Question: Problem 1 Let P ( YTM ) denote the bond pricing equation for perpetual, zero - coupon, and coupon paying bonds as a function of

Problem

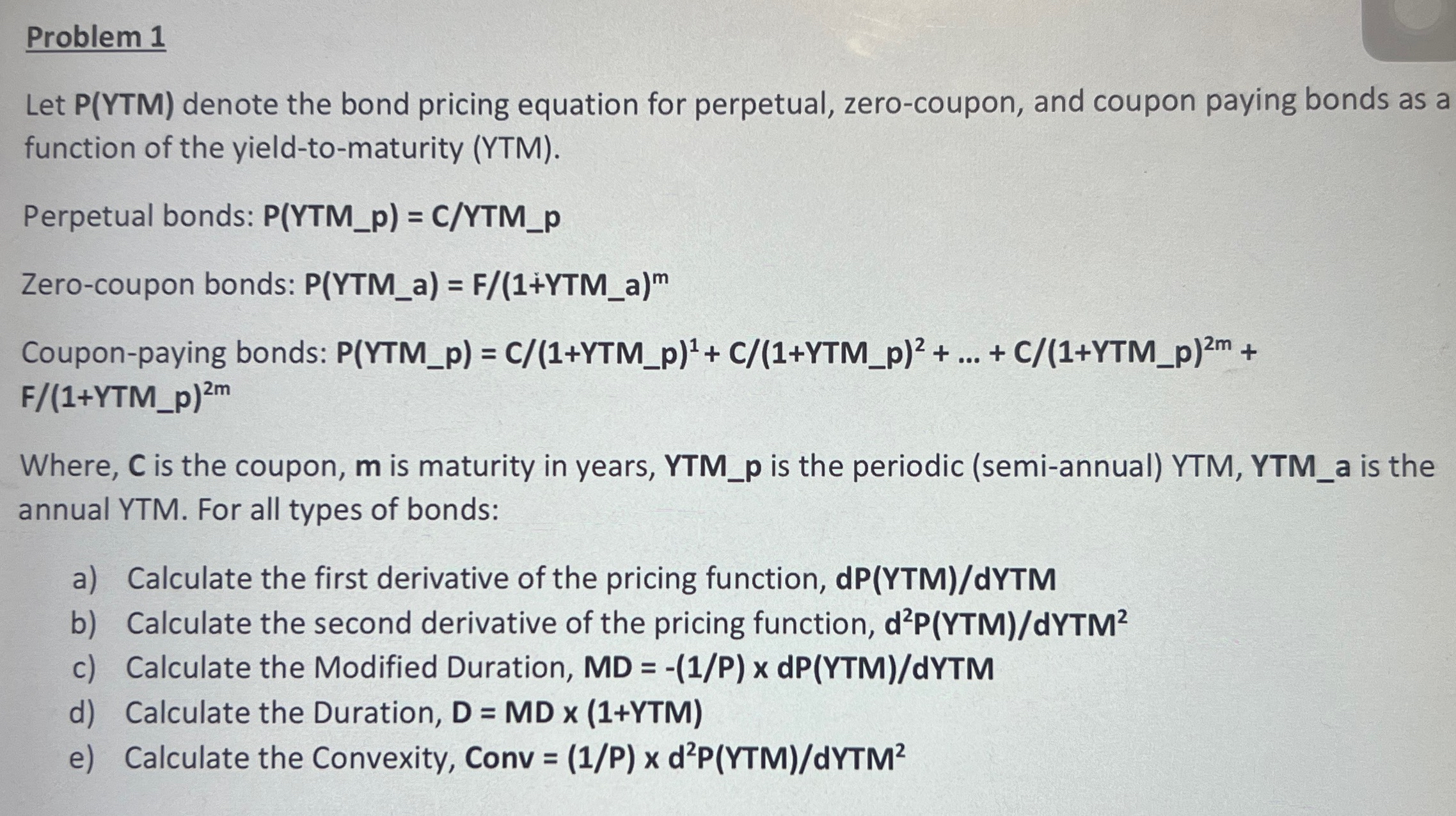

Let PYTM denote the bond pricing equation for perpetual, zerocoupon, and coupon paying bonds as a function of the yieldtomaturity YTM

Perpetual bonds: PYTMp CYTMp

Zerocoupon bonds: PYTMa FYTMa

Couponpaying bonds: dots FYTMp

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock