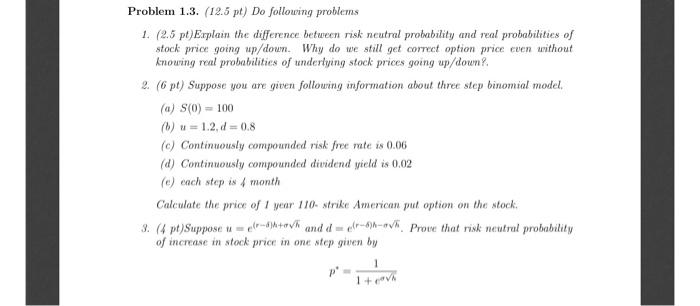

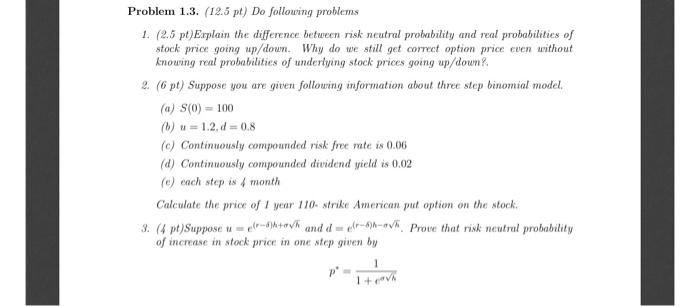

Question: Problem 1.3. (12.5 pt) Do following problems 1. (2.5 pt)Explain the difference between risk neutral prolubility and real probabilities of stock price going up/down. Why

Problem 1.3. (12.5 pt) Do following problems 1. (2.5 pt)Explain the difference between risk neutral prolubility and real probabilities of stock price going up/down. Why do we still get correct option price even without knouring real probabilities of underlying stock prices going up/down? 2. (6 pt) Suppose you are given following information about three step binomial model, (a) S(0) - 100 (0) - 1.2.d = 0.8 (e) Continuously compounded risk free rate is 0.06 (d) Continuously compounded dividend yield is 0.02 (e) each step is 4 month Calculate the price of year 110. strike American pul option on the stock. 3. (4 pt)Suppose u = e(}+ov and do Prove that risk neutral probability of increase in stock price in one step given by 1 1 + Problem 1.3. (12.5 pt) Do following problems 1. (2.5 pt)Explain the difference between risk neutral prolubility and real probabilities of stock price going up/down. Why do we still get correct option price even without knouring real probabilities of underlying stock prices going up/down? 2. (6 pt) Suppose you are given following information about three step binomial model, (a) S(0) - 100 (0) - 1.2.d = 0.8 (e) Continuously compounded risk free rate is 0.06 (d) Continuously compounded dividend yield is 0.02 (e) each step is 4 month Calculate the price of year 110. strike American pul option on the stock. 3. (4 pt)Suppose u = e(}+ov and do Prove that risk neutral probability of increase in stock price in one step given by 1 1 + Problem 1.3. (12.5 pt) Do following problems 1. (2.5 pt)Explain the difference between risk neutral prolubility and real probabilities of stock price going up/down. Why do we still get correct option price even without knouring real probabilities of underlying stock prices going up/down? 2. (6 pt) Suppose you are given following information about three step binomial model, (a) S(0) - 100 (0) - 1.2.d = 0.8 (e) Continuously compounded risk free rate is 0.06 (d) Continuously compounded dividend yield is 0.02 (e) each step is 4 month Calculate the price of year 110. strike American pul option on the stock. 3. (4 pt)Suppose u = e(}+ov and do Prove that risk neutral probability of increase in stock price in one step given by 1 1 + Problem 1.3. (12.5 pt) Do following problems 1. (2.5 pt)Explain the difference between risk neutral prolubility and real probabilities of stock price going up/down. Why do we still get correct option price even without knouring real probabilities of underlying stock prices going up/down? 2. (6 pt) Suppose you are given following information about three step binomial model, (a) S(0) - 100 (0) - 1.2.d = 0.8 (e) Continuously compounded risk free rate is 0.06 (d) Continuously compounded dividend yield is 0.02 (e) each step is 4 month Calculate the price of year 110. strike American pul option on the stock. 3. (4 pt)Suppose u = e(}+ov and do Prove that risk neutral probability of increase in stock price in one step given by 1 1 +

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts