Question: PROBLEM 1 PROBLEM 2 PROBLEM 3 How much should the company recognized as compensation expense for 2021? * (1 Point) In order to boost the

PROBLEM 1

PROBLEM 2

PROBLEM 3

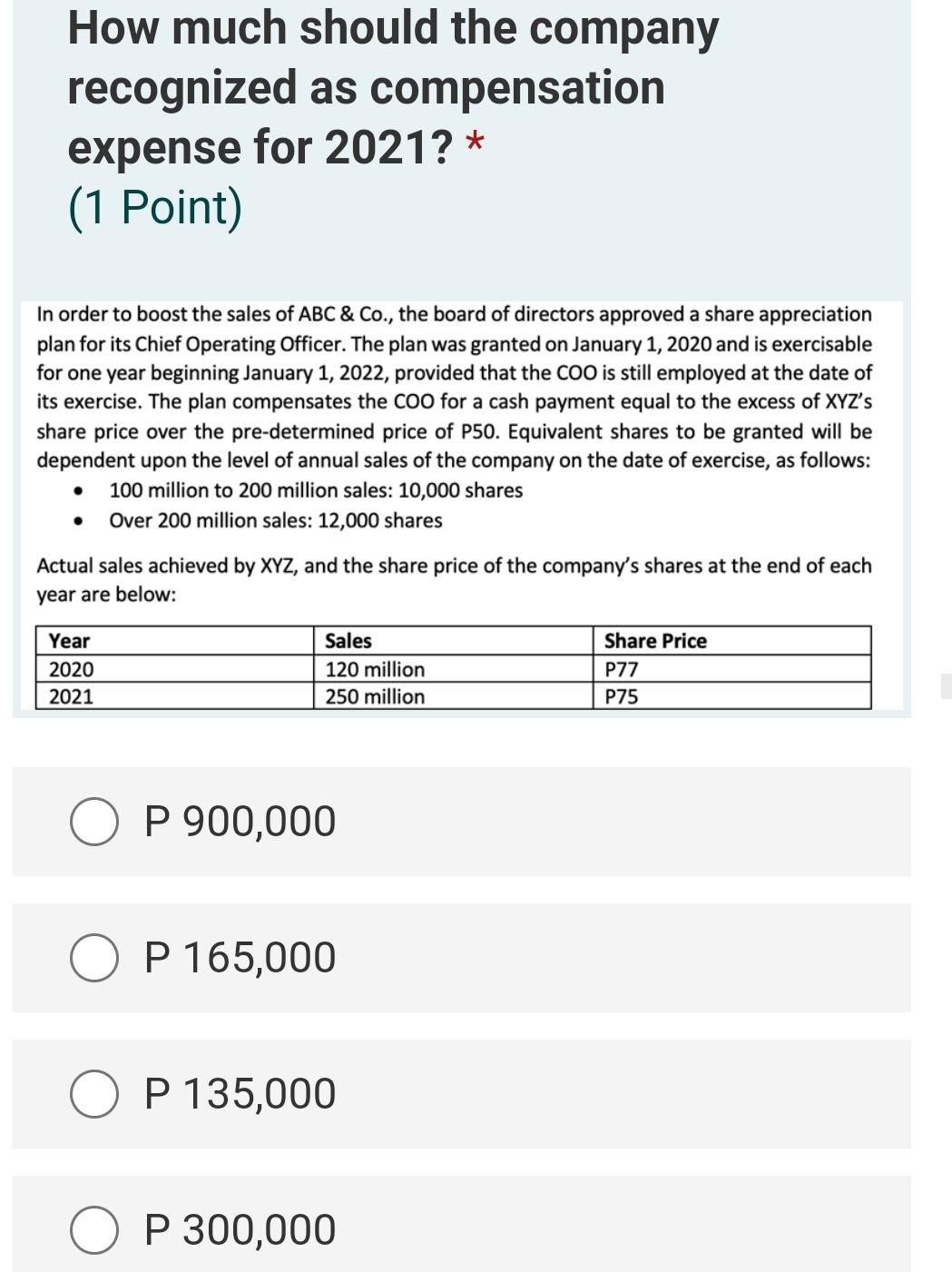

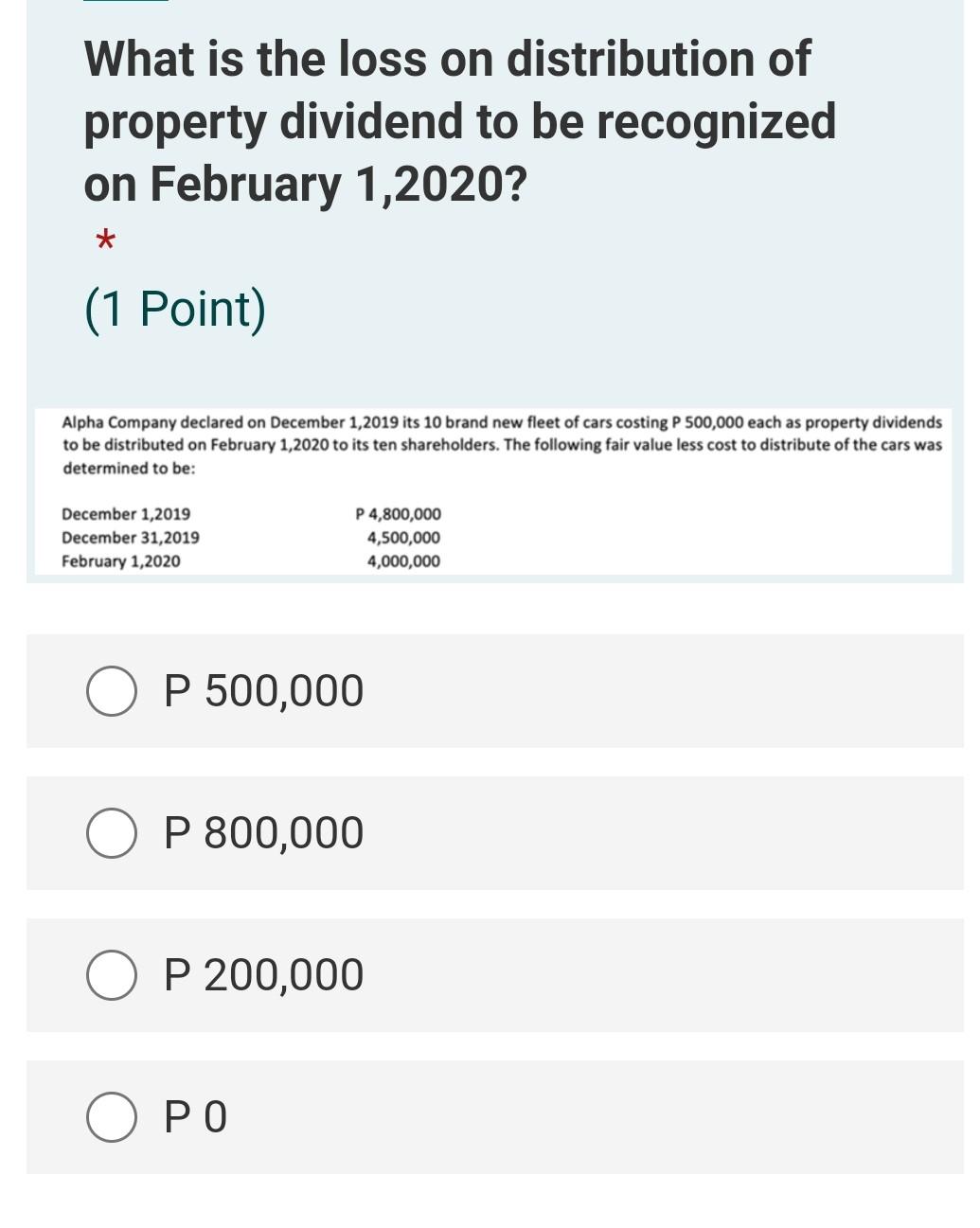

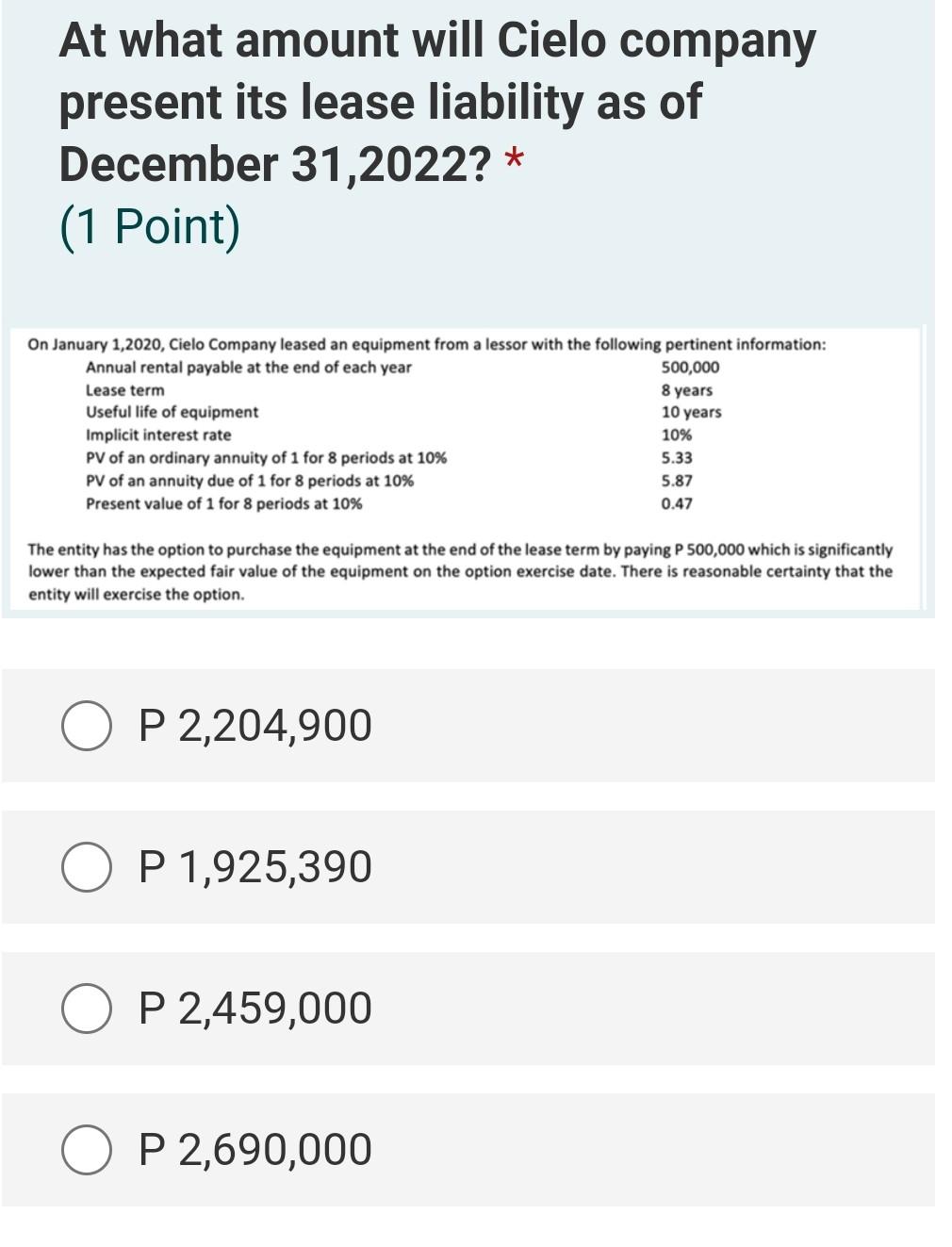

How much should the company recognized as compensation expense for 2021? * (1 Point) In order to boost the sales of ABC & Co., the board of directors approved a share appreciation plan for its Chief Operating Officer. The plan was granted on January 1, 2020 and is exercisable for one year beginning January 1, 2022, provided that the COO is still employed at the date of its exercise. The plan compensates the coo for a cash payment equal to the excess of XYZ's share price over the pre-determined price of P50. Equivalent shares to be granted will be dependent upon the level of annual sales of the company on the date of exercise, as follows: 100 million to 200 million sales: 10,000 shares Over 200 million sales: 12,000 shares Actual sales achieved by XYZ, and the share price of the company's shares at the end of each year are below: Year 2020 2021 Sales 120 million 250 million Share Price P77 P75 P 900,000 P 165,000 O P 135,000 P 300,000 What is the loss on distribution of property dividend to be recognized on February 1,2020? * (1 Point) Alpha Company declared on December 1,2019 its 10 brand new fleet of cars costing P 500,000 each as property dividends to be distributed on February 1,2020 to its ten shareholders. The following fair value less cost to distribute of the cars was determined to be: December 1,2019 December 31,2019 February 1, 2020 P 4,800,000 4,500,000 4,000,000 P 500,000 P 800,000 P 200,000 At what amount will Cielo company present its lease liability as of December 31,2022? * (1 Point) On January 1,2020, Cielo Company leased an equipment from a lessor with the following pertinent information: Annual rental payable at the end of each year 500,000 Lease term 8 years Useful life of equipment 10 years Implicit interest rate 10% PV of an ordinary annuity of 1 for 8 periods at 10% 5.33 PV of an annuity due of 1 for 8 periods at 10% 5.87 Present value of 1 for 8 periods at 10% 0.47 The entity has the option to purchase the equipment at the end of the lease term by paying P 500,000 which is significantly lower than the expected fair value of the equipment on the option exercise date. There is reasonable certainty that the entity will exercise the option. O P 2,204,900 P 1,925,390 O P 2,459,000 O P 2,690,000

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts