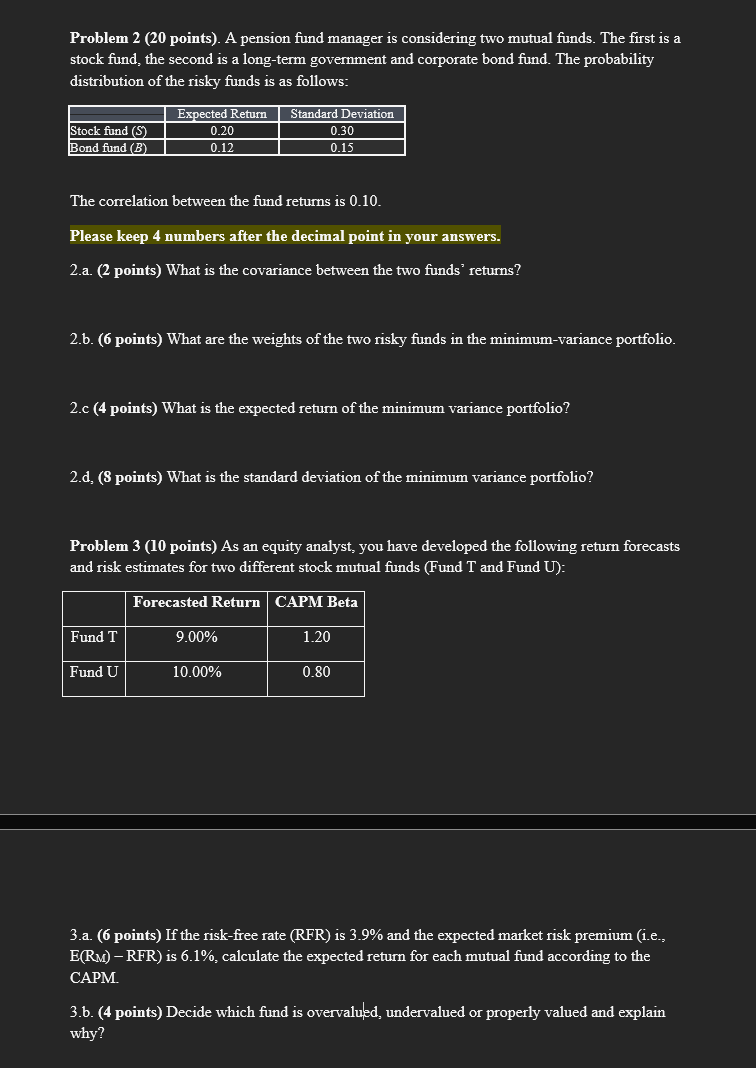

Question: Problem 2 ( 2 0 points ) . A pension fund manager is considering two mutual funds. The first is a stock fund, the second

Problem points A pension fund manager is considering two mutual funds. The first is a

stock fund, the second is a longterm government and corporate bond fund. The probability

distribution of the risky funds is as follows:

The correlation between the fund returns is

Please keep numbers after the decimal point in your answers.

a points What is the covariance between the two funds' returns?

b points What are the weights of the two risky funds in the minimumvariance portfolio.

c points What is the expected return of the minimum variance portfolio?

d points What is the standard deviation of the minimum variance portfolio?

Problem points As an equity analyst, you have developed the following return forecasts

and risk estimates for two different stock mutual funds Fund T and Fund U:

a points If the riskfree rate RFR is and the expected market risk premium ie

is calculate the expected return for each mutual fund according to the

CAPM

b points Decide which fund is overvalued, undervalued or properly valued and explain

why?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock