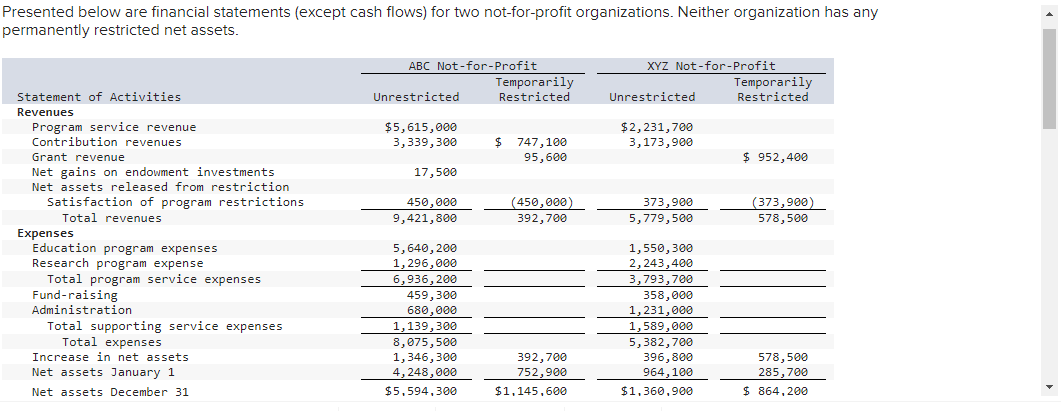

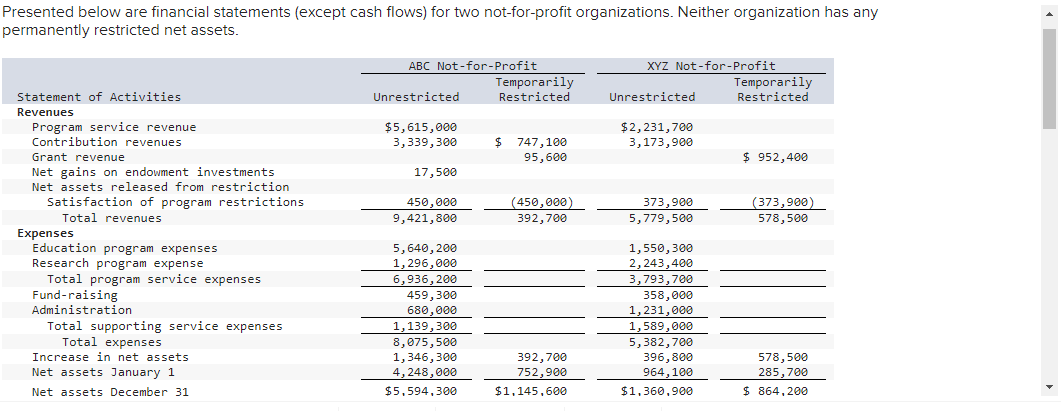

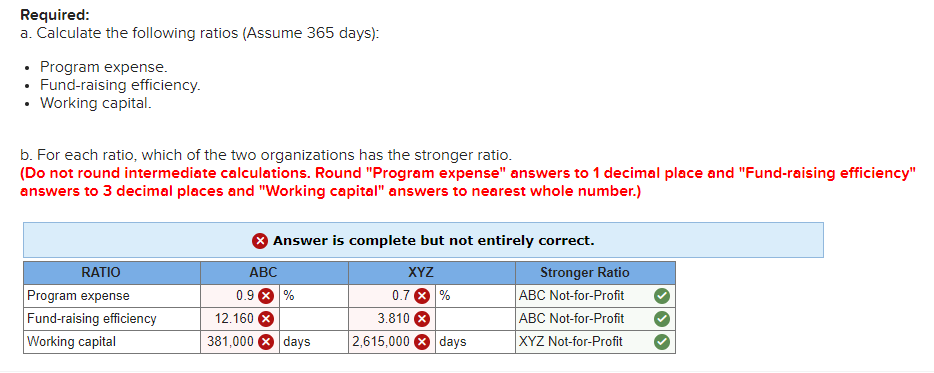

Question: Presented below are financial statements (except cash flows) for two not-for-profit organizations. Neither organization has any permanently restricted net assets. ABC Not-for-Profit Temporarily Unrestricted Restricted

Presented below are financial statements (except cash flows) for two not-for-profit organizations. Neither organization has any permanently restricted net assets. ABC Not-for-Profit Temporarily Unrestricted Restricted XYZ Not-for-Profit Temporarily Unrestricted Restricted $5,615,000 3,339,300 $ 747,100 95,600 $2,231,700 3,173,900 $ 952,400 17,500 450,000 9,421,800 (450,000) 392,700 373,900 5,779,500 (373,900) 578,500 Statement of Activities Revenues Program service revenue Contribution revenues Grant revenue Net gains on endowment investments Net assets released from restriction Satisfaction of program restrictions Total revenues Expenses Education program expenses Research program expense Total program service expenses Fund-raising Administration Total supporting service expenses Total expenses Increase in net assets Net assets January 1 Net assets December 31 5,640,200 1,296,000 6,936,200 459,300 680,000 1,139,300 8,075,500 1,346,300 4,248,000 $5,594,300 1,550,300 2,243,400 3,793,700 358,000 1,231,000 1,589,000 5,382,700 396,800 964,100 $1,360,900 392,700 752,900 $1,145,600 578,500 285,700 $ 864,200 Presented below are financial statements (except cash flows) for two not-for-profit organizations. Neither organization has any permanently restricted net assets. ABC Not-for-Profit Temporarily Unrestricted Restricted XYZ Not-for-Profit Temporarily Unrestricted Restricted $5,615,000 3,339,300 $ 747,100 95,600 $2,231,700 3,173,900 $ 952,400 17,500 450,000 9,421,800 (450,000) 392,700 373,900 5,779,500 (373,900) 578,500 Statement of Activities Revenues Program service revenue Contribution revenues Grant revenue Net gains on endowment investments Net assets released from restriction Satisfaction of program restrictions Total revenues Expenses Education program expenses Research program expense Total program service expenses Fund-raising Administration Total supporting service expenses Total expenses Increase in net assets Net assets January 1 Net assets December 31 5,640,200 1,296,000 6,936,200 459,300 680,000 1,139,300 8,075,500 1,346,300 4,248,000 $5,594,300 1,550,300 2,243,400 3,793,700 358,000 1,231,000 1,589,000 5,382,700 396,800 964,100 $1,360,900 392,700 752,900 $1,145,600 578,500 285,700 $ 864,200 Required: a. Calculate the following ratios (Assume 365 days): Program expense. Fund-raising efficiency. Working capital. b. For each ratio, which of the two organizations has the stronger ratio. (Do not round intermediate calculations. Round "Program expense" answers to 1 decimal place and "Fund-raising efficiency" answers to 3 decimal places and "Working capital" answers to nearest whole number.) Answer is complete but not entirely correct. RATIO Program expense Fund-raising efficiency Working capital ABC 0.9 % % 12.160 X 381,000 days XYZ 0.7 % 3.810 2,615,000 days Stronger Ratio ABC Not-for-Profit ABC Not-for-Profit XYZ Not-for-Profit Presented below are financial statements (except cash flows) for two not-for-profit organizations. Neither organization has any permanently restricted net assets. ABC Not-for-Profit Temporarily Unrestricted Restricted XYZ Not-for-Profit Temporarily Unrestricted Restricted $5,615,000 3,339,300 $ 747,100 95,600 $2,231,700 3,173,900 $ 952,400 17,500 450,000 9,421,800 (450,000) 392,700 373,900 5,779,500 (373,900) 578,500 Statement of Activities Revenues Program service revenue Contribution revenues Grant revenue Net gains on endowment investments Net assets released from restriction Satisfaction of program restrictions Total revenues Expenses Education program expenses Research program expense Total program service expenses Fund-raising Administration Total supporting service expenses Total expenses Increase in net assets Net assets January 1 Net assets December 31 5,640,200 1,296,000 6,936,200 459,300 680,000 1,139,300 8,075,500 1,346,300 4,248,000 $5,594,300 1,550,300 2,243,400 3,793,700 358,000 1,231,000 1,589,000 5,382,700 396,800 964,100 $1,360,900 392,700 752,900 $1,145,600 578,500 285,700 $ 864,200 Presented below are financial statements (except cash flows) for two not-for-profit organizations. Neither organization has any permanently restricted net assets. ABC Not-for-Profit Temporarily Unrestricted Restricted XYZ Not-for-Profit Temporarily Unrestricted Restricted $5,615,000 3,339,300 $ 747,100 95,600 $2,231,700 3,173,900 $ 952,400 17,500 450,000 9,421,800 (450,000) 392,700 373,900 5,779,500 (373,900) 578,500 Statement of Activities Revenues Program service revenue Contribution revenues Grant revenue Net gains on endowment investments Net assets released from restriction Satisfaction of program restrictions Total revenues Expenses Education program expenses Research program expense Total program service expenses Fund-raising Administration Total supporting service expenses Total expenses Increase in net assets Net assets January 1 Net assets December 31 5,640,200 1,296,000 6,936,200 459,300 680,000 1,139,300 8,075,500 1,346,300 4,248,000 $5,594,300 1,550,300 2,243,400 3,793,700 358,000 1,231,000 1,589,000 5,382,700 396,800 964,100 $1,360,900 392,700 752,900 $1,145,600 578,500 285,700 $ 864,200 Required: a. Calculate the following ratios (Assume 365 days): Program expense. Fund-raising efficiency. Working capital. b. For each ratio, which of the two organizations has the stronger ratio. (Do not round intermediate calculations. Round "Program expense" answers to 1 decimal place and "Fund-raising efficiency" answers to 3 decimal places and "Working capital" answers to nearest whole number.) Answer is complete but not entirely correct. RATIO Program expense Fund-raising efficiency Working capital ABC 0.9 % % 12.160 X 381,000 days XYZ 0.7 % 3.810 2,615,000 days Stronger Ratio ABC Not-for-Profit ABC Not-for-Profit XYZ Not-for-Profit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts