Question: Problem 1 (25 points) Suppose that risk-free zero interest rates with continuous compounding are as follows: Maturity ( years) Rate (% per annum) 3.0 5.0

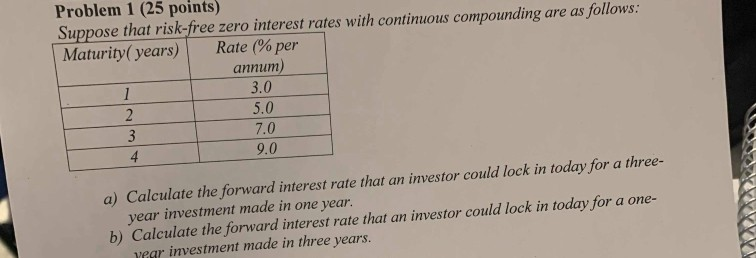

Problem 1 (25 points) Suppose that risk-free zero interest rates with continuous compounding are as follows: Maturity ( years) Rate (% per annum) 3.0 5.0 7.0 9.0 4 a) Calculate the forward interest rate that an investor could lock in today for a three- year investment made in one year. b) Calculate the forward interest rate that an investor could lock in today for a one- wear investment made in three years

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock