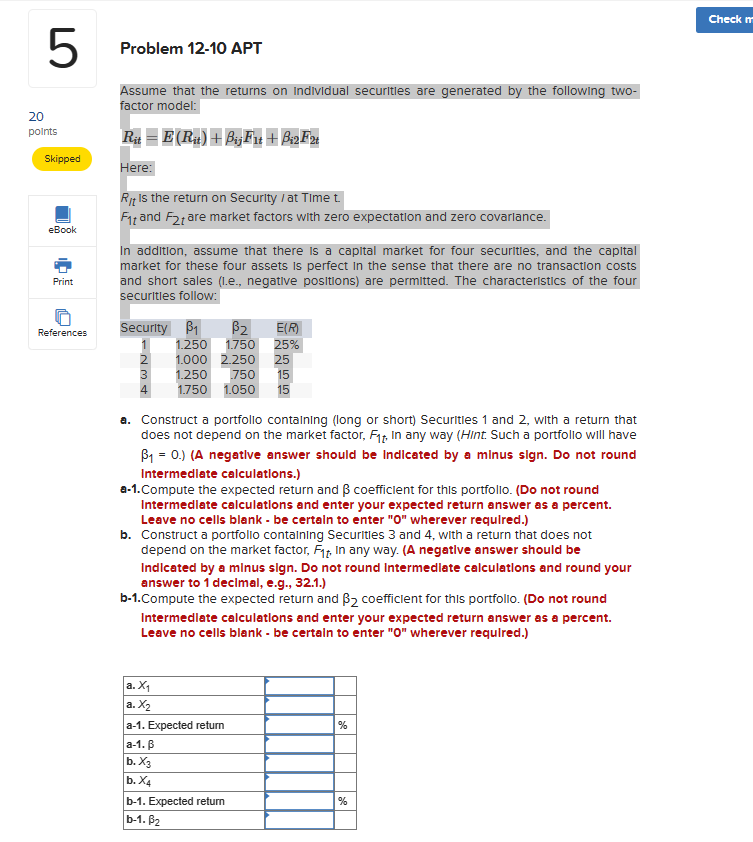

Question: Problem 1 2 - 1 0 APT Assume that the returns on Individual securitles are generated by the following two - factor model: R ?

Problem APT

Assume that the returns on Individual securitles are generated by the following two

factor model:

Is the return on Security at Time

and are market factors with zero expectation and zero covarlance.

In addition, assume that there is a capital market for four securities and the capital

market for these four assets is perfect in the sense that there are no transaction costs

and short sales le negative positions are permitted. The characteristics of the four

securities follow:

a Construct a portfolio containing long or short Securities and with a return that

does not depend on the market factor, In any way Hint Such a portfolio will have

A negatlve answer should be Indicated by a minus sign. Do not round

Intermedlate calculations.

aCompute the expected return and coefficient for this portfolio. Do not round

Intermedlate calculations and enter your expected return answer as a percent.

Leave no cells blank be certain to enter wherever required.

b Construct a portfolio containing Securitles and with a return that does not

depend on the market factor, in any way. A negatlve answer should be

Indlcated by a minus sign. Do not round Intermedlate calculations and round your

answer to decimal, eg

bCompute the expected return and coefficlent for this portfollo. Do not round

Intermedlate calculations and enter your expected return answer as a percent.

Leave no cells blank be certaln to enter wherever requlred.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock