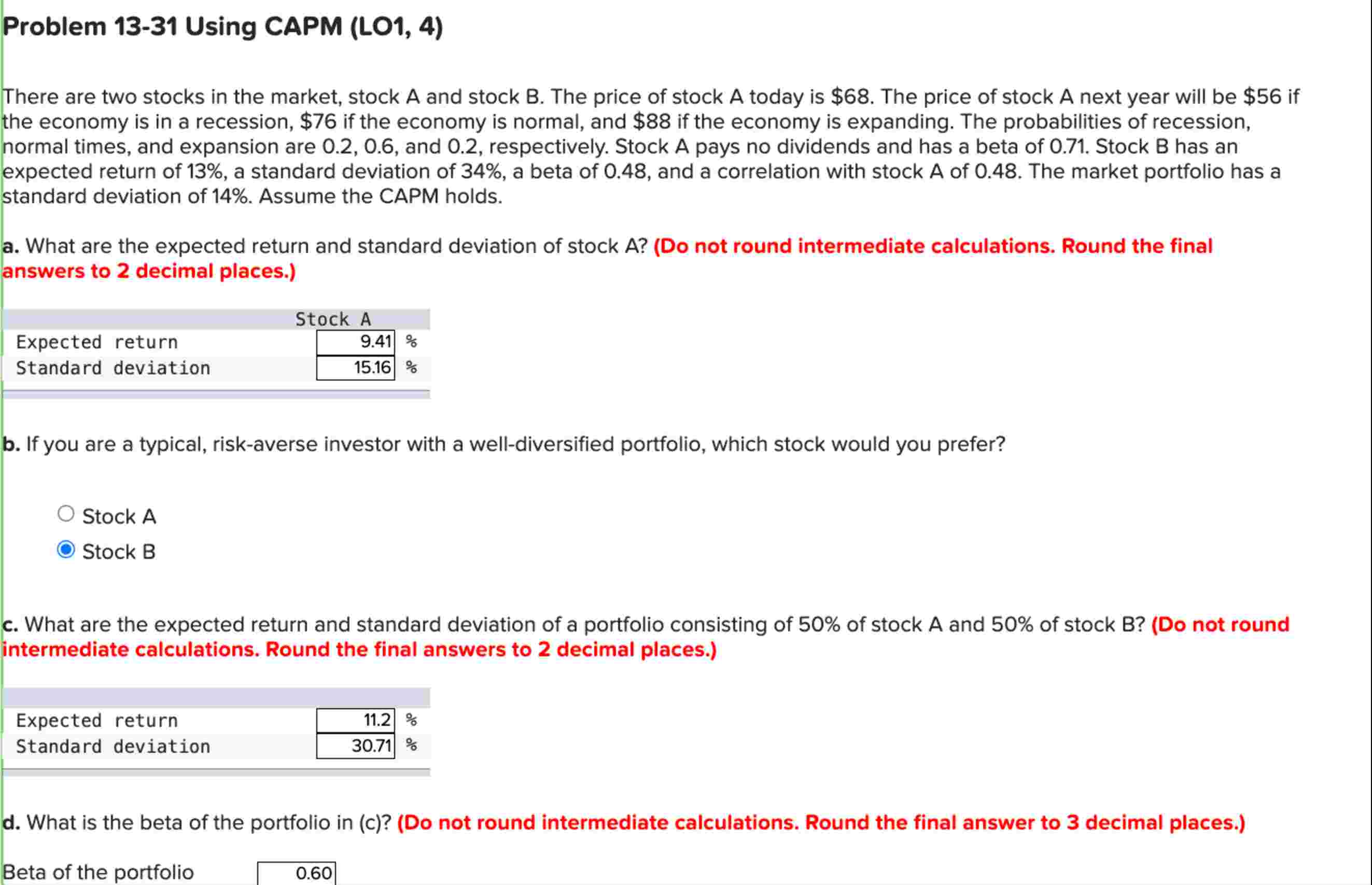

Question: Problem 1 3 - 3 1 Using CAPM ( ( L O 1 , 4 ) ) There are two stocks in the

Problem Using CAPM L O There are two stocks in the market, stock A and stock B The price of stock A today is $ The price of stock A next year will be $ if the economy is in a recession, $ if the economy is normal, and $ if the economy is expanding. The probabilities of recession, normal times, and expansion are and respectively. Stock A pays no dividends and has a beta of Stock B has an expected return of a standard deviation of a beta of and a correlation with stock A of The market portfolio has a standard deviation of Assume the CAPM holds. a What are the expected return and standard deviation of stock ADo not round intermediate calculations. Round the final answers to decimal places. b If you are a typical, riskaverse investor with a welldiversified portfolio, which stock would you prefer? Stock A Stock B c What are the expected return and standard deviation of a portfolio consisting of of stock A and of stock BDo not round intermediate calculations. Round the final answers to mathbf decimal places. d What is the beta of the portfolio in cDo not round intermediate calculations. Round the final answer to decimal places. Beta of the portfolio

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock