Question: Problem 14-02A a-c (Part Level Submission) The post-closing trial balance of Crane Corporation at December 31, 2020 contains the following stockholders equity accounts. Preferred Stock

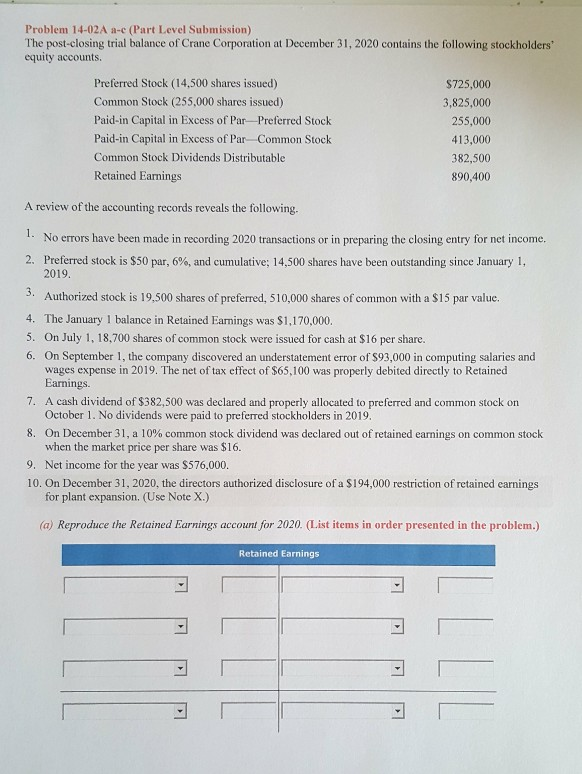

Problem 14-02A a-c (Part Level Submission) The post-closing trial balance of Crane Corporation at December 31, 2020 contains the following stockholders equity accounts. Preferred Stock (14,500 shares issued) Common Stock (255,000 shares issued) Paid-in Capital in Excess of Par-Preferred Stock Paid-in Capital in Excess of Par Common Stock Common Stock Dividends Distributable Retained Earnings $725,000 3,825,000 255,000 413,000 382,500 890,400 A review of the accounting records reveals the following. 1. No errors have been made in recording 2020 transactions or in preparing the closing entry for net income. 2. Preferred stock is $50 par, 6%, and cumulative; 14,500 shares have been outstanding since January 1, 2019. 3. Authorized stock is 19,500 shares of preferred, 510,000 shares of common with a $15 par value. 4. The January 1 balance in Retained Earnings was $1,170,000. 5. On July 1, 18.700 shares of common stock were issued for cash at $16 per share. 6. On September 1, the company discovered an understatement error of $93,000 in computing salaries and wages expense in 2019. The net of tax effect of $65.100 was properly debited directly to Retained Earnings. 7. A cash dividend of $382,500 was declared and properly allocated to preferred and common stock on October 1. No dividends were paid to preferred stockholders in 2019. 8. On December 31. a 10% common stock dividend was declared out of retained earnings on common stock when the market price per share was $16. 9. Net income for the year was $576,000. 10. On December 31, 2020, the directors authorized disclosure of a $194,000 restriction of retained earnings for plant expansion. (Use Note X.) (a) Reproduce the Retained Earnings account for 2020. (List items in order presented in the problem.) Retained Earnings

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts