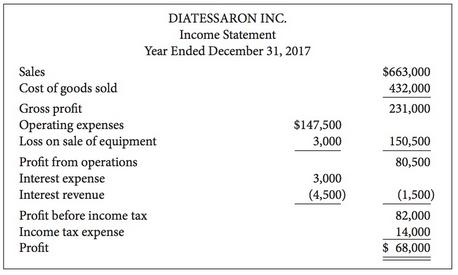

Question: Presented below is the comparative balance sheet for Diatessaron Inc., a private company reporting under ASPE, at December 31, 2017 and 2016: Additional information: 1.

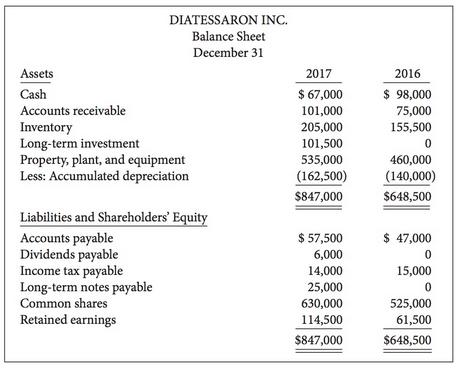

Presented below is the comparative balance sheet for Diatessaron Inc., a private company reporting under ASPE, at December 31, 2017 and 2016:

Additional information:

1. Cash dividends of $15,000 were declared.

2. A long-term investment was acquired for cash at a cost of $101,500.

3. Depreciation expense is included in the operating expenses.

4. The company issued 10,500 common shares for cash on March 2, 2017. The fair value of the shares was $10 per share. The proceeds were used to purchase additional equipment.

5. Equipment that originally cost $30,000 was sold during the year for cash. The equipment had a carrying value of $9,000 at the time of sale.

6. The company issued a note payable for $28,000 and repaid $3,000 by year end.

Instructions

Prepare a cash flow statement for the year using the indirect method.

TAKING IT FURTHER

Is it necessary to show both the proceeds from issuing a new note payable and the partial repayment of notes payable? Or is it sufficient to simply show the net increase or decrease in notes payable, as is done with accounts payable? Explain.

SOLUTION

DIATESSARON INC.

Cash Flow Statement – Indirect Method

Year Ended December 31, 2017

Operating activities

Profit ........................................................................................... $68,000

Adjustments to reconcile profit

to net cash provided by operating activities:

Depreciation expense..................................................... $43,500 (1)

Loss on sale of equipment.............................................. 3,000

Increase in accounts receivable...................................... (26,000)

Increase in inventory...................................................... (49,500)

Increase in accounts payable.......................................... 10,500

Decrease in income tax payable..................................... (1,000) (19,500)

Net cash provided by operating activities...................................... 48,500

Investing activities

Acquisition of long-term investment.................................. (101,500)

Purchase of equipment........................................................ (105,000)

Sale of equipment................................................................. 6,000 (2)

Net cash used by investing activities.................................................... (200,500)

Financing activities

Issue of note payable............................................................ 28,000

Issuance of common shares.................................................. 105,000

Payment of dividends ($15,000 − $6,000).......................... (9,000)

Repayment of note payable.................................................. (3,000)

Net cash provided by financing activities............................................ 121,000

Net decrease in cash......................................................................................... (31,000)

Cash, January 1................................................................................................. 98,000

Cash, December 31........................................................................................... $67,000

Calculations:

(1) Depreciation expense

Accumulated depreciation, end of year................................................... $162,500

Plus: Accumulated depreciation of equipment

sold ($30,000 − $9,000).......................................................... 21,000

Accumulated depreciation, beg. of year................................... (140,000)

Depreciation expense............................................................................... $ 43,500

(2) Cash from sale of equipment

Carrying amount of equipment................................................................ $9,000

Less: Loss on sale............................................................................... (3,000)

Cash received........................................................................................... $6,000

Taking It Further:

Both the proceeds and the repayment should be shown separately. Information in financial statements is usually condensed and regrouped so that proceeds from issuing a note and repayments do not necessarily relate to the same debt instrument. Showing both separately allows the user to tie the amounts to note disclosure about the various debt instruments.

Assets Cash Accounts receivable Inventory Long-term investment DIATESSARON INC. Balance Sheet December 31 Property, plant, and equipment Less: Accumulated depreciation Liabilities and Shareholders' Equity Accounts payable Dividends payable Income tax payable Long-term notes payable Common shares Retained earnings 2017 $ 67,000 101,000 205,000 101,500 535,000 (162,500) $847,000 $ 57,500 6,000 14,000 25,000 630,000 114,500 $847,000 2016 $ 98,000 75,000 155,500 0 460,000 (140,000) $648,500 $ 47,000 0 15,000 0 525,000 61,500 $648,500

Step by Step Solution

3.53 Rating (160 Votes )

There are 3 Steps involved in it

Question Answer Diatessaron Inc Cash Flow statement indirect Method For the year ended December 31 A... View full answer

Get step-by-step solutions from verified subject matter experts