Question: Problem 12-23 Hi can you please help me solve this using Excel? Thanks! But scenario 3 is a bad year for the small-cap value fund;

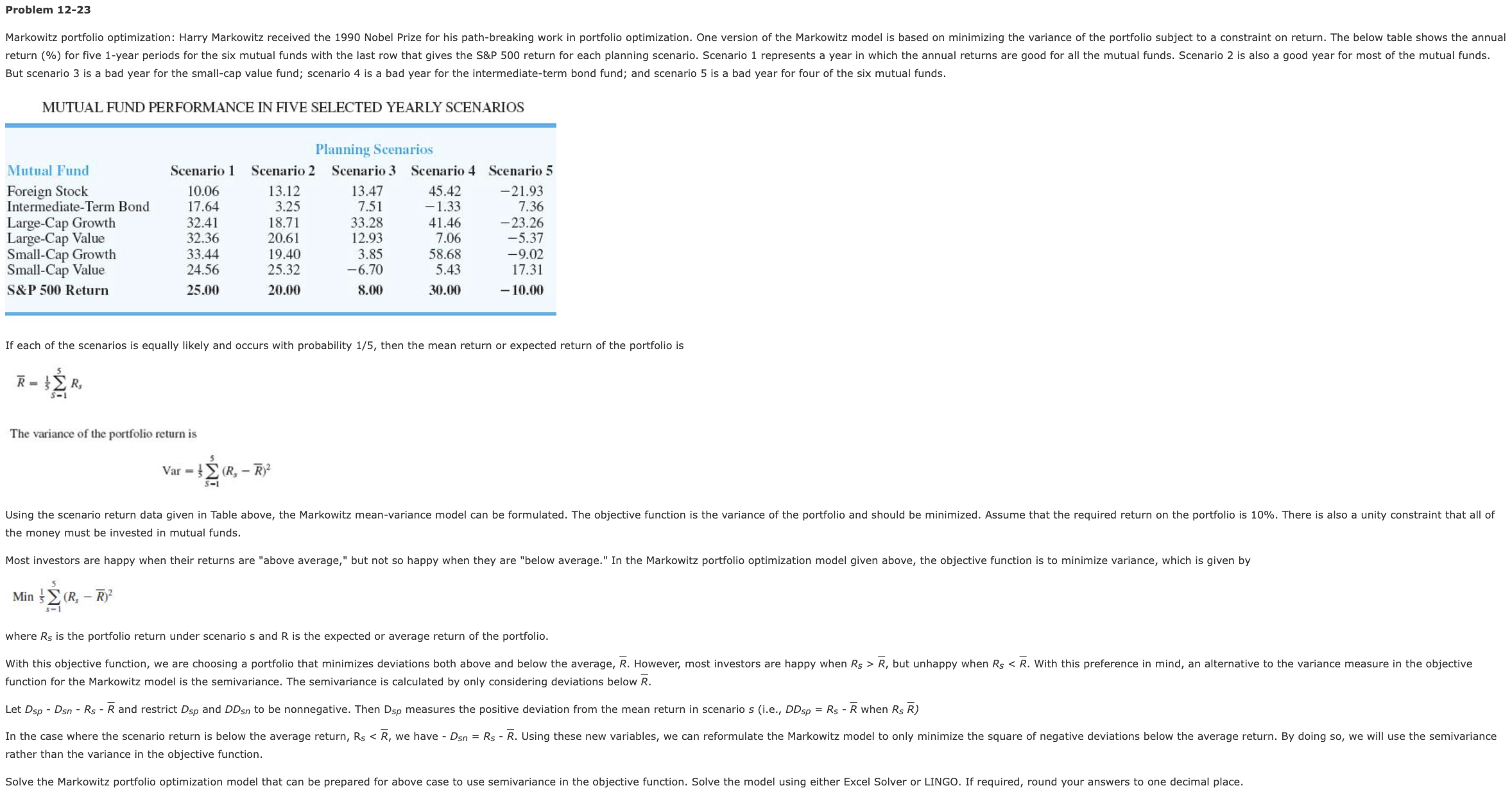

Problem 12-23

Hi can you please help me solve this using Excel? Thanks!

But scenario 3 is a bad year for the small-cap value fund; scenario 4 is a bad year for the intermediate-term bond fund; and scenario 5 is a bad year for four of the six mutual funds. MUTUAL FUND PERFORMANCE IN FIVE SELECTED YEARLY SCENARIOS If each of the scenarios is equally likely and occurs with probability 1/5, then the mean return or expected return of the portfolio is R=51s=15Rs The variance of the portfolio return is Var=51S=15(RsR)2 the money must be invested in mutual funds. Min51s=15(RsR)2 where RS is the portfolio return under scenario s and R is the expected or average return of the portfolio. function for the Markowitz model is the semivariance. The semivariance is calculated by only considering deviations below R. Let DspDsnRSR and restrict Dsp and DDsn to be nonnegative. Then Dsp measures the positive deviation from the mean return in scenario s (i.e., DDsp=RSR when RsR ) rather than the variance in the objective function. \begin{tabular}{|l|c|} \hline Mutual Funds & Investments in \% \\ \hline Foreign Stock & % \\ \hline Intermediate-Term Bond & % \\ \hline Large-Cap Growth & % \\ \hline Large-Cap Value & % \\ \hline Small-Cap Growth & % \\ \hline Small-Cap Value & \\ \hline \end{tabular}

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts