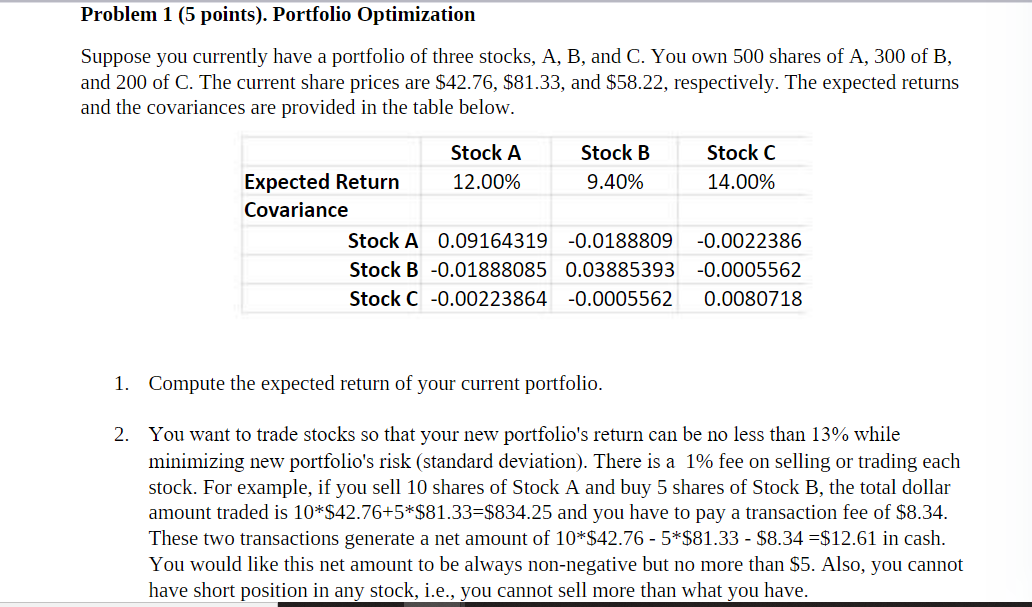

Question: Problem 1 (5 points). Portfolio Optimization Suppose you currently have a portfolio of three stocks, A, B, and C. You own 500 shares of A,

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts