Question: Problem 1 discount zero forward par Bond Cash Flow curve curve curve curve Overnight Cash Inputs 0 0.70% 1 1.20% 2 1.60% 3 1.90% 4

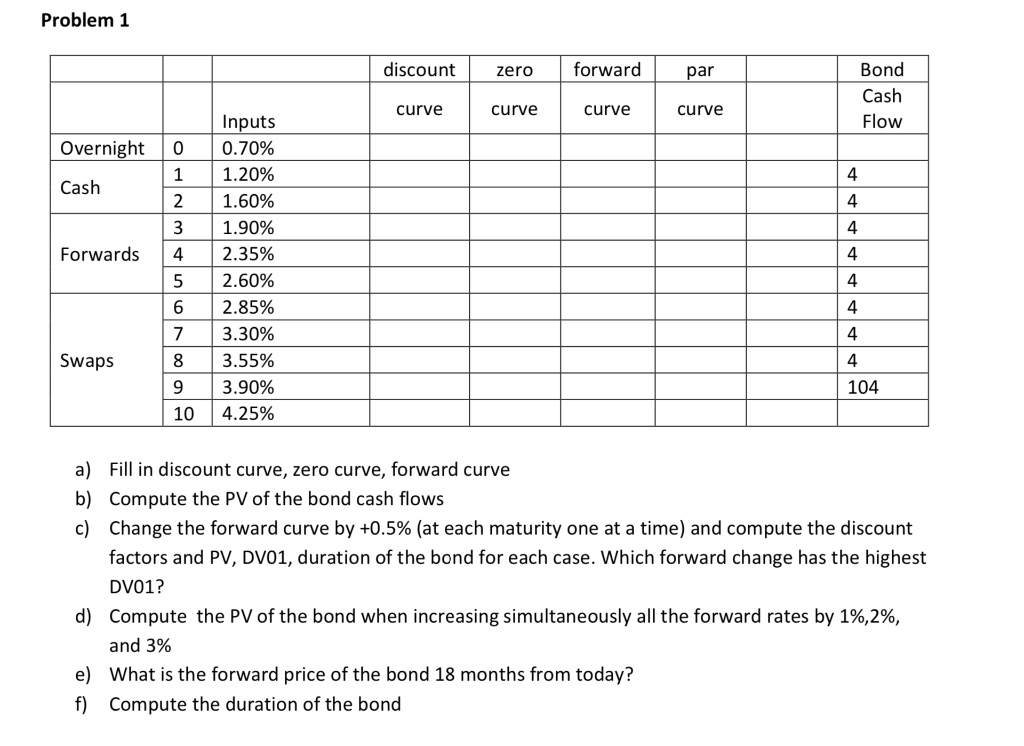

Problem 1 discount zero forward par Bond Cash Flow curve curve curve curve Overnight Cash Inputs 0 0.70% 1 1.20% 2 1.60% 3 1.90% 4 2.35% 5 2.60% 6 2.85% 17 3.30% 8 3.55% 193.90% 10 4.25% 4 4 4 4 4 4 Forwards Swaps 104 a) Fill in discount curve, zero curve, forward curve b) Compute the PV of the bond cash flows c) Change the forward curve by +0.5% (at each maturity one at a time) and compute the discount factors and PV, DV01, duration of the bond for each case. Which forward change has the highest DVO1? d) Compute the PV of the bond when increasing simultaneously all the forward rates by 1%,2%, and 3% e) What is the forward price of the bond 18 months from today? f) Compute the duration of the bond Problem 1 discount zero forward par Bond Cash Flow curve curve curve curve Overnight Cash Inputs 0 0.70% 1 1.20% 2 1.60% 3 1.90% 4 2.35% 5 2.60% 6 2.85% 17 3.30% 8 3.55% 193.90% 10 4.25% 4 4 4 4 4 4 Forwards Swaps 104 a) Fill in discount curve, zero curve, forward curve b) Compute the PV of the bond cash flows c) Change the forward curve by +0.5% (at each maturity one at a time) and compute the discount factors and PV, DV01, duration of the bond for each case. Which forward change has the highest DVO1? d) Compute the PV of the bond when increasing simultaneously all the forward rates by 1%,2%, and 3% e) What is the forward price of the bond 18 months from today? f) Compute the duration of the bond

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts