Question: Preparing a consolidated income statement-Cost method with noncontrolling interest and AAP A parent company purchased a 90% controlling interest in its subsidiary several years ago.

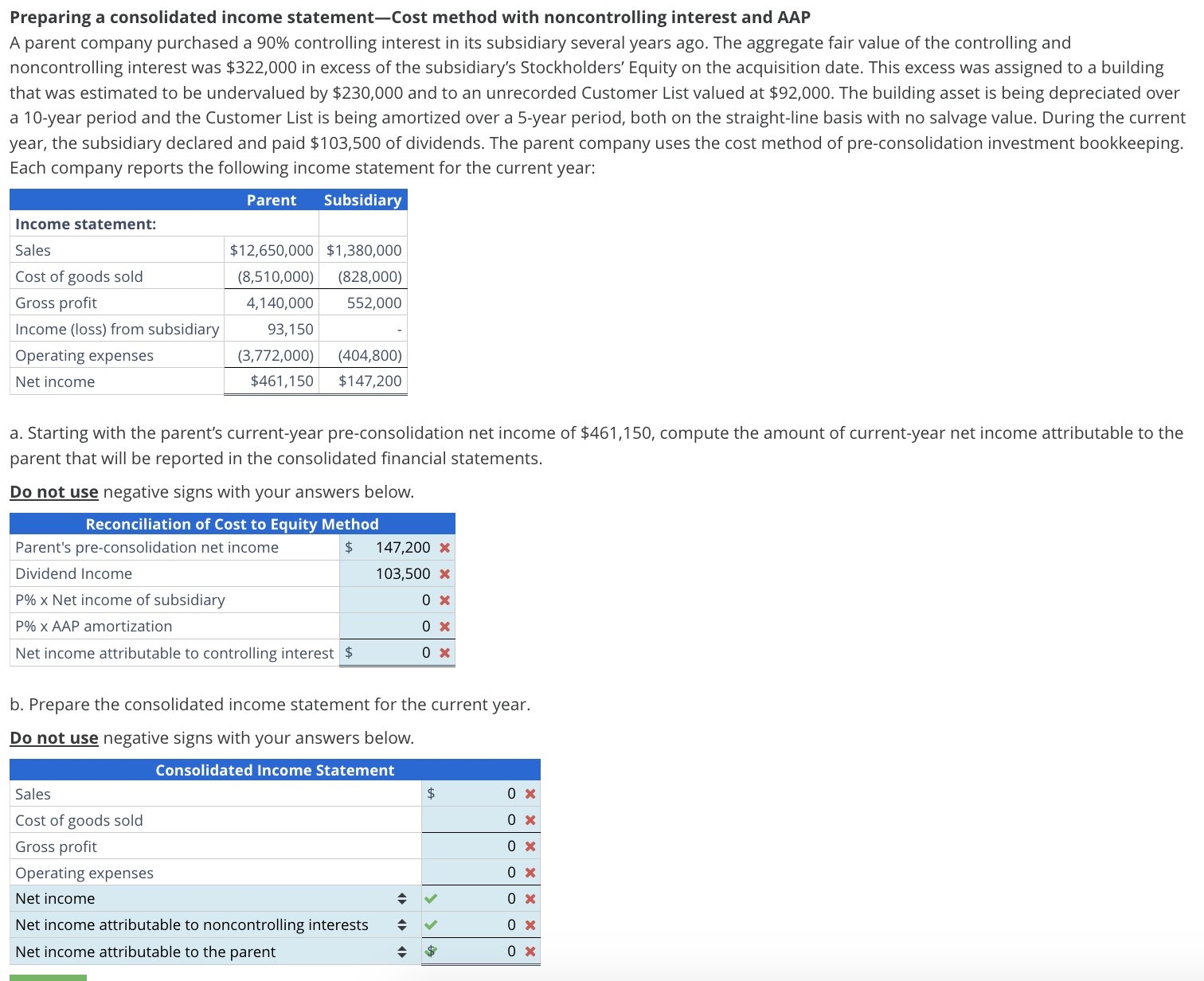

Preparing a consolidated income statement-Cost method with noncontrolling interest and AAP A parent company purchased a 90% controlling interest in its subsidiary several years ago. The aggregate fair value of the controlling and noncontrolling interest was $322,000 in excess of the subsidiary's Stockholders' Equity on the acquisition date. This excess was assigned to a building that was estimated to be undervalued by $230,000 and to an unrecorded Customer List valued at $92,000. The building asset is being depreciated over a 10-year period and the Customer List is being amortized over a 5-year period, both on the straight-line basis with no salvage value. During the current year, the subsidiary declared and paid $103,500 of dividends. The parent company uses the cost method of pre-consolidation investment bookkeeping. Each company reports the following income statement for the current year: a. Starting with the parent's current-year pre-consolidation net income of $461,150, compute the amount of current-year net income attributable to the parent that will be reported in the consolidated financial statements. Do not use negative signs with your answers below. b. Prepare the consolidated income statement for the current year. Do not use negative signs with your answers below

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts