Question: Problem 13-23 Portfolio Returns and Deviations (L01, 2) Consider the following information about three stocks: State of Probability of State Rate of Return if State

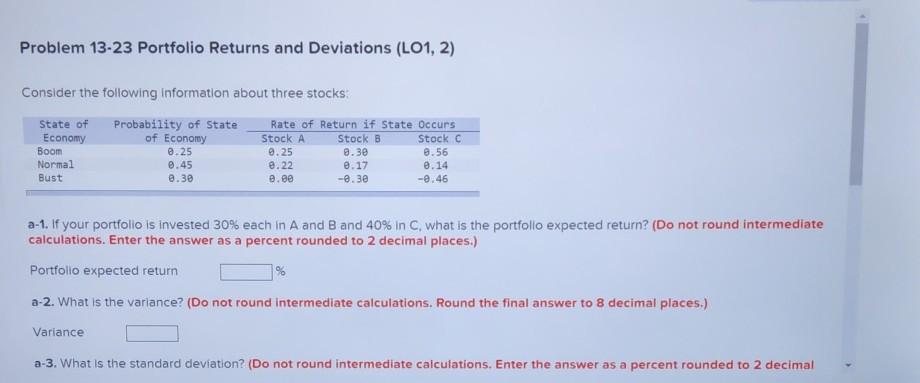

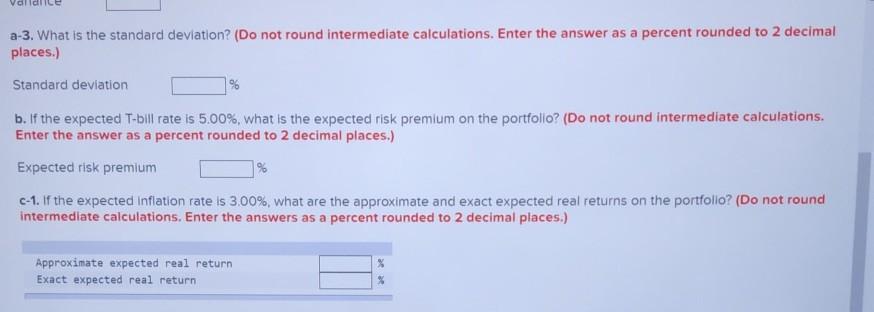

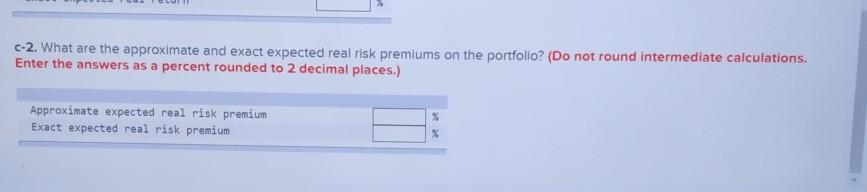

Problem 13-23 Portfolio Returns and Deviations (L01, 2) Consider the following information about three stocks: State of Probability of State Rate of Return if State Occurs Economy of Economy Stock A Stock B Stock C Boom 0.25 0.25 8.30 8.56 Normal 0.45 8.22 0.17 0.14 Bust 2.30 e.ee -0.30 -0.46 a-1. If your portfolio is invested 30% each in A and B and 40% in C, what is the portfolio expected return? (Do not round intermediate calculations. Enter the answer as a percent rounded to 2 decimal places.) Portfolio expected return % a-2. What is the variance? (Do not round intermediate calculations. Round the final answer to 8 decimal places.) Variance a-3. What is the standard deviation? (Do not round intermediate calculations. Enter the answer as a percent rounded to 2 decimal a-3. What is the standard deviation? (Do not round intermediate calculations. Enter the answer as a percent rounded to 2 decimal places.) Standard deviation 1% b. If the expected T-bill rate is 5.00%, what is the expected risk premium on the portfolio? (Do not round intermediate calculations. Enter the answer as a percent rounded to 2 decimal places.) Expected risk premium % c-1. If the expected Inflation rate is 3.00%, what are the approximate and exact expected real returns on the portfolio? (Do not round intermediate calculations. Enter the answers as a percent rounded to 2 decimal places.) Approximate expected real return Exact expected real return % c-2. What are the approximate and exact expected real risk premiums on the portfolio? (Do not round intermediate calculations. Enter the answers as a percent rounded to 2 decimal places.) Approximate expected real risk premium Exact expected real risk premium %

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts