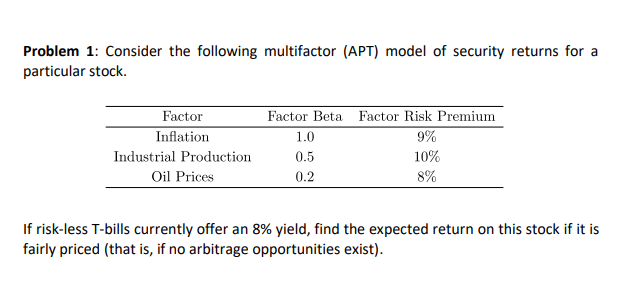

Question: Problem 1: Consider the following multifactor (APT) model of security returns for a particular stock Factor Inflation Industrial Production Oil Prices Factor Beta 1.0 0.5

Problem 1: Consider the following multifactor (APT) model of security returns for a particular stock Factor Inflation Industrial Production Oil Prices Factor Beta 1.0 0.5 0.2 Factor Risk Premium 9% 10% 8% If riskless T-bills currently offer an 8% yield, find the expected return on this stock if it is fairly priced (that is, if no arbitrage opportunities exist)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock