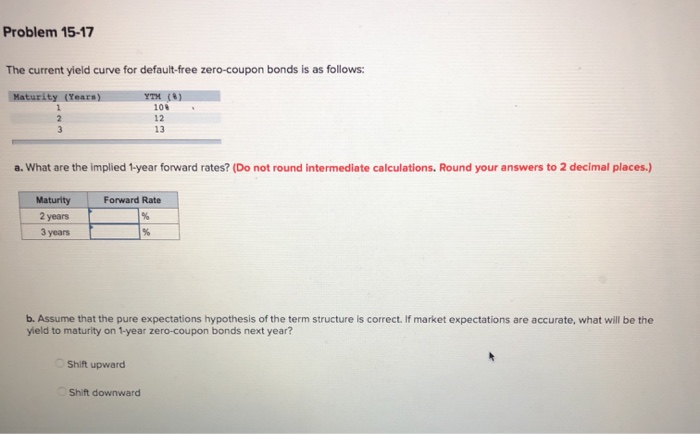

Question: Problem 15-17 The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (0) 100 12 a. What are the implied 1-year

Problem 15-17 The current yield curve for default-free zero-coupon bonds is as follows: Maturity (Years) YTM (0) 100 12 a. What are the implied 1-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Forward Rate Maturity 2 years 3 years b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will be the yield to maturity on 1-year zero-coupon bonds next year? Shift upward Shift downward

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock