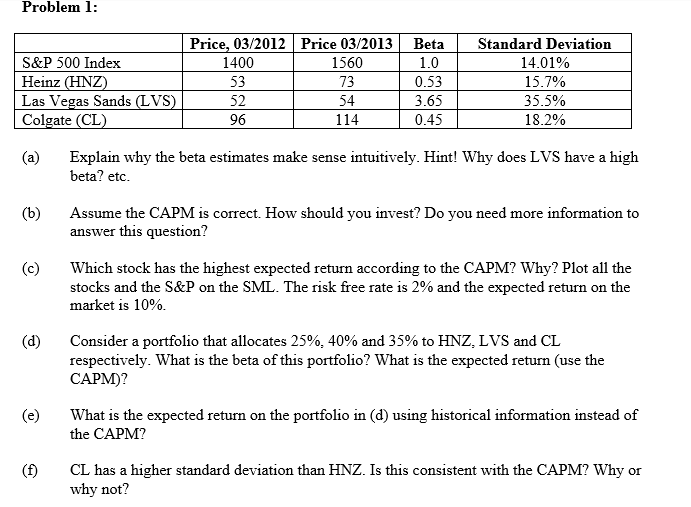

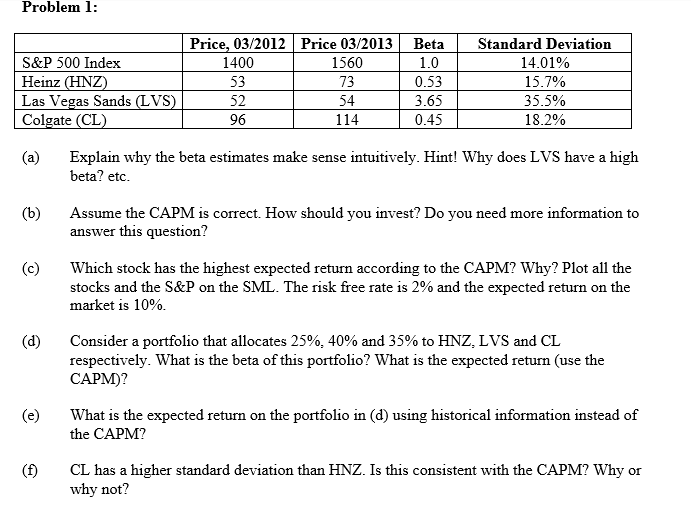

Question: Problem 1: Price, 03/2012 Price 03/2013 Beta Standard Deviation S&P 500 Index 1400 1560 1.0 14.01% Heinz (HNZ) 53 73 0.53 15.7% Las Vegas Sands

Problem 1: Price, 03/2012 Price 03/2013 Beta Standard Deviation S&P 500 Index 1400 1560 1.0 14.01% Heinz (HNZ) 53 73 0.53 15.7% Las Vegas Sands (LVS) 52 54 3.65 35.5% Colgate (CL) 96 114 0.45 18.2% (a) Explain why the beta estimates make sense intuitively. Hint! Why does LVS have a high beta? etc. (b) Assume the CAPM is correct. How should you invest? Do you need more information to answer this question? (c) Which stock has the highest expected return according to the CAPM? Why? Plot all the stocks and the S&P on the SML. The risk free rate is 2% and the expected return on the market is 10%. (d) Consider a portfolio that allocates 25%, 40% and 35% to HNZ, LVS and CL respectively. What is the beta of this portfolio? What is the expected return (use the CAPM)? (e) What is the expected return on the portfolio in (d) using historical information instead of the CAPM? (f) CL has a higher standard deviation than HNZ. Is this consistent with the CAPM? Why or why not

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts