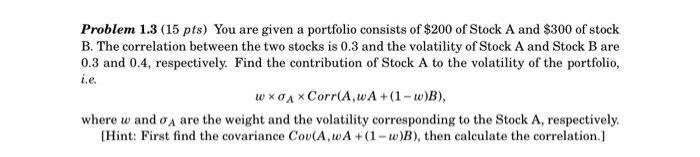

Question: Problem 1.3 (15 pts) You are given a portfolio consists of $200 of Stock A and $300 of stock B. The correlation between the two

Problem 1.3 (15 pts) You are given a portfolio consists of $200 of Stock A and $300 of stock B. The correlation between the two stocks is 0.3 and the volatility of Stock A and Stock B are 0.3 and 0.4, respectively. Find the contribution of Stock A to the volatility of the portfolio, wX0A x Corr(A,WA+(1-w)B), where w and 0 A are the weight and the volatility corresponding to the Stock A, respectively, (Hint: First find the covariance Cou(A,wA+ (1 -w)B), then calculate the correlation]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock