Question: Problem 1. Consider an asset whose price path is as follows: Time 1 $p1 $p1 $p2 $p2 Time 2 $21 $11 $10 $5 Risk-neutral probability

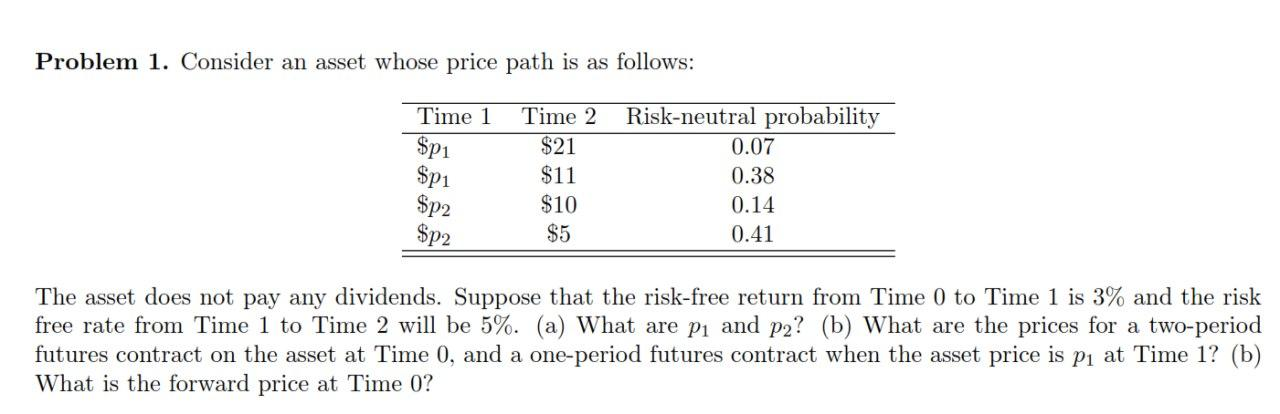

Problem 1. Consider an asset whose price path is as follows: Time 1 $p1 $p1 $p2 $p2 Time 2 $21 $11 $10 $5 Risk-neutral probability 0.07 0.38 0.14 0.41 The asset does not pay any dividends. Suppose that the risk-free return from Time 0 to Time 1 is 3% and the risk free rate from Time 1 to Time 2 will be 5%. (a) What are p and p2? (b) What are the prices for a two-period futures contract on the asset at Time 0, and a one-period futures contract when the asset price is P at Time 1? (b) What is the forward price at Time 0? Problem 1. Consider an asset whose price path is as follows: Time 1 $p1 $p1 $p2 $p2 Time 2 $21 $11 $10 $5 Risk-neutral probability 0.07 0.38 0.14 0.41 The asset does not pay any dividends. Suppose that the risk-free return from Time 0 to Time 1 is 3% and the risk free rate from Time 1 to Time 2 will be 5%. (a) What are p and p2? (b) What are the prices for a two-period futures contract on the asset at Time 0, and a one-period futures contract when the asset price is P at Time 1? (b) What is the forward price at Time 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts