Question: Problem 1. Consider a market with three assets and three states of the world. At time t=0 we have that 8= 1,57 = 3,86 and

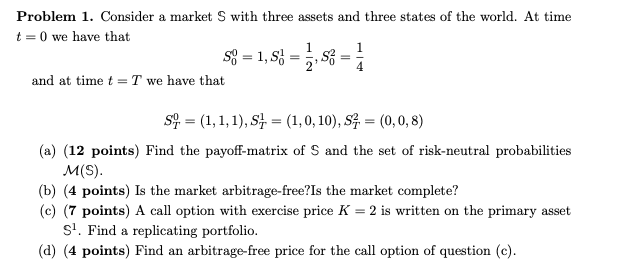

Problem 1. Consider a market with three assets and three states of the world. At time t=0 we have that 8= 1,57 = 3,86 and at time t = T we have that 4 Se = (1,1,1), S1 = (1,0,10), S = (0,0,8) (a) (12 points) Find the payoff-matrix of S and the set of risk-neutral probabilities M(S). (b) (4 points) Is the market arbitrage-free?Is the market complete? (c) (7 points) A call option with exercise price K = 2 is written on the primary asset S! Find a replicating portfolio. (d) (4 points) Find an arbitrage-free price for the call option of question (c). Problem 1. Consider a market with three assets and three states of the world. At time t=0 we have that 8= 1,57 = 3,86 and at time t = T we have that 4 Se = (1,1,1), S1 = (1,0,10), S = (0,0,8) (a) (12 points) Find the payoff-matrix of S and the set of risk-neutral probabilities M(S). (b) (4 points) Is the market arbitrage-free?Is the market complete? (c) (7 points) A call option with exercise price K = 2 is written on the primary asset S! Find a replicating portfolio. (d) (4 points) Find an arbitrage-free price for the call option of question (c)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts