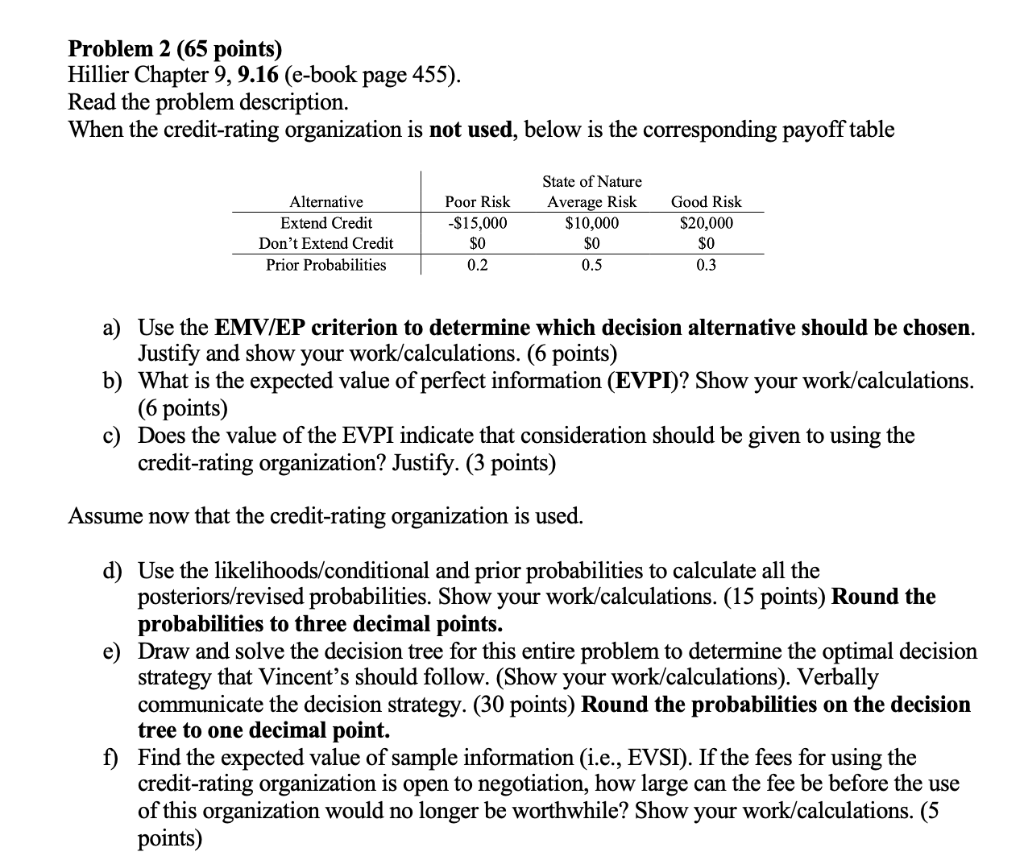

Question: Problem 2 (65 points) Hillier Chapter 9,9.16 (e-book page 455). Read the problem description. When the credit-rating organization is not used, below is the corresponding

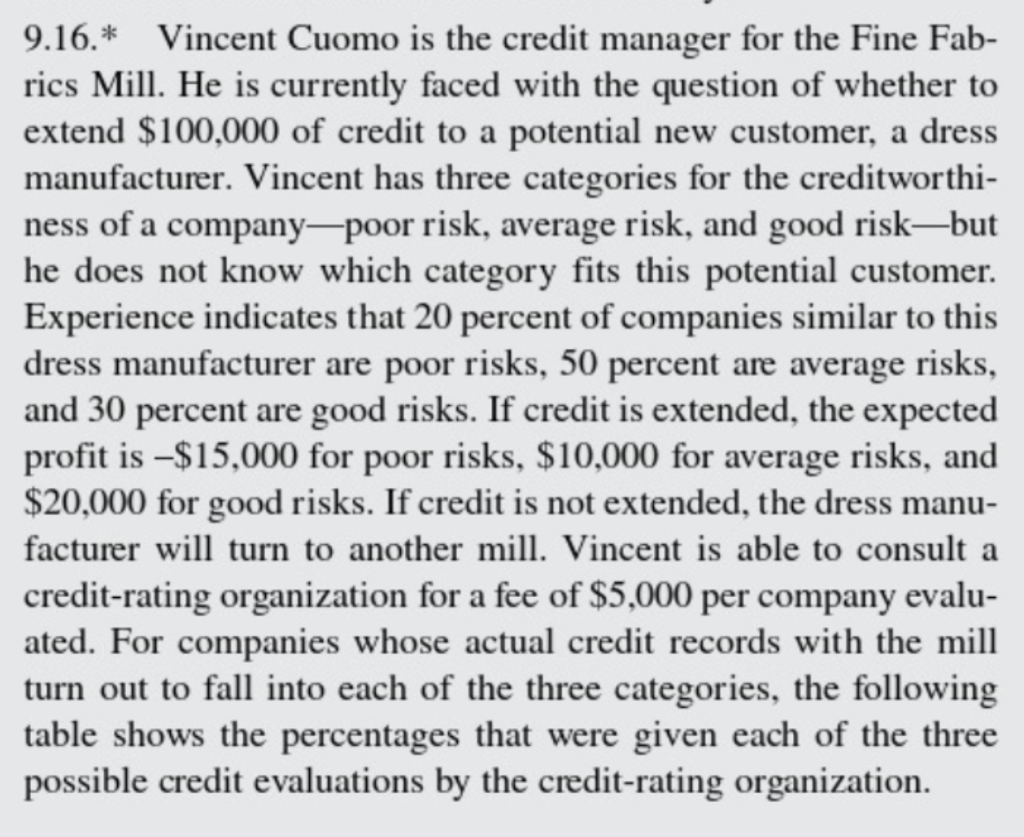

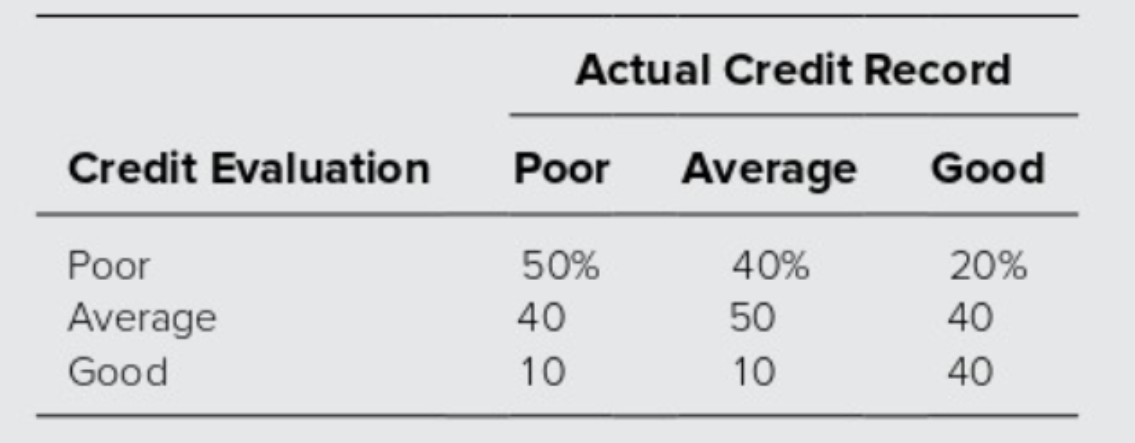

Problem 2 (65 points) Hillier Chapter 9,9.16 (e-book page 455). Read the problem description. When the credit-rating organization is not used, below is the corresponding payoff table a) Use the EMV/EP criterion to determine which decision alternative should be chosen. Justify and show your work/calculations. (6 points) b) What is the expected value of perfect information (EVPI)? Show your work/calculations. (6 points) c) Does the value of the EVPI indicate that consideration should be given to using the credit-rating organization? Justify. (3 points) Assume now that the credit-rating organization is used. d) Use the likelihoods/conditional and prior probabilities to calculate all the posteriors/revised probabilities. Show your work/calculations. (15 points) Round the probabilities to three decimal points. e) Draw and solve the decision tree for this entire problem to determine the optimal decision strategy that Vincent's should follow. (Show your work/calculations). Verbally communicate the decision strategy. (30 points) Round the probabilities on the decision tree to one decimal point. f) Find the expected value of sample information (i.e., EVSI). If the fees for using the credit-rating organization is open to negotiation, how large can the fee be before the use of this organization would no longer be worthwhile? Show your work/calculations. (5 points) 9.16.* Vincent Cuomo is the credit manager for the Fine Fabrics Mill. He is currently faced with the question of whether to extend $100,000 of credit to a potential new customer, a dress manufacturer. Vincent has three categories for the creditworthiness of a company-poor risk, average risk, and good risk-but he does not know which category fits this potential customer. Experience indicates that 20 percent of companies similar to this dress manufacturer are poor risks, 50 percent are average risks, and 30 percent are good risks. If credit is extended, the expected profit is $15,000 for poor risks, $10,000 for average risks, and $20,000 for good risks. If credit is not extended, the dress manufacturer will turn to another mill. Vincent is able to consult a credit-rating organization for a fee of $5,000 per company evaluated. For companies whose actual credit records with the mill turn out to fall into each of the three categories, the following table shows the percentages that were given each of the three possible credit evaluations by the credit-rating organization. \begin{tabular}{lccc} \hline & \multicolumn{3}{c}{ Actual Credit Record } \\ \cline { 2 - 4 } Credit Evaluation & Poor & Average & Good \\ \hline Poor & 50% & 40% & 20% \\ Average & 40 & 50 & 40 \\ Good & 10 & 10 & 40 \\ \hline \end{tabular}