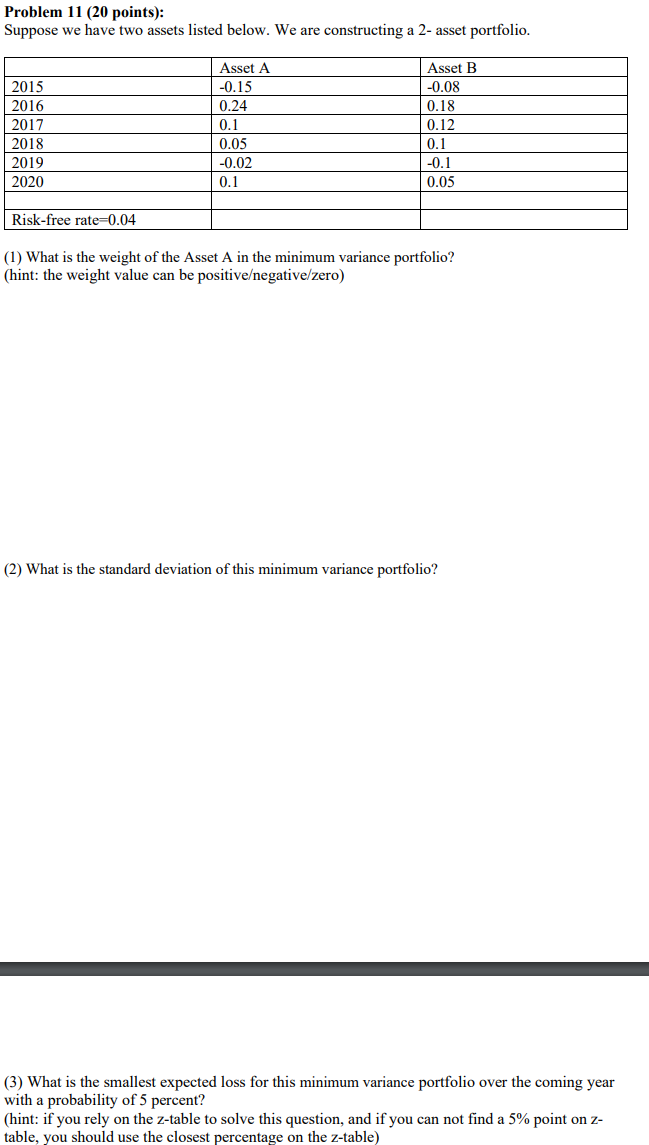

Question: Problem 11 (20 points): Suppose we have two assets listed below. We are constructing a 2-asset portfolio. 2015 2016 2017 2018 2019 2020 Asset A

Problem 11 (20 points): Suppose we have two assets listed below. We are constructing a 2-asset portfolio. 2015 2016 2017 2018 2019 2020 Asset A -0.15 0.24 0.1 0.05 -0.02 0.1 Asset B -0.08 0.18 0.12 0.1 -0.1 0.05 Risk-free rate=0.04 (1) What is the weight of the Asset A in the minimum variance portfolio? (hint: the weight value can be positiveegative/zero) (2) What is the standard deviation of this minimum variance portfolio? (3) What is the smallest expected loss for this minimum variance portfolio over the coming year with a probability of 5 percent? (hint: if you rely on the z-table to solve this question, and if you can not find a 5% point on z- table, you should use the closest percentage on the z-table)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts