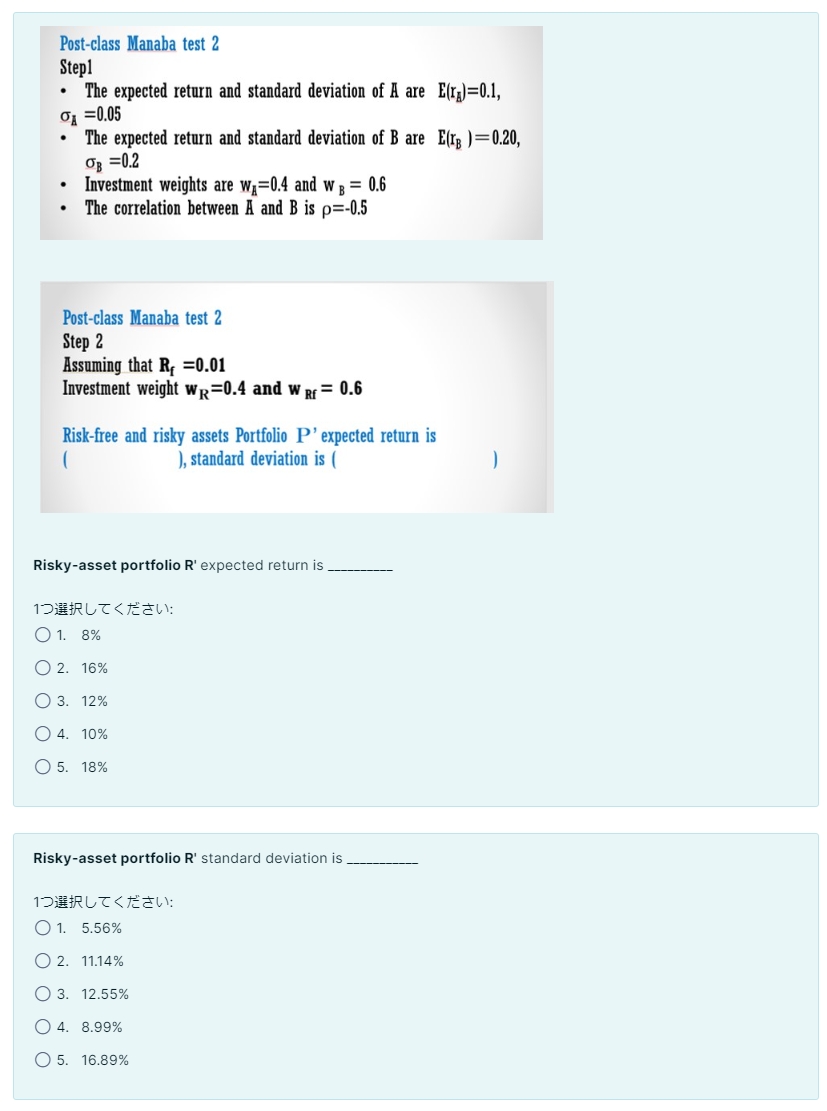

Question: Post-class Manaba test 2 Stepl 1=0.05 - The expected return and standard deviation of B are E(rB)=0.20, B=0.2 - Investment weights are wA=0.4 and wB=0.6

Post-class Manaba test 2 Stepl 1=0.05 - The expected return and standard deviation of B are E(rB)=0.20, B=0.2 - Investment weights are wA=0.4 and wB=0.6 - The correlation between A and B is =0.5 Post-class Manaba test 2 Step 2 Assuming that Rf=0.01 Investment weight wR=0.4 and wRf=0.6 Risk-free and risky assets Portfolio P expected return is ), standard deviation is ( Risky-asset portfolio R expected return is 1: 1. 8% 2. 16% 3. 12% 4. 10% 5. 18% Risky-asset portfolio R standard deviation is 1: 1. 5.56% 2. 11.14% 3. 12.55% 4. 8.99% 5. 16.89% Risky- and risk-free-asset portfolio P expected return is 1: 1. 22% 2. 12% 3. 18% 4. 15% 5. 7% Risky- and risk-free-asset portfolio P standard deviation is 1: 1. 4.45% 2. 1.89% 3. 9.45% 4. 2.55% 5. 4.88%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts