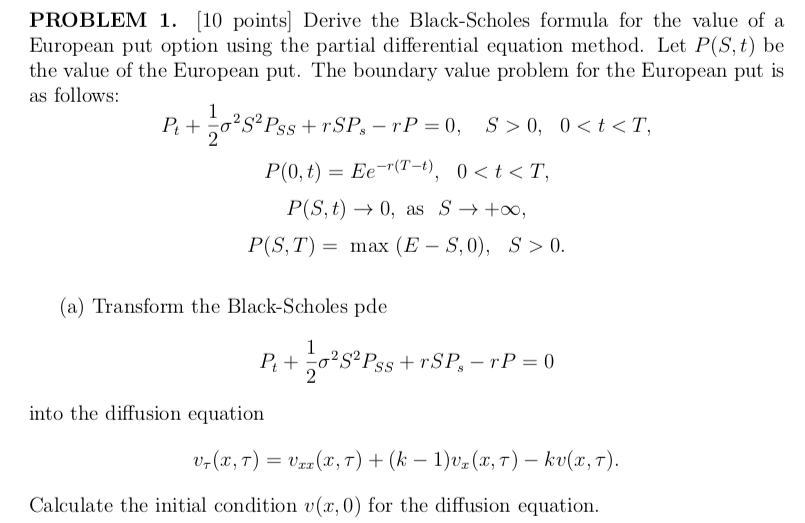

Question: PROBLEM 1. [10 points Derive the Black-Scholes formula for the value of a European put option using the partial differential equation method. Let P(S, t)

PROBLEM 1. [10 points Derive the Black-Scholes formula for the value of a European put option using the partial differential equation method. Let P(S, t) be the value of the European put. The boundary value problem for the European put is as follows: P(0, t) Ee-T-), 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts