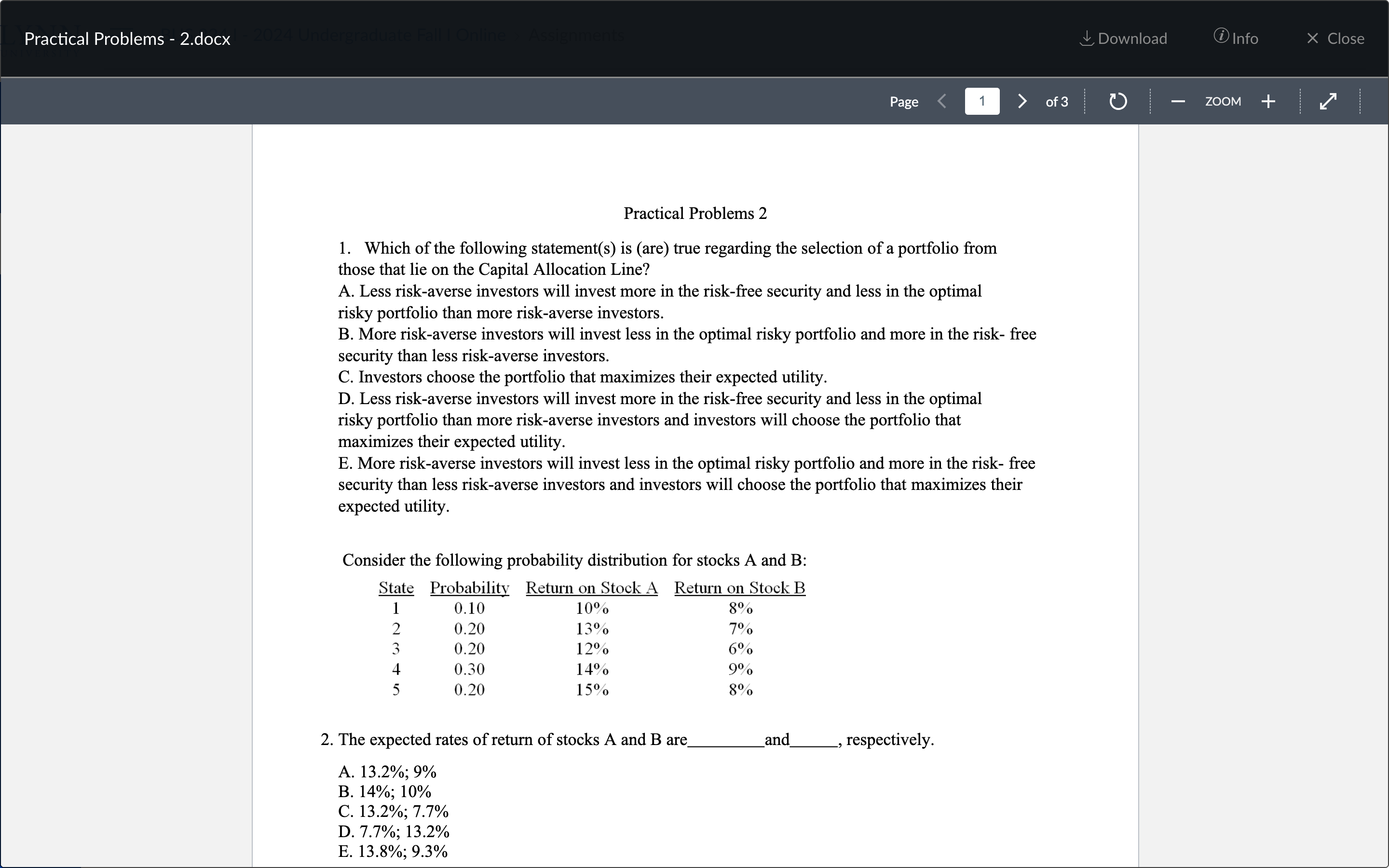

Question: Practical Problems - 2.docx N Practical Problems 2 1. Which of the following statement(s) is (are) true regarding the selection of a portfolio from those

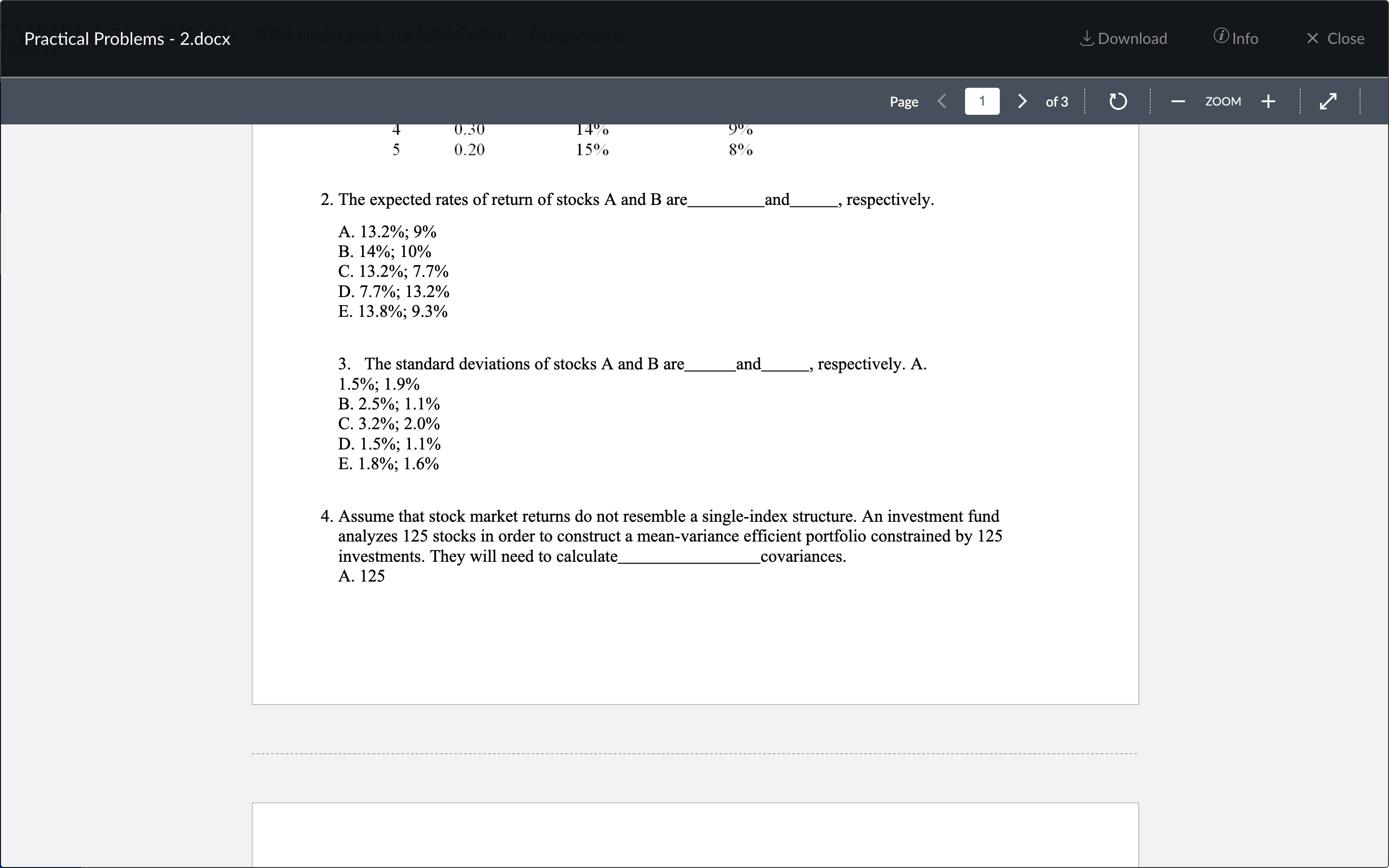

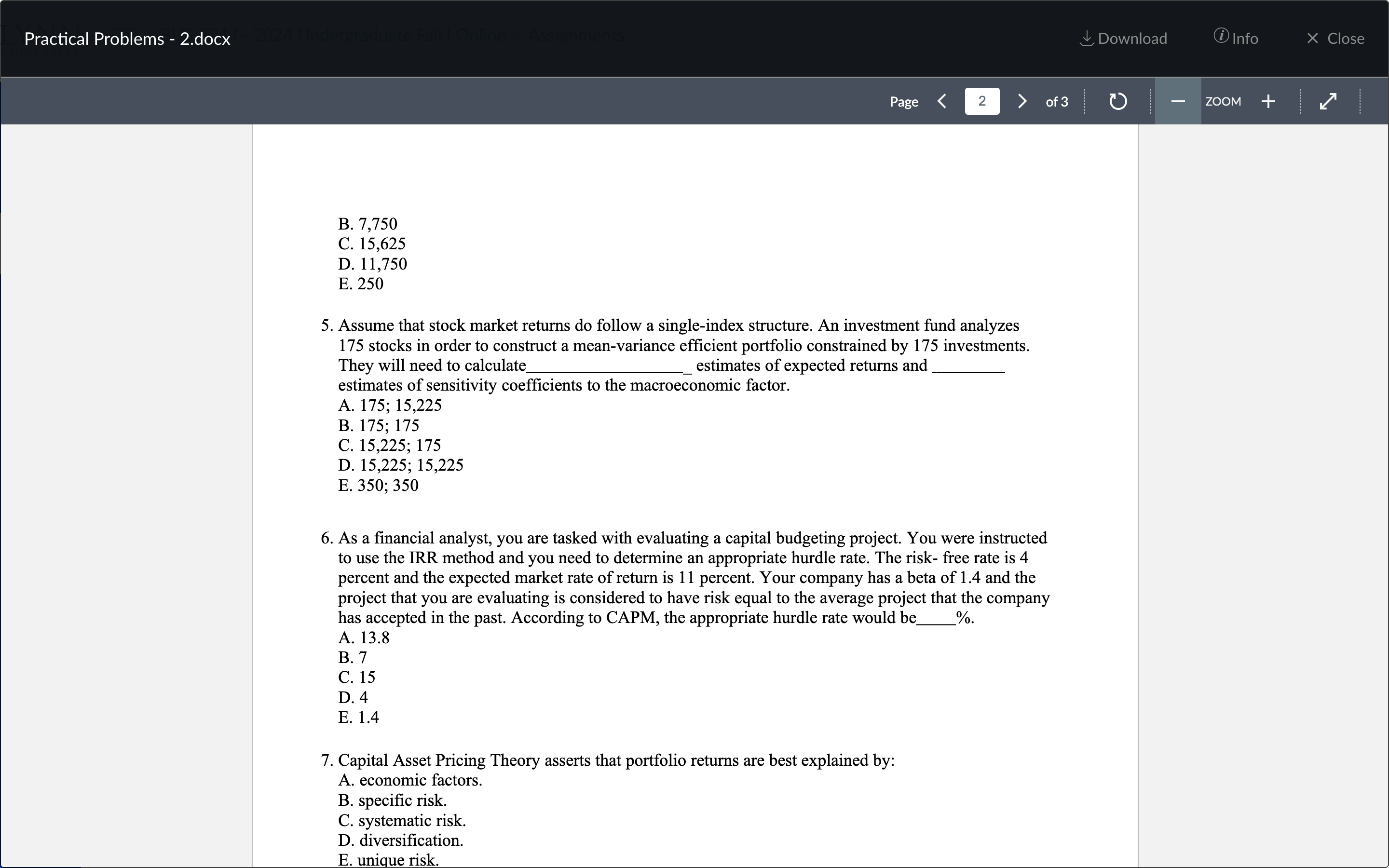

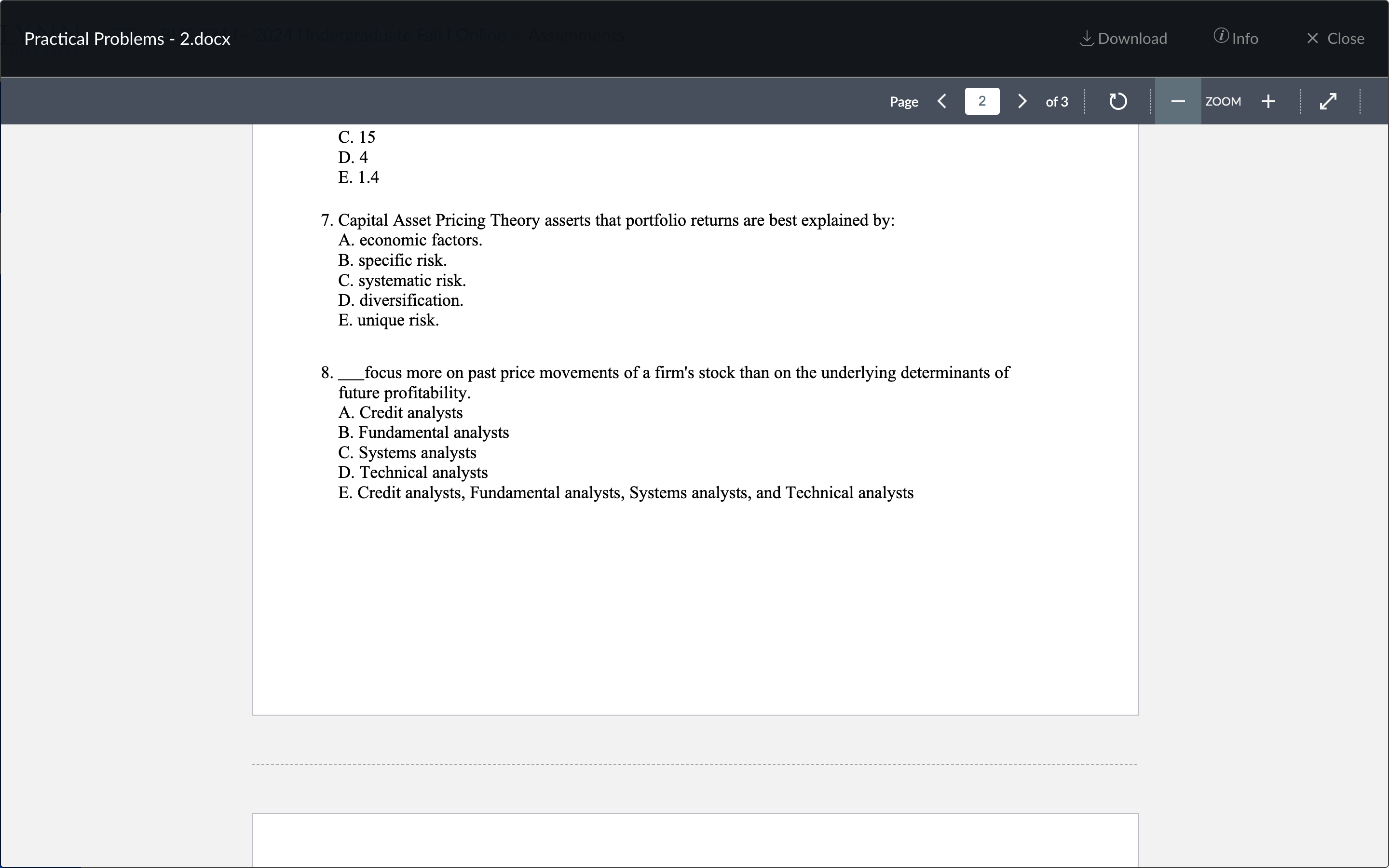

Practical Problems - 2.docx N Practical Problems 2 1. Which of the following statement(s) is (are) true regarding the selection of a portfolio from those that lie on the Capital Allocation Line? A. Less risk-averse investors will invest more in the risk-free security and less in the optimal risky portfolio than more risk-averse investors. B. More risk-averse investors will invest less in the optimal risky portfolio and more in the risk- free security than less risk-averse investors. C. Investors choose the portfolio that maximizes their expected utility. D. Less risk-averse investors will invest more in the risk-free security and less in the optimal risky portfolio than more risk-averse investors and investors will choose the portfolio that maximizes their expected utility. E. More risk-averse investors will invest less in the optimal risky portfolio and more in the risk- free security than less risk-averse investors and investors will choose the portfolio that maximizes their expected utility. Consider the following probability distribution for stocks A and B: State Probability Return on Stock A Return on Stock B 1 0.10 10% 8% 2 0.20 3% 7% 3 0.20 12% 6% 4 0.30 14% 9% 5 0.20 15% 8% The expected rates of return of stocks A and B are and, , respectively. A. 13.2%; 9% B. 14%; 10% C. 13.2%; 7.7% D. 7.7%; 13.2% E. 13.8%;9.3% Practical Problems - 2.docx 2. The expected rates of return of stocks A and B are and, , respectively. A. 13.2%; 9% B. 14%; 10% C. 13.2%; 7.7% D. 7.7%; 13.2% E. 13.8%; 9.3% 3. The standard deviations of stocks A and B are and, , respectively. A. 1.5%; 1.9% B.2.5%; 1.1% C.3.2%;2.0% D. 1.5%; 1.1% E. 1.8%; 1.6% 4. Assume that stock market returns do not resemble a single-index structure. An investment fund analyzes 125 stocks in order to construct a mean-variance efficient portfolio constrained by 125 investments. They will need to calculate covariances. A. 125 Practical Problems - 2.docx w N = B. 7,750 C. 15,625 D. 11,750 E. 250 . Assume that stock market returns do follow a single-index structure. An investment fund analyzes 175 stocks in order to construct a mean-variance efficient portfolio constrained by 175 investments. They will need to calculate _ estimates of expected returns and estimates of sensitivity coefficients to the macroeconomic factor. A. 175; 15,225 B. 175; 175 C. 15,225; 175 D. 15,225; 15,225 E. 350; 350 . As a financial analyst, you are tasked with evaluating a capital budgeting project. You were instructed to use the IRR method and you need to determine an appropriate hurdle rate. The risk- free rate is 4 percent and the expected market rate of return is 11 percent. Your company has a beta of 1.4 and the project that you are evaluating is considered to have risk equal to the average project that the company has accepted in the past. According to CAPM, the appropriate hurdle rate would be____ %. A. 138 7 15 4 .1.4 oaow Jes] . Capital Asset Pricing Theory asserts that portfolio returns are best explained by: A. economic factors. B. specific risk. C. systematic risk. D. diversification. E. unique risk. Practical Problems - 2.docx C. 15 D. 4 E. 14 = . Capital Asset Pricing Theory asserts that portfolio returns are best explained by: A. economic factors. B. specific risk. C. systematic risk. D. diversification. E. unique risk. 90 ___focus more on past price movements of a firm's stock than on the underlying determinants of future profitability. A. Credit analysts B. Fundamental analysts C. Systems analysts D. Technical analysts E. Credit analysts, Fundamental analysts, Systems analysts, and Technical analysts Practical Problems - 2.docx 9. The debate over whether markets are efficient will probably never be resolved because of A. the lucky event issue B. the magnitude issue C. the selection bias issue D. the lucky event issue, magnitude issue, and selection bias issue E. None of these answers are correct. 10. Conventional theories presume that investors, and behavioral finance presumes that they. A. are irrational; are irrational B. are rational; may not be rational C. are rational; are rational D. may not be rational; may not be rational E. may not be rational; are rational 11. Tests of multifactor models indicate A. the single-factor model has better explanatory power in estimating security returns. B. macroeconomic variables have no explanatory power in estimating security returns. C. it may be possible to hedge some economic factors that affect future consumption risk with appropriate portfolios. D. multifactor models do not work. E. None of these is correct. 12. was the grandfather of technical analysis. A. Harry Markowitz B. William Sharpe C. Charles Dow D. Benjamin Graham E. None of these is correct. https://lynn.instructure.com/files/5831317/download?download_frd=1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!