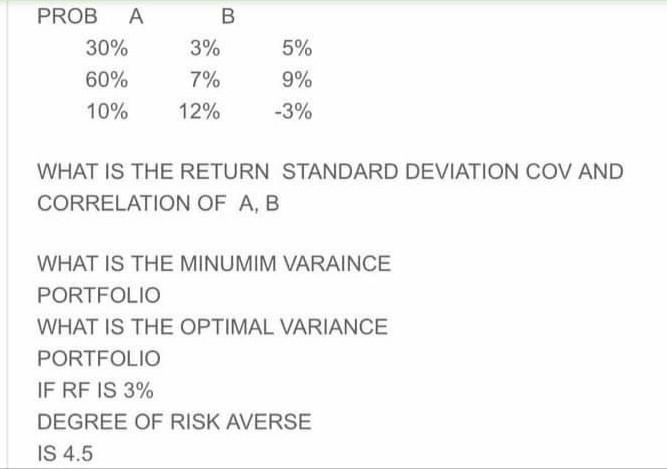

Question: PROB A B 30% 3% 5% 60% 7% 9% 10% 12% -3% WHAT IS THE RETURN STANDARD DEVIATION COV AND CORRELATION OF A, B WHAT

PROB A B 30% 3% 5% 60% 7% 9% 10% 12% -3% WHAT IS THE RETURN STANDARD DEVIATION COV AND CORRELATION OF A, B WHAT IS THE MINUMIM VARAINCE PORTFOLIO WHAT IS THE OPTIMAL VARIANCE PORTFOLIO IF RF IS 3% DEGREE OF RISK AVERSE IS 4.5

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock