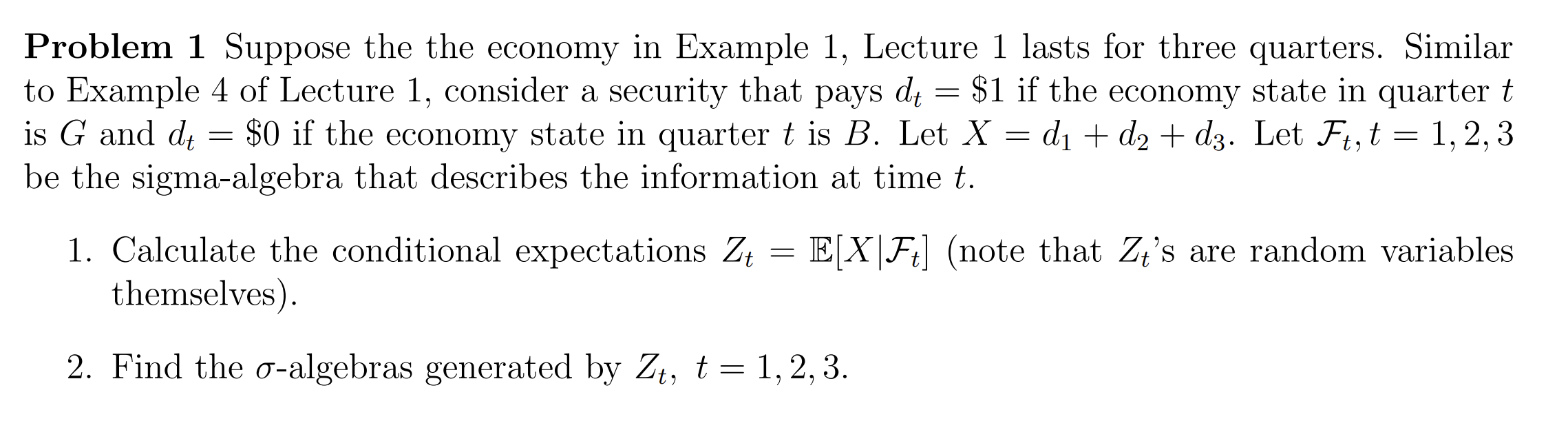

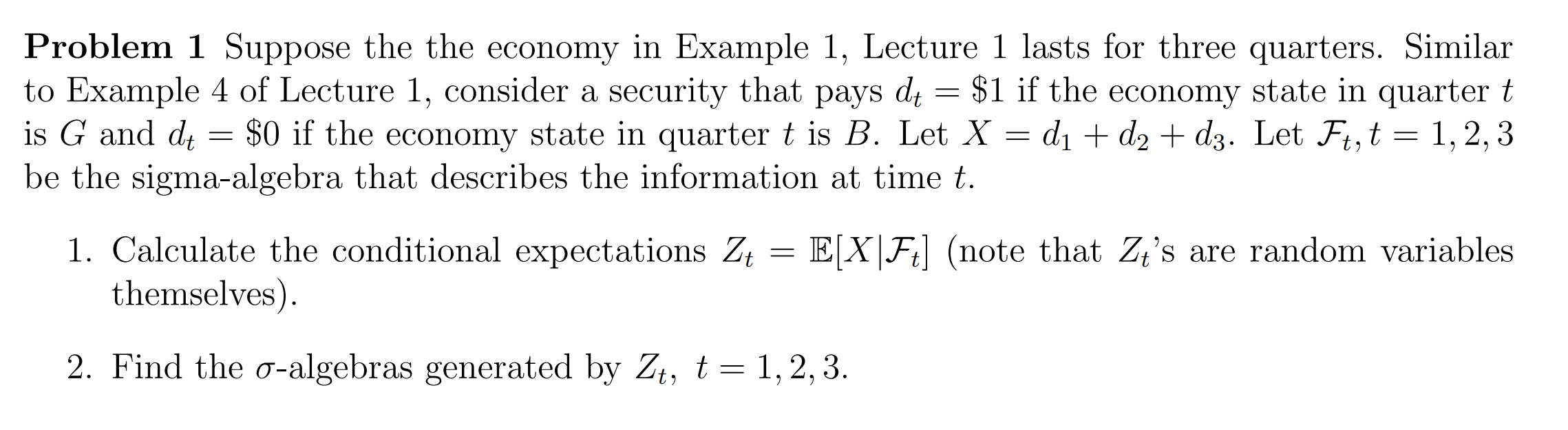

Question: Problem 1 Suppose the the economy in Example 1, Lecture 1 lasts for three quarters. Similar to Example 4 of Lecture 1, consider a security

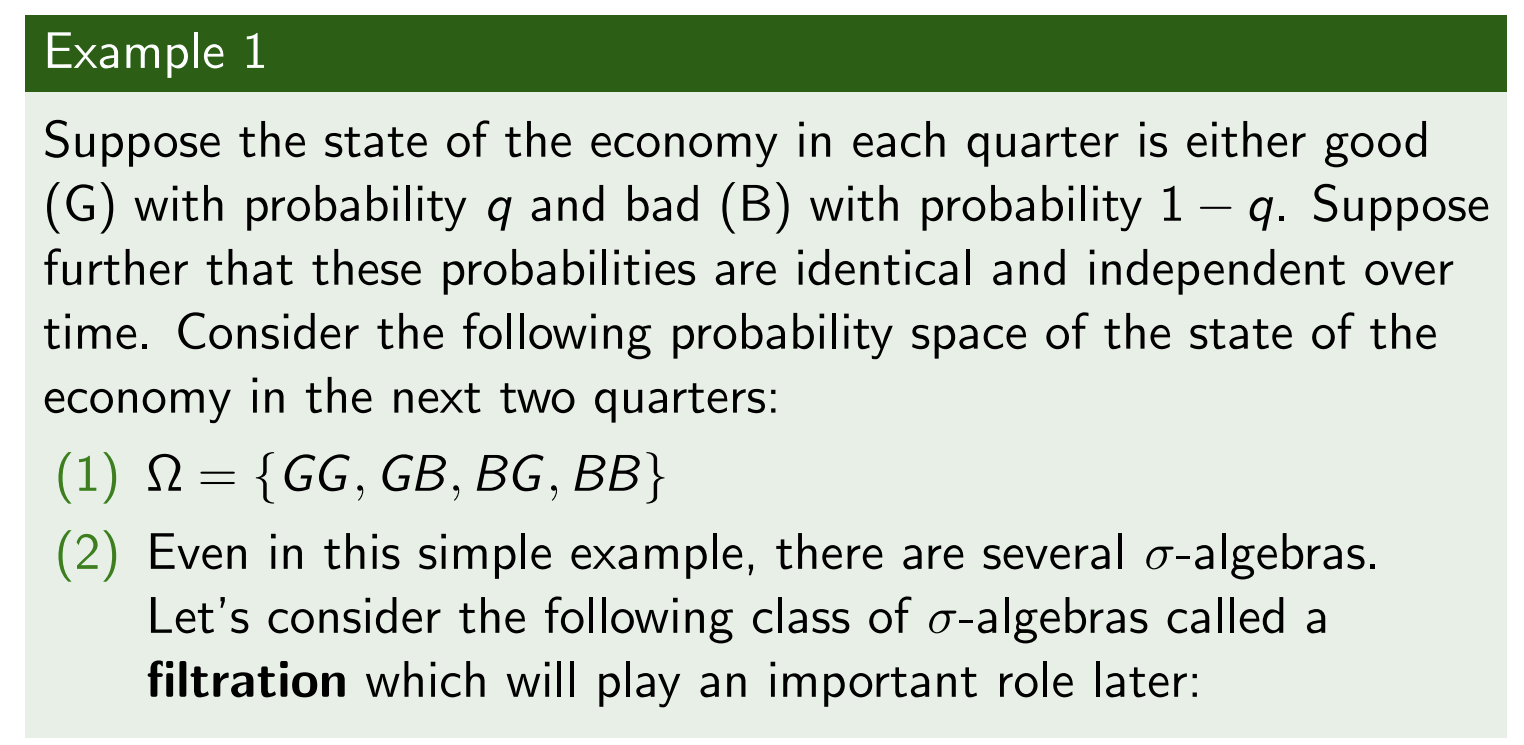

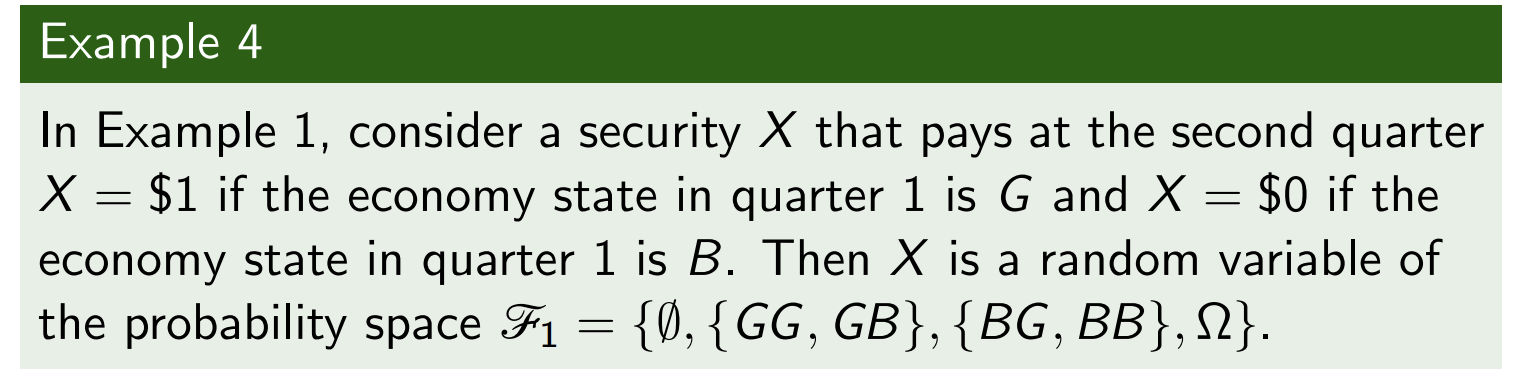

Problem 1 Suppose the the economy in Example 1, Lecture 1 lasts for three quarters. Similar to Example 4 of Lecture 1, consider a security that pays dt : $1 if the economy state in quarter 15 is G and dt : $0 if the economy state in quarter t is B. Let X : (11 + d2 + d3. Let .7-1,t : l, 2, 3 be the sigmaalgebra that describes the information at time t. 1. Calculate the conditional expectations Z = E[Xl]'t] (note that Zt's are random variables themselves). 2. Find the Ualgebras generated by Z, t = 17 2, 3. Example 1 Suppose the state of the economy in each quarter is either good (G) with probability q and bad (B) with probability 1 q. Suppose further that these probabilities are identical and independent over time. Consider the following probability space of the state of the economy in the next two quarters: (1) :2 : {66, GB, BG, BB} (2) Even in this simple example, there are several aalgebras. Let's consider the following class of aalgebras called a filtration which will play an important role later: Example 4 In Example 1, consider a security X that pays at the second quarter X : $1 if the economy state in quarter 1 is G and X = $0 if the economy state in quarter 1 is B. Then X is a random variable of the probability space 9/71 : {(2), {GG, GB}, {BG7 BB}, 9}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts