Question: Problem 12-25 (LO. 2, 3, 4, 5) Arthur Wesson, an unmarried individual who is age 68, reports taxable income of $510,000 in 2020. He reports

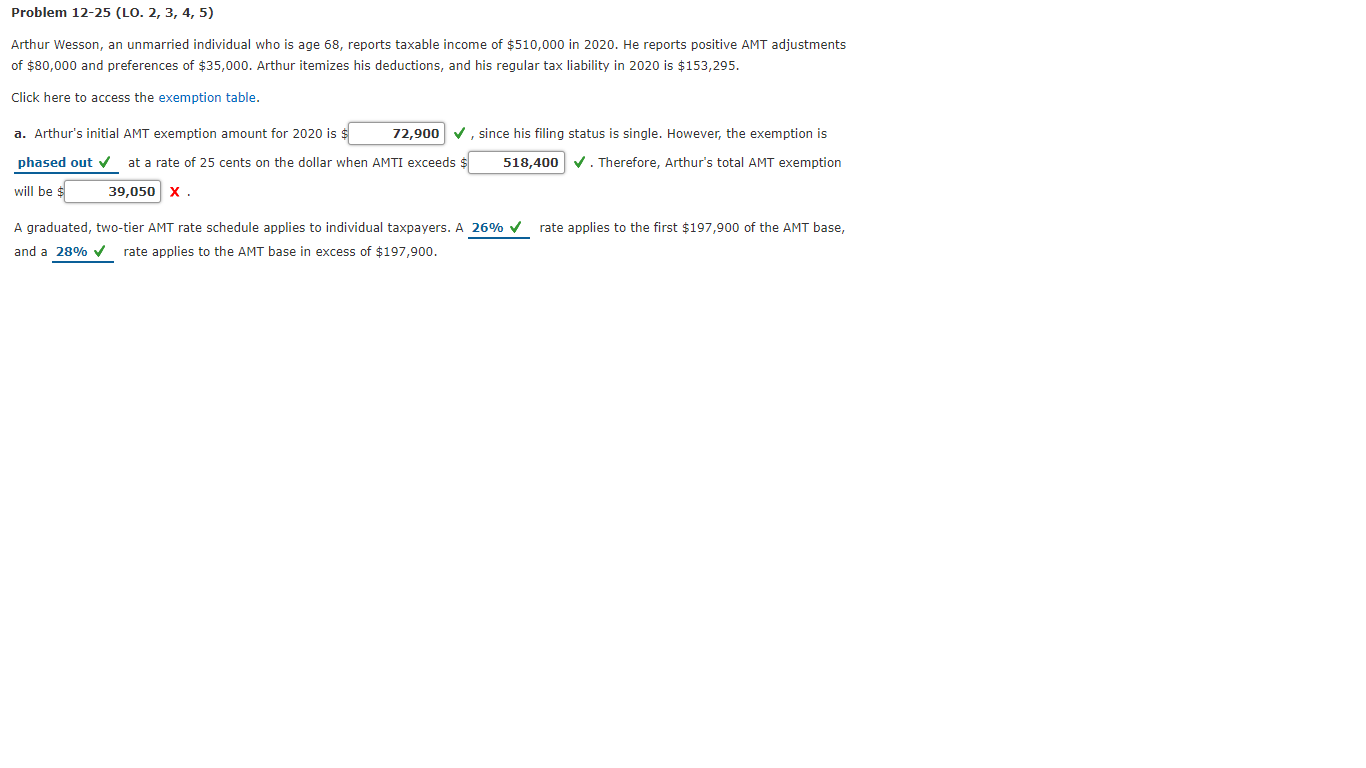

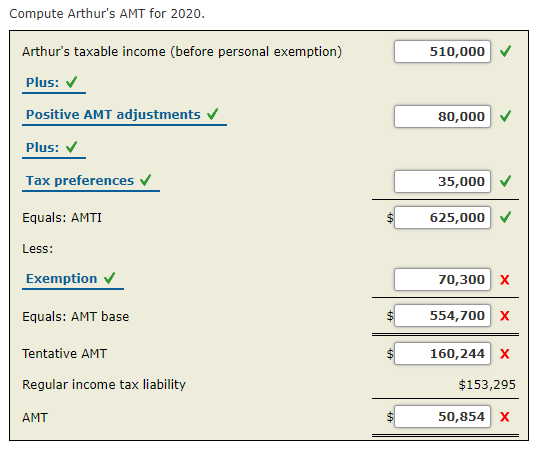

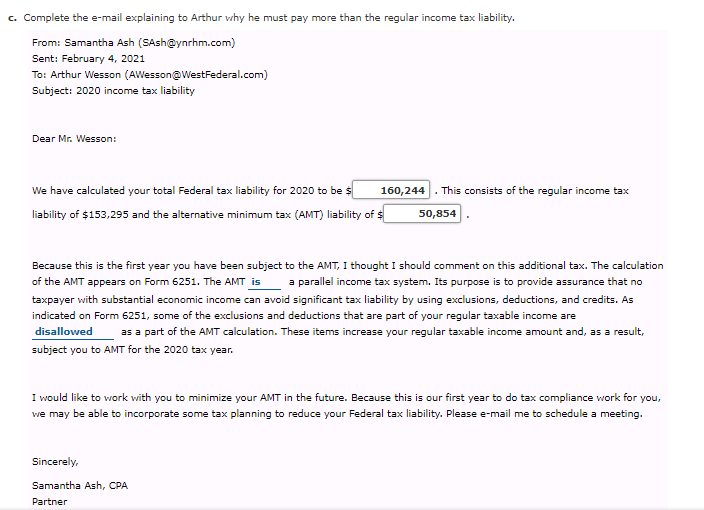

Problem 12-25 (LO. 2, 3, 4, 5) Arthur Wesson, an unmarried individual who is age 68, reports taxable income of $510,000 in 2020. He reports positive AMT adjustments of $80,000 and preferences of $35,000. Arthur itemizes his deductions, and his regular tax liability in 2020 is $153,295. Click here to access the exemption table. a. Arthur's initial AMT exemption amount for 2020 is $ 72,900 , since his filing status is single. However, the exemption is phased out at a rate of 25 cents on the dollar when AMTI exceeds s 518,400 . Therefore, Arthur's total AMT exemption will be $ 39,050 X. A graduated, two-tier AMT rate schedule applies to individual taxpayers. A 26% rate applies to the first $197,900 of the AMT base, and a 28% rate applies to the AMT base in excess of $197,900. Compute Arthur's AMT for 2020. Arthur's taxable income (before personal exemption) 510,000 Plus: Positive AMT adjustments 80,000 Plus: Tax preferences 35,000 Equals: AMTI 625,000 Less: Exemption 70,300 x Equals: AMT base 554,700 x Tentative AMT 160,244 X Regular income tax liability $153,295 AMT 50,854 x b. What is the total amount of Arthur's tax liability? 160,244 X $ C. Complete the e-mail explaining to Arthur why he must pay more than the regular income tax liability. From: Samantha Ash (SAsh@ynrhm.com) Sent: February 4, 2021 To: Arthur Wesson (AWesson@WestFederal.com) Subject: 2020 income tax liability Dear Mr. Wesson: We have calculated your total Federal tax liability for 2020 to be s 160,244 This consists of the regular income tax liability of $153,295 and the alternative minimum tax (AMT) liability of $ 50,854 Because this is the first year you have been subject to the AMT, I thought I should comment on this additional tax. The calculation of the AMT appears on Form 6251. The AMT is a parallel income tax system. Its purpose is to provide assurance that no taxpayer with substantial economic income can avoid significant tax liability by using exclusions, deductions, and credits. As indicated on Form 6251, some of the exclusions and deductions that are part of your regular taxable income are disallowed as a part of the AMT calculation. These items increase your regular taxable income amount and, as a result, subject you to AMT for the 2020 tax year. I would like to work with you to minimize your AMT in the future. Because this is our first year to do tax compliance work for you, we may be able to incorporate some tax planning to reduce your Federal tax liability. Please e-mail me to schedule a meeting. Sincerely, Samantha Ash, CPA Partner

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts